Key Takeaways

- Adjusted capital spending and asset optimization strategies aim to enhance cash flow, improve margins, and focus on high-margin operations.

- Strategic divestitures and cost reductions enhance financial flexibility and improve earnings amidst macroeconomic challenges, with litigation proceeds providing additional support.

- Margin pressures and geopolitical uncertainties are challenging profitability, while delayed projects and regulatory issues indicate concerns about future growth and earnings.

Catalysts

About Dow- Through its subsidiaries, provides various materials science solutions for packaging, infrastructure, mobility, and consumer applications in the United States, Canada, Europe, the Middle East, Africa, India, the Asia Pacific, and Latin America.

- Dow is delaying construction on the Path2Zero project in Fort Saskatchewan, which aligns with their strategy to adjust capital spending in response to market conditions, potentially improving near-term cash flow and margins due to reduced CapEx.

- The company is expanding their strategic review of European assets, planning to idle or shut down three initial assets. This move aims to optimize asset utilization and enhance near-term cash flow, potentially improving earnings by reducing excess capacity and focusing on higher-margin operations.

- Dow expects a $2.4 billion influx from the sale of their minority stake in select U.S. Gulf Coast infrastructure assets, which will bolster cash reserves and improve financial flexibility, providing a potential boost to earnings.

- A final ruling on pending Nova litigation is anticipated, with expected proceeds exceeding $1 billion, offering significant cash inflow that can support capital allocation strategies, influencing earnings positively.

- Dow is targeting at least $1 billion in annual cost reductions by 2026, focusing on areas such as purchased services and contract labor. These cost-cutting measures aim to improve net margins and bolster earnings despite a challenging macroeconomic environment.

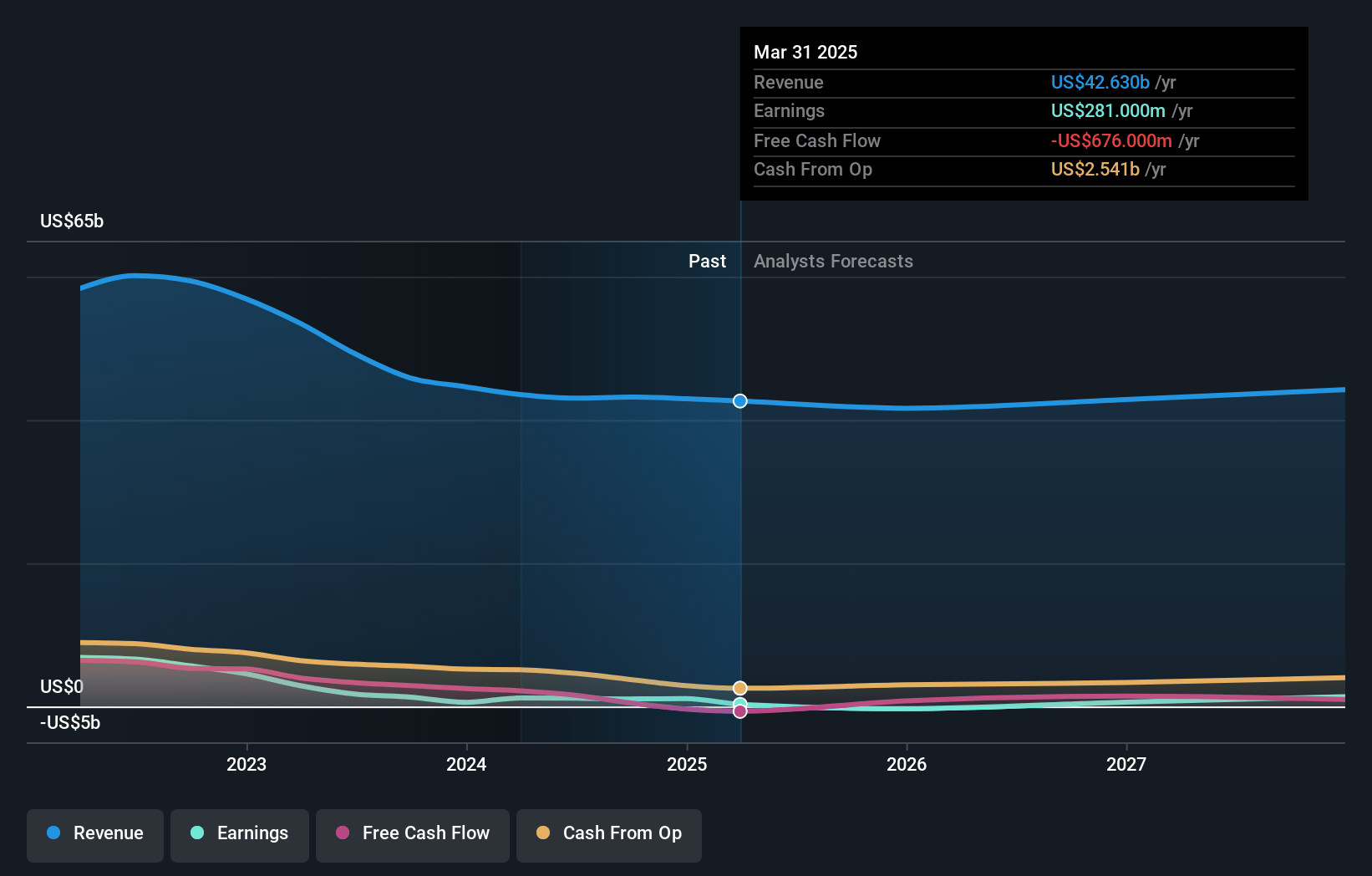

Dow Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Dow's revenue will grow by 1.4% annually over the next 3 years.

