Key Takeaways

- Rising regulatory and labor costs, alongside public skepticism, threaten profitability and sustained demand for the company’s aesthetic treatment systems.

- Competitive pressures and dependence on international markets increase pricing, revenue, and margin volatility.

- Rising demand for minimally invasive treatments, product innovation, global expansion, and growing recurring revenues position InMode for resilient long-term growth and margin stability.

Catalysts

About InMode- Designs, develops, manufactures, and markets minimally invasive aesthetic medical products based on its proprietary radio frequency assisted lipolysis and deep subdermal fractional radiofrequency technologies in the United States, Europe, Asia, and internationally.

- Ongoing and escalating regulatory scrutiny, especially in core developed markets and with unpredictable U.S. and global tariff regimes, is set to raise compliance costs and further delay new product launches, constraining long-term revenue growth and squeezing gross margins as regulatory burdens rise.

- Heightened public skepticism towards elective aesthetic procedures, paired with increased cultural and government scrutiny of “wellness fads,” risks a structural drop in demand, driving reduced procedure volumes and a decline in system and consumable revenues over time.

- Significant and sustained wage inflation, along with tightening labor markets for qualified healthcare professionals, is expected to push up procedure costs for providers, suppressing utilization rates of InMode’s systems and thus reducing recurring consumable sales and putting pressure on net earnings.

- Intensifying competition, both from established large medical device companies and new agile entrants, threatens to compress pricing power for InMode’s radiofrequency-focused portfolio, leading to declining average selling prices and ongoing margin erosion in future reporting periods.

- Heavy reliance on international expansion exposes the company to volatile foreign exchange rates and the risk of unpredictable regulatory changes abroad, undermining the stability of revenue contributions and leading to further unpredictability in operating margins and long-term earnings power.

