Narratives are currently in beta

Key Takeaways

- Completion of feasibility studies and new producing assets are expected to boost Royal Gold's revenue and mine life.

- Debt-free status and significant liquidity enable strategic acquisitions, enhancing future growth and earnings.

- Changes in SEC reporting, market dynamics, operational challenges, and geopolitical risks may affect Royal Gold's investor confidence, revenue predictability, and earnings growth.

Catalysts

About Royal Gold- Acquires and manages precious metal streams, royalties, and related interests.

- The expected completion of feasibility studies, such as the study at Mount Milligan and the expansion at Khoemacau, could lead to production increases and extended mine life, which are likely to boost Royal Gold's future revenue streams.

- Several new producing assets, such as Bellevue, Mara Rosa, Wonder North, and Cote Gold, are beginning to contribute to revenue, and continued ramp-up at these sites is anticipated to drive revenue growth.

- Plans for production expansion, such as the development of the Zone 5 mine and the Mango Northeast deposits at Khoemacau, will likely enhance earnings and operating cash flow in the long term once operational.

- The high gold price environment boosts financial results and provides an opportunity for Royal Gold to invest in new projects that could drive future growth, potentially increasing earnings as these projects come to fruition.

- The company’s improved financial position, with being debt-free and having significant liquidity, allows for strategic acquisitions and investments that could lead to enhanced future revenue and earnings.

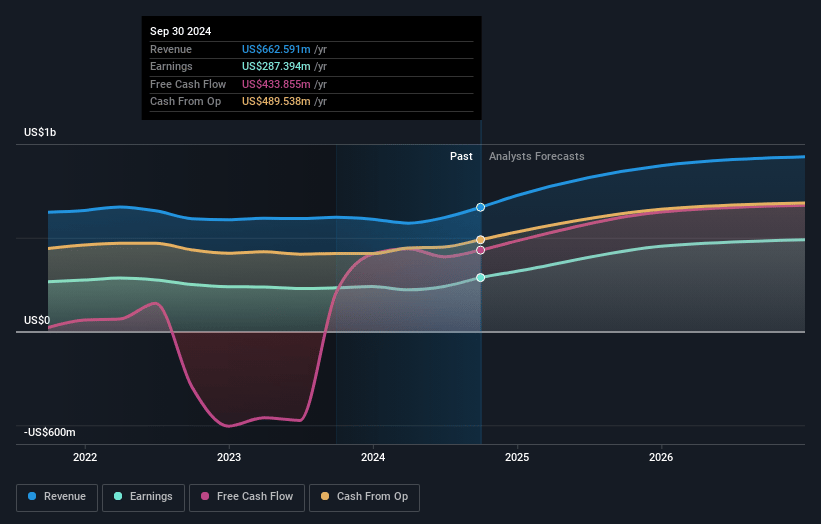

Royal Gold Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Royal Gold's revenue will grow by 19.1% annually over the next 3 years.

- Analysts assume that profit margins will increase from 43.4% today to 51.1% in 3 years time.

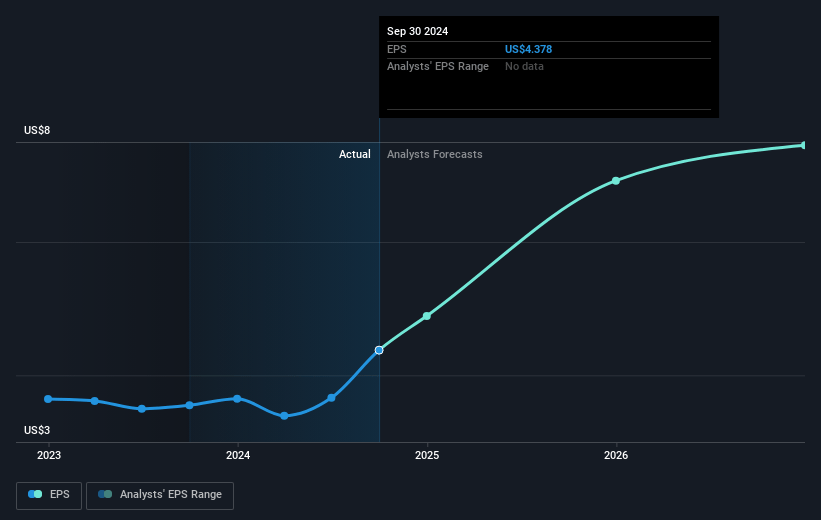

- Analysts expect earnings to reach $571.4 million (and earnings per share of $9.66) by about January 2028, up from $287.4 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 21.8x on those 2028 earnings, down from 31.8x today. This future PE is greater than the current PE for the US Metals and Mining industry at 16.5x.

- Analysts expect the number of shares outstanding to decline by 3.47% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.0%, as per the Simply Wall St company report.

Royal Gold Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Changes in SEC reporting standards (Regulation S-K 1300) could impact investor confidence and transparency regarding the company's reported reserves and resources, potentially affecting the company's perceived stability and future revenue forecasts.

- Timing uncertainties of metal deliveries under streaming agreements, particularly with assets like Mount Milligan, could lead to inconsistent quarterly revenues, impacting earnings predictability.

- Production and delivery challenges related to weather conditions or other operational factors, such as water availability at Andacollo, may affect future revenue streams as these factors can disrupt production.

- Political changes and risks in certain jurisdictions, such as recent government changes in Botswana, could pose operational and financial risks to the company's interest in these regions, possibly affecting future earnings from affected operations.

- An intensely competitive market environment, requiring more complex deal structures to secure investments, could increase costs or lead to less favorable financial terms, thereby impacting net margins and earnings growth prospects.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $172.0 for Royal Gold based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $186.0, and the most bearish reporting a price target of just $140.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $1.1 billion, earnings will come to $571.4 million, and it would be trading on a PE ratio of 21.8x, assuming you use a discount rate of 7.0%.

- Given the current share price of $139.03, the analyst's price target of $172.0 is 19.2% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives