Narratives are currently in beta

Key Takeaways

- Ensign Group's disciplined acquisitions and skilled local leadership bolster long-term growth, enhancing net margins and earnings.

- Significant same-store occupancy increases reflect meaningful revenue growth potential through organic development and strategic market adaptation.

- Reliance on projections, acquisition complexities, revenue uncertainties from state reimbursements, and competitive acquisitions could impact margins and long-term profitability.

Catalysts

About Ensign Group- Provides skilled nursing, senior living, and rehabilitative services.

- Ensign Group's focus on integrating newly acquired distressed operations into its existing clusters has resulted in earlier-than-expected contributions to revenue and strong performance, highlighting potential future revenue growth from these acquisitions.

- The company has seen a significant increase in same-store occupancies and skilled days across payer sources, which is translating into meaningful revenue growth, indicating a potential for increased revenue and earnings through higher occupancy and skilled mix in the future.

- Ensign's consistent strategy of disciplined acquisitions at attractive prices provides long-term growth opportunities, enhancing net margins and earnings as these lower occupancy operations ramp up.

- The company's development and retention of skilled local leadership teams who innovate and adapt to market needs, such as increasing the skilled mix and acuity, positions Ensign for future earnings growth and improved net margins.

- Ensign's strategy of leveraging organic growth, with 46% of quarterly revenue increases derived organically, suggests a sustained potential for revenue and earnings growth without over-reliance on acquisitions.

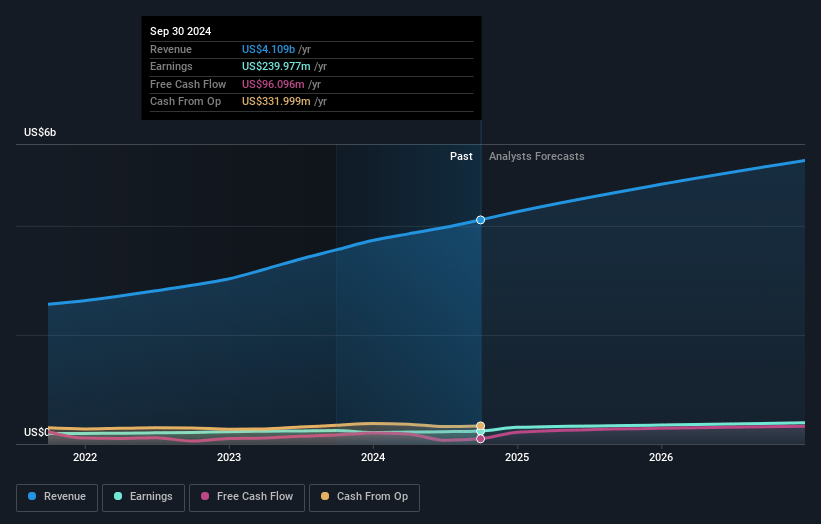

Ensign Group Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Ensign Group's revenue will grow by 11.3% annually over the next 3 years.

- Analysts assume that profit margins will increase from 5.8% today to 7.2% in 3 years time.

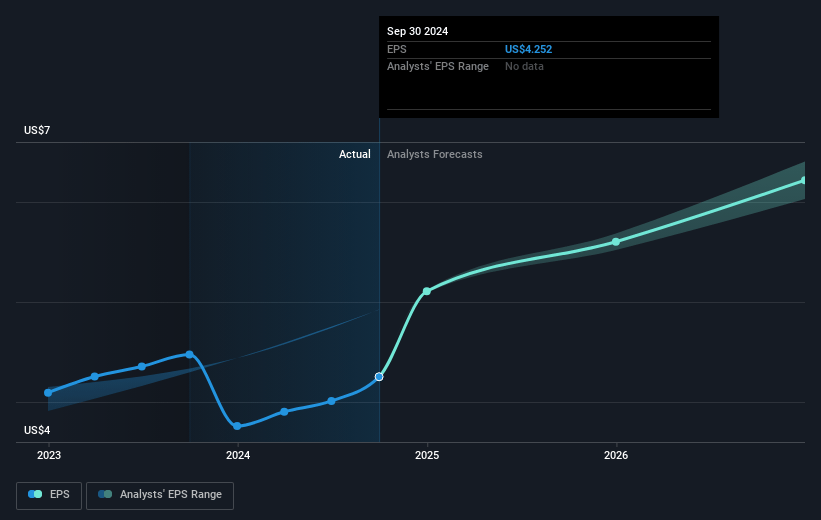

- Analysts expect earnings to reach $408.3 million (and earnings per share of $6.5) by about January 2028, up from $240.0 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 30.2x on those 2028 earnings, down from 33.3x today. This future PE is greater than the current PE for the US Healthcare industry at 23.7x.

- Analysts expect the number of shares outstanding to grow by 3.37% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 5.92%, as per the Simply Wall St company report.

Ensign Group Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The reliance on projections and forward-