Key Takeaways

- Diversification into specialty insurance and tech-driven operations is improving revenue stability, earnings quality, and operational efficiency.

- Infrastructure trends and advanced risk management are boosting demand for Ambac's products, driving new revenue and fee income.

- Heavy legacy exposure, regulatory pressures, and limited diversification restrict Ambac's growth while growing competition and climate risks threaten profitability and future revenue streams.

Catalysts

About Ambac Financial Group- Operates as a financial services holding company.

- The expected increase in U.S. infrastructure spending and municipal bond issuance is set to boost demand for bond insurance, providing Ambac with new revenue streams and supporting top-line growth.

- Expansion into specialty property & casualty insurance diversifies Ambac's earnings base, reducing reliance on legacy products and leading to more stable recurring revenue and improved earnings quality.

- Investments in technology-driven underwriting and automation are positioned to enhance operational efficiency, lower loss ratios, and support net margin expansion through better risk selection and reduced costs.

- Ongoing runoff of legacy insured portfolios and proactive litigation recoveries could unlock additional capital and generate extraordinary gains, positively impacting both earnings and capital flexibility.

- Industry-wide emphasis on advanced risk management in response to more complex financial markets should drive increased demand for Ambac's insurance and risk solutions, directly supporting higher fee income and premiums earned.

Ambac Financial Group Future Earnings and Revenue Growth

Assumptions

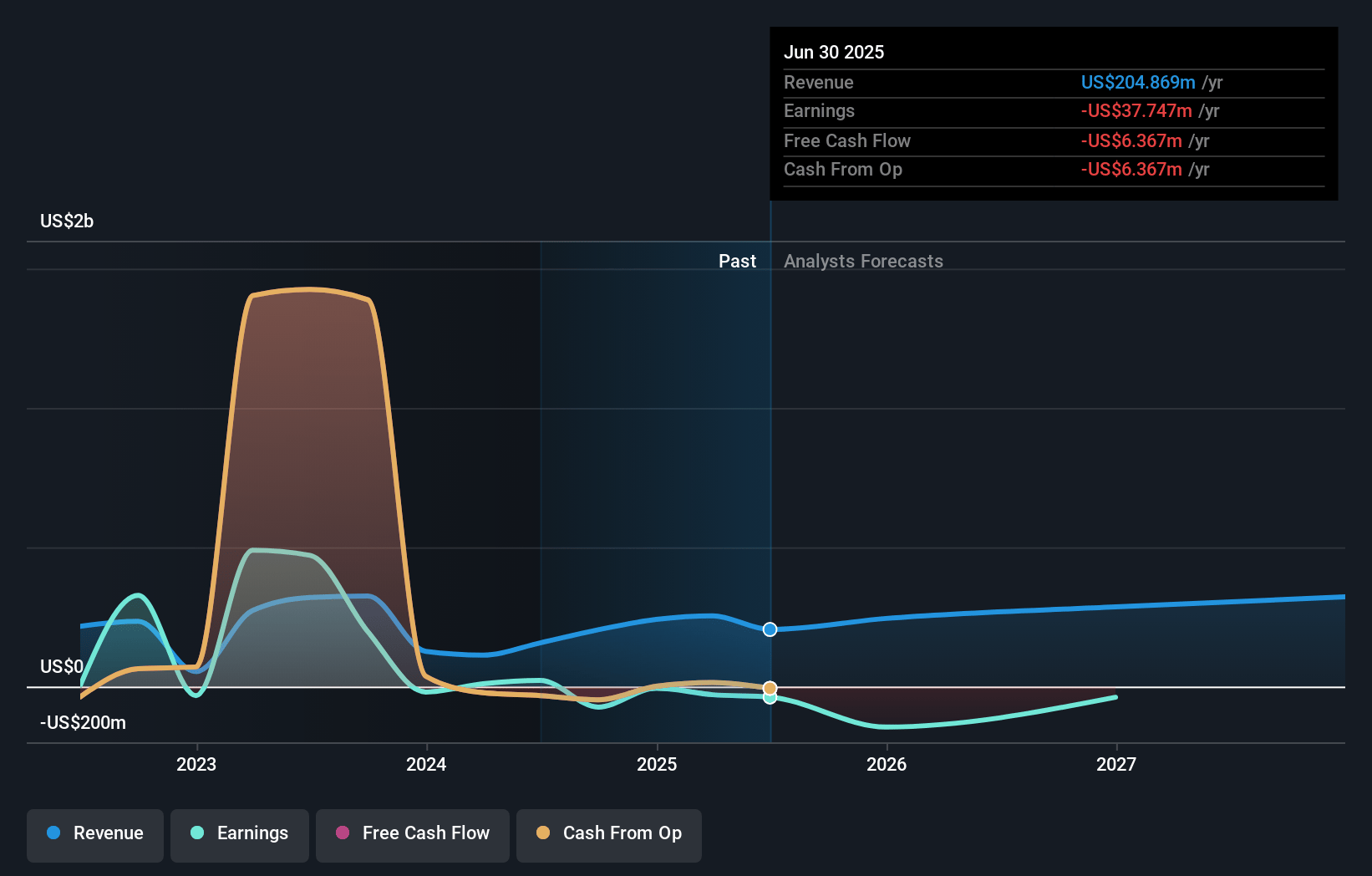

How have these above catalysts been quantified?- Analysts are assuming Ambac Financial Group's revenue will grow by 10.4% annually over the next 3 years.

- Analysts are not forecasting that Ambac Financial Group will become profitable in next 3 years. To represent the Analyst Price Target as a Future PE Valuation we will estimate Ambac Financial Group's profit margin will increase from -11.6% to the average US Insurance industry of 10.4% in 3 years.

- If Ambac Financial Group's profit margin were to converge on the industry average, you could expect earnings to reach $35.5 million (and earnings per share of $0.82) by about July 2028, up from $-29.4 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 21.5x on those 2028 earnings, up from -13.8x today. This future PE is greater than the current PE for the US Insurance industry at 14.4x.

- Analysts expect the number of shares outstanding to decline by 2.14% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.58%, as per the Simply Wall St company report.

Ambac Financial Group Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Persistent legacy exposure to structured finance and distressed municipal debt carries the risk of ongoing litigation costs or unexpected claims, which could directly erode Ambac's net earnings and strain balance sheet reserves.

- Limited business diversification and overreliance on specialty insurance and legacy run-off business restrict Ambac's ability to generate new sources of recurring revenue, potentially resulting in prolonged revenue stagnation and pressure on top-line growth.

- Heightened regulatory requirements for capital adequacy and solvency may force Ambac to hold larger capital reserves and limit flexibility in underwriting, weighing down return on investment and placing constraints on future earnings growth.

- Acceleration of climate change risks and an increase in natural disasters could raise the incidence of municipal bond defaults in Ambac's insured regions, leading to higher payouts and lower underwriting profitability, thus negatively impacting net margins.

- Increasing competition and consolidation in the financial guaranty sector intensifies downward pricing pressure, while the rise of capital market risk transfer alternatives erodes demand for traditional insurance, both of which can reduce Ambac's premium income and long-term fee revenue.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $14.667 for Ambac Financial Group based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $19.0, and the most bearish reporting a price target of just $10.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $341.4 million, earnings will come to $35.5 million, and it would be trading on a PE ratio of 21.5x, assuming you use a discount rate of 6.6%.

- Given the current share price of $8.71, the analyst price target of $14.67 is 40.6% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.