Key Takeaways

- Competitive pressures, economic constraints, and client behavior shifts threaten IDEXX's pricing power, core market growth, and recurring revenue streams.

- Regulatory and operational cost increases, alongside innovation challenges, may compress margins and slow long-term earnings growth.

- Strong innovation, international expansion, and resilient recurring revenues position IDEXX for sustained growth and margin improvement despite macroeconomic and market risks.

Catalysts

About IDEXX Laboratories- Develops, manufactures, and distributes products for the companion animal veterinary, livestock and poultry, dairy, and water testing industries in the United States and internationally.

- Long-term growth in IDEXX's core markets is at risk due to rising global economic inequality and pressures on discretionary pet healthcare spending, which could limit the addressable market for diagnostics and put downward pressure on top-line revenue growth over time.

- The company faces intensifying regulatory scrutiny and evolving compliance requirements related to animal health, data privacy, and environmental standards worldwide; these challenges may raise operational costs and erode net margins, particularly as IDEXX expands internationally.

- More affordable competitors and the potential commoditization of veterinary diagnostics threaten IDEXX's ability to sustain premium pricing for its diagnostic tests and instruments, making it increasingly difficult to protect gross margins and long-term profitability.

- Persistent declines in U.S. veterinary clinic visits, coupled with signs of consumer trade-offs in elective procedures and wellness visits, signal that IDEXX may struggle to maintain high growth in recurring diagnostic revenues and software subscriptions, weakening both revenue and earnings prospects even as the installed instrument base grows.

- High innovation and R&D expenditures required to maintain technological leadership may not yield sufficiently differentiated products as new entrants leverage digital and AI solutions, raising the risk that returns on investment will decline and long-term earnings growth will decelerate.

IDEXX Laboratories Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more pessimistic perspective on IDEXX Laboratories compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

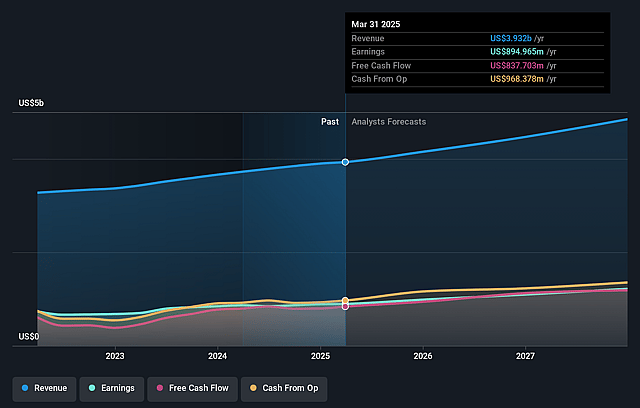

- The bearish analysts are assuming IDEXX Laboratories's revenue will grow by 7.6% annually over the next 3 years.

- The bearish analysts assume that profit margins will increase from 22.8% today to 24.7% in 3 years time.

- The bearish analysts expect earnings to reach $1.2 billion (and earnings per share of $15.06) by about July 2028, up from $895.0 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 29.3x on those 2028 earnings, down from 48.6x today. This future PE is lower than the current PE for the US Medical Equipment industry at 31.1x.

- Analysts expect the number of shares outstanding to decline by 2.29% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.1%, as per the Simply Wall St company report.

IDEXX Laboratories Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Strong long-term secular tailwinds, such as the increasing global pet population (noted at a 3 percent compound annual growth rate since 2019, surpassing historical averages), combined with aging pets and rising standards of care, provide sustained demand for veterinary diagnostics and underpin robust recurring revenue growth.

- The launch and rapid commercial adoption of innovative platforms like IDEXX Cancer Dx and inVue Dx-with thousands of placements and high early customer interest-demonstrate IDEXX's continued ability to innovate and drive both incremental utilization and high-margin consumables revenue, supporting higher operating and net margins over time.

- International expansion is accelerating, highlighted by double-digit install base growth and strong momentum in regions such as Europe and South Korea, which increases the total addressable market and diversifies revenue streams, contributing to top-line growth and reducing dependency on any one geographic market.

- High levels of customer retention (in the high 90s percent range) and growing usage of cloud-based practice management and engagement software provide IDEXX with a resilient, predictable, and sticky recurring revenue base, supporting long-term earnings stability and margin expansion.

- Despite challenging macroeconomic and tariff environments, IDEXX's supply chain resilience, local-for-local lab strategies, and limited exposure to China (less than 1 percent of revenues) enable it to manage cost pressures and operational risks, helping protect profitability and free cash flow conversion even during sector headwinds.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bearish price target for IDEXX Laboratories is $385.0, which represents the lowest price target estimate amongst analysts. This valuation is based on what can be assumed as the expectations of IDEXX Laboratories's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $625.0, and the most bearish reporting a price target of just $385.0.

- In order for you to agree with the bearish analysts, you'd need to believe that by 2028, revenues will be $4.9 billion, earnings will come to $1.2 billion, and it would be trading on a PE ratio of 29.3x, assuming you use a discount rate of 7.1%.

- Given the current share price of $540.68, the bearish analyst price target of $385.0 is 40.4% lower. Despite analysts expecting the underlying buisness to improve, they seem to believe the market's expectations are too high.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.