Key Takeaways

- New recycling center and Vision '25 program are set to enhance earnings and margins through cost savings and improved EBITDA.

- Share buybacks and improved aerospace contracts show confidence in future growth, supporting EPS despite supply chain and market challenges.

- Constellium faces challenges with weaker demand in aerospace, automotive, and industrial markets, high metal costs, and unexpected financial impacts, risking revenue and earnings stability.

Catalysts

About Constellium- Engages in the design, manufacture, and sale of rolled and extruded aluminum products for the packaging, aerospace, automotive, defense, and other transportation and industry end-markets.

- The startup of the new recycling and casting center in Neuf-Brisach ahead of schedule and below budget should provide a significant boost to EBITDA, estimated between €35 million to €40 million for the next year, positively impacting earnings.

- The Vision '25 cost improvement program aims to achieve north of €25 million in additional savings, enhancing net margins through cost reductions in labor and other nonmetal expenses.

- Better contractual terms in aerospace next year, particularly in the commercial aircraft sector, are expected to bolster earnings, even as short-term demand shifts due to supply chain challenges.

- Progress in operations at Muscle Shoals, with better production rates expected, should contribute to earnings improvement, although it may be slightly offset by tighter scrap spreads impacting net margins.

- Continued share buybacks, with a year-to-date repurchase of roughly 3.1 million shares, indicate confidence in future free cash flow generation, anticipated to support EPS growth despite current market headwinds.

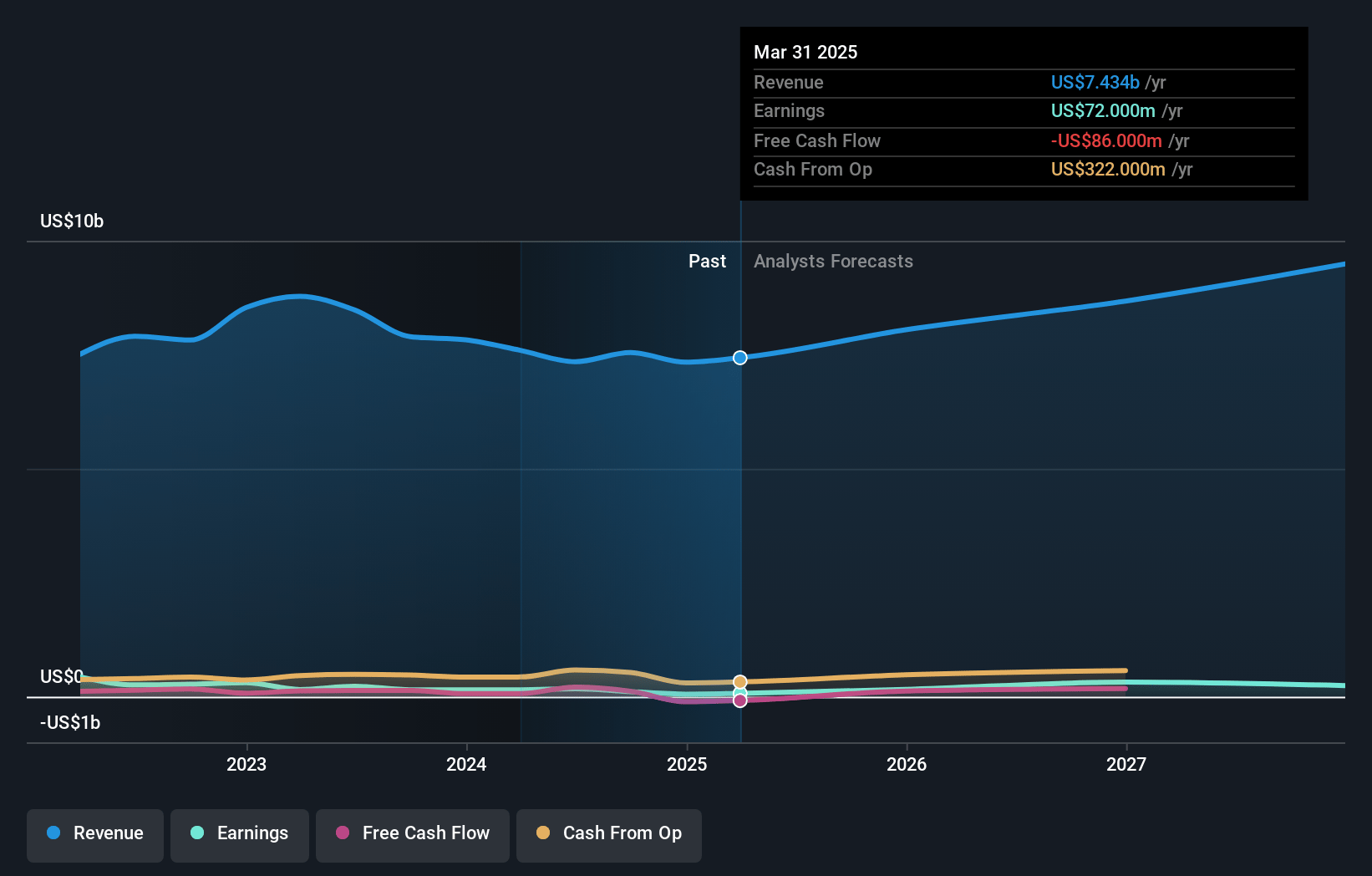

Constellium Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Constellium's revenue will grow by 9.0% annually over the next 3 years.