- Analysts assume that profit margins will increase from 0.7% today to 4.1% in 3 years time.

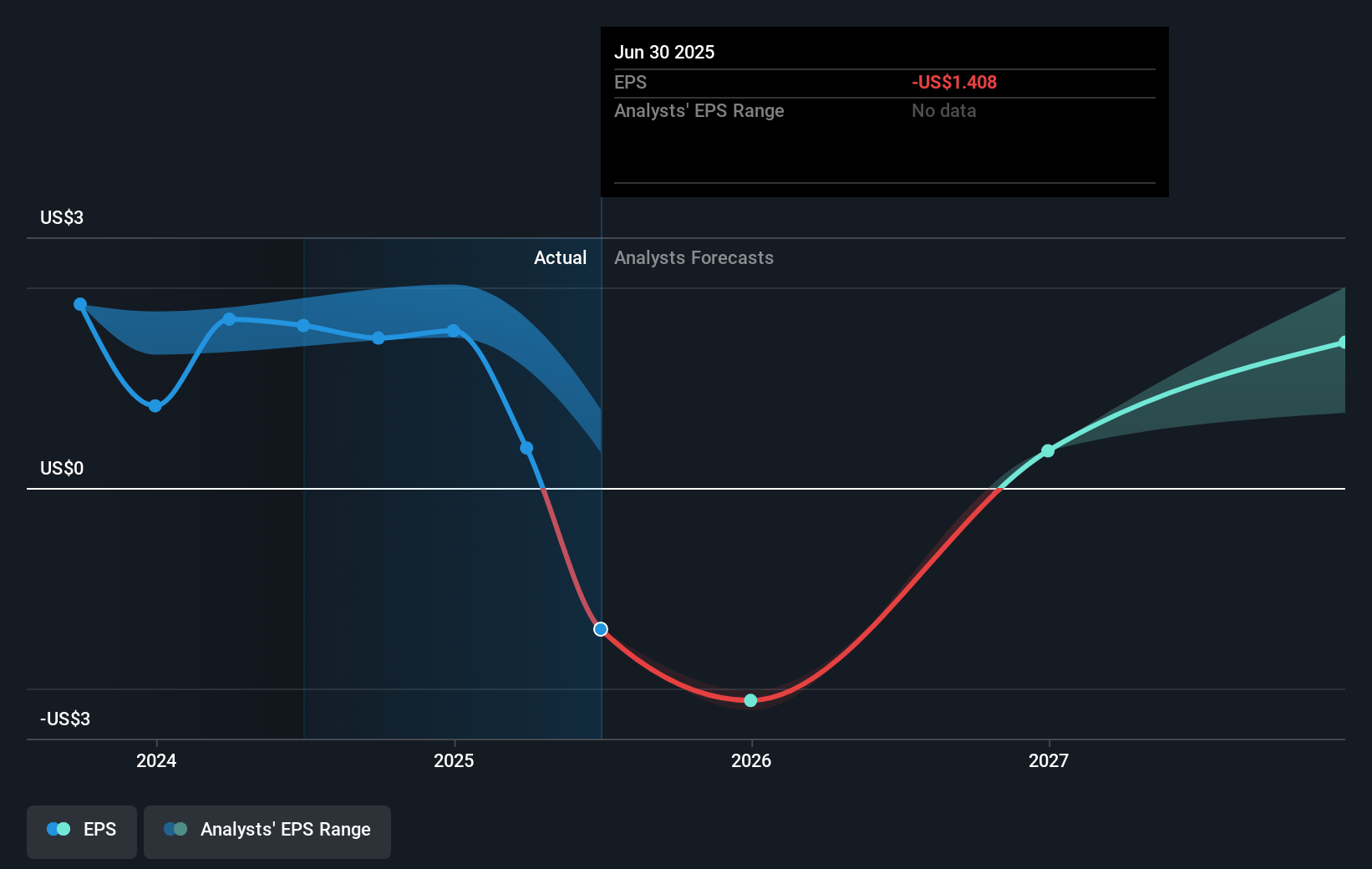

- Analysts expect earnings to reach $1.8 billion (and earnings per share of $2.47) by about April 2028, up from $281.0 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $2.2 billion in earnings, and the most bearish expecting $1.4 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 18.4x on those 2028 earnings, down from 77.1x today. This future PE is lower than the current PE for the US Chemicals industry at 19.3x.

- Analysts expect the number of shares outstanding to grow by 0.52% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.4%, as per the Simply Wall St company report.

Dow Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The company faces margin pressures in all operating segments due to elevated feedstock and energy costs, which have not declined as expected, thereby impacting net margins and profitability.

- There is a risk of prolonged macroeconomic weakness and below-average GDP growth, which could weigh heavily on global demand and thereby reduce revenue potential.

- Dow is delaying capital projects such as the Path2Zero construction to conserve cash, indicating potential concerns about future earnings and growth forecasts.

- The expansion of the European asset review highlights persistent demand and regulatory challenges in that region, potentially impacting revenues and profitability from Dow's European operations.

- Geopolitical and tariff uncertainties, particularly concerning trade with China, create significant unpredictability that could lead to operational and revenue disruptions, thereby challenging net margins and earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $36.478 for Dow based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $63.12, and the most bearish reporting a price target of just $27.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $44.4 billion, earnings will come to $1.8 billion, and it would be trading on a PE ratio of 18.4x, assuming you use a discount rate of 8.4%.

- Given the current share price of $30.65, the analyst price target of $36.48 is 16.0% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.