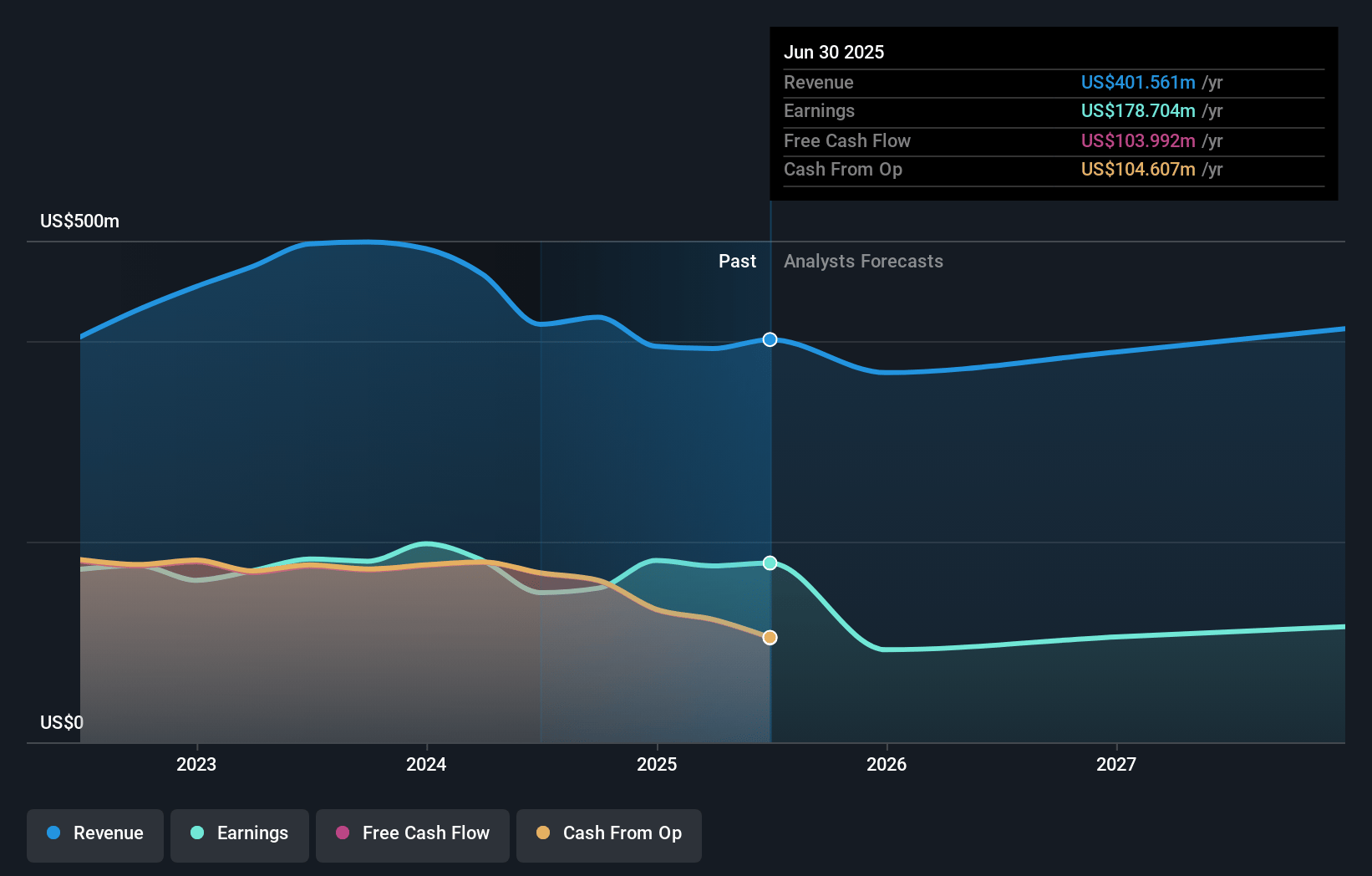

InMode Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more pessimistic perspective on InMode compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming InMode's revenue will decrease by 0.5% annually over the next 3 years.

- The bearish analysts assume that profit margins will shrink from 44.8% today to 22.3% in 3 years time.

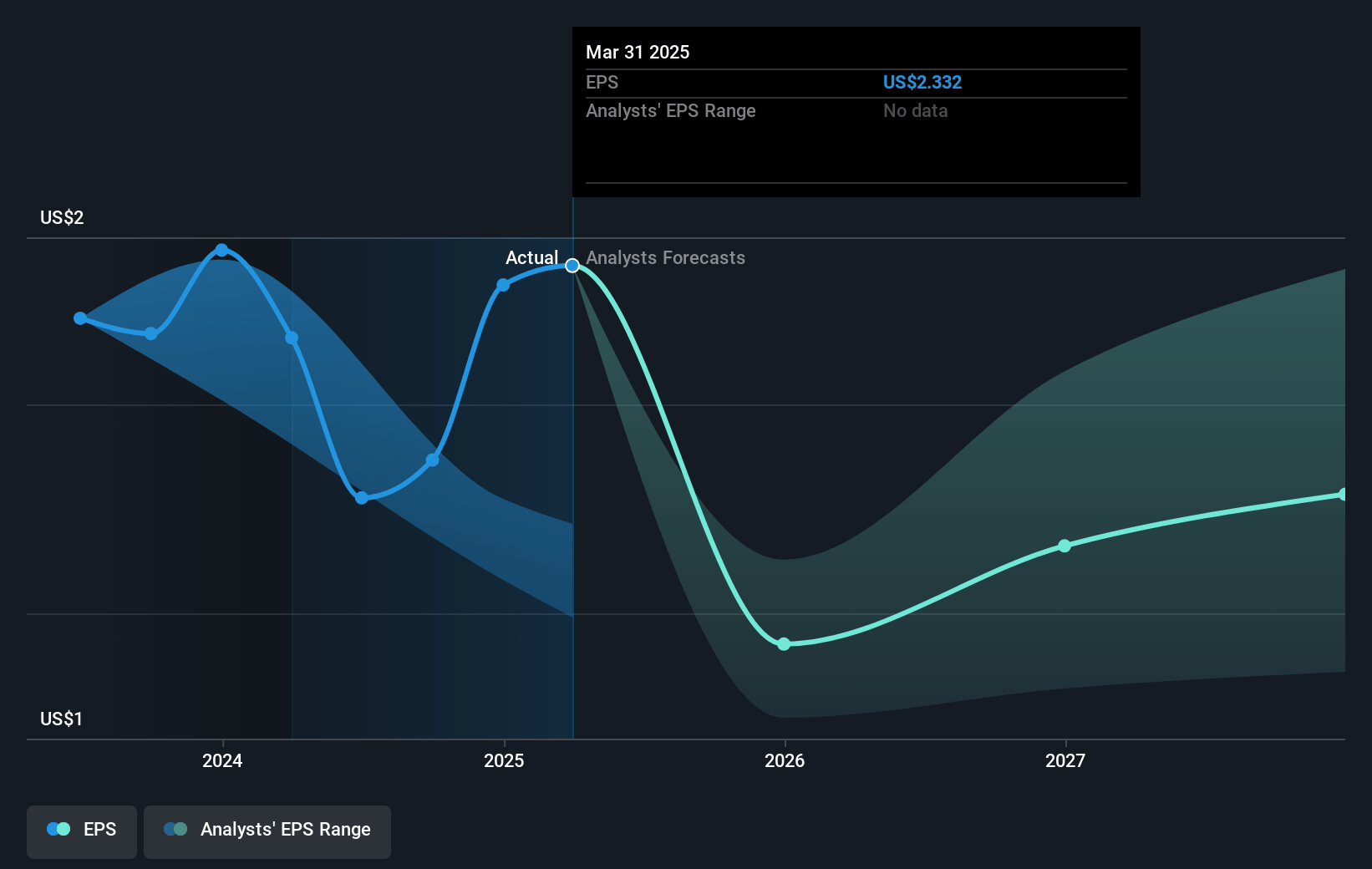

- The bearish analysts expect earnings to reach $86.3 million (and earnings per share of $1.29) by about July 2028, down from $175.8 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 10.5x on those 2028 earnings, up from 5.4x today. This future PE is lower than the current PE for the US Medical Equipment industry at 31.1x.

- Analysts expect the number of shares outstanding to decline by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.08%, as per the Simply Wall St company report.

InMode Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The aging global population and rising focus on self-image are driving long-term increases in demand for minimally invasive aesthetic and wellness treatments, which aligns with InMode’s core technologies and could support steady revenue growth even during periods of temporary cyclical weakness.

- Expanding into new geographic markets, as evidenced by strong recent performance in Europe and ongoing investments in international sales teams, provides diversification and new revenue streams that can offset U.S. market softness, helping to stabilize and potentially boost overall company earnings.

- Continuous product innovation and launch of new platforms, including upcoming entries into the wellness space and recent additions like Ignite and OptimasMAX, position InMode as an industry leader poised to capture additional share and premium pricing, which can underpin gross margin resilience and future revenue growth.

- Increasing recurring revenue from the growing installed base of proprietary devices, particularly from single-use consumables and disposables, enhances revenue visibility and helps smooth earnings volatility even when capital equipment sales slow down.

- Secular and industry trends, such as the shift toward non-surgical, minimally invasive procedures and the broadening of applications in aesthetic medicine, are expanding the addressable market for device-makers like InMode, supporting long-term top-line growth and improving the outlook for margins and net earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bearish price target for InMode is $14.0, which represents the lowest price target estimate amongst analysts. This valuation is based on what can be assumed as the expectations of InMode's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $24.0, and the most bearish reporting a price target of just $14.0.

- In order for you to agree with the bearish analysts, you'd need to believe that by 2028, revenues will be $386.5 million, earnings will come to $86.3 million, and it would be trading on a PE ratio of 10.5x, assuming you use a discount rate of 9.1%.

- Given the current share price of $14.93, the bearish analyst price target of $14.0 is 6.6% lower.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.