- Analysts assume that profit margins will increase from 1.5% today to 4.4% in 3 years time.

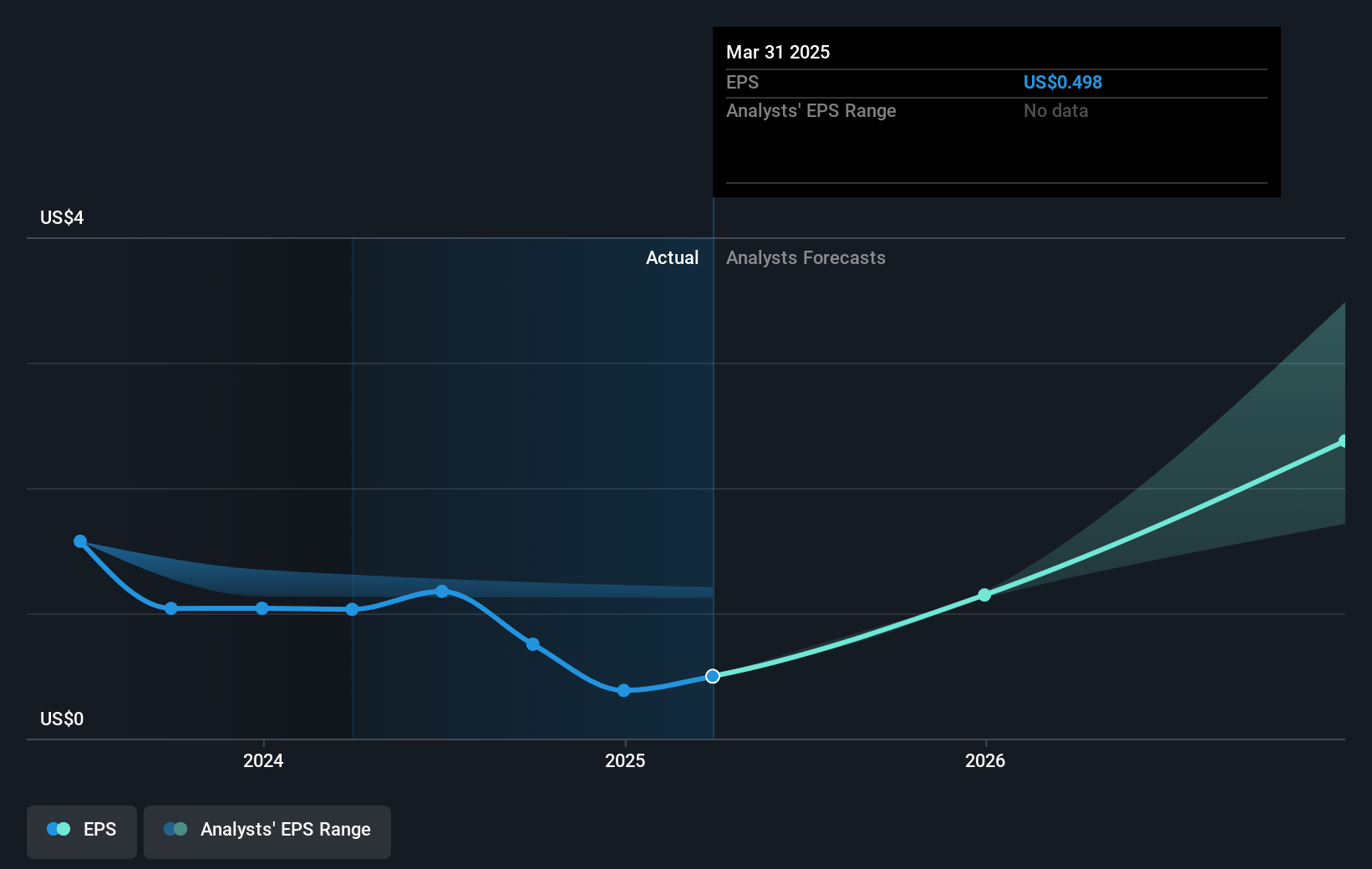

- Analysts expect earnings to reach €384.4 million (and earnings per share of €3.02) by about January 2028, up from €99.0 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 7.8x on those 2028 earnings, down from 14.1x today. This future PE is lower than the current PE for the US Metals and Mining industry at 16.5x.

- Analysts expect the number of shares outstanding to decline by 4.48% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 11.01%, as per the Simply Wall St company report.

Constellium Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Constellium is facing slower aerospace demand, partly due to supply chain challenges impacting OEMs' build rates, which could negatively affect revenue and earnings.

- Automotive demand is weakening in North America and Europe, particularly impacting the luxury, premium, and electric vehicle segments, potentially leading to lower revenues and net margins.

- There has been a sharp decline in demand in North America for industrial markets, which may reduce revenue and contribute to earnings volatility.

- Constellium experienced a significant financial impact due to flooding in Valais, Switzerland, affecting their adjusted EBITDA and free cash flow, which could pose a risk to their financial performance.

- High metal costs and tighter scrap spreads are unfavorable for the company, reducing segment margins and potentially impacting overall earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $18.09 for Constellium based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $23.78, and the most bearish reporting a price target of just $11.13.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be €8.8 billion, earnings will come to €384.4 million, and it would be trading on a PE ratio of 7.8x, assuming you use a discount rate of 11.0%.

- Given the current share price of $9.95, the analyst's price target of $18.09 is 45.0% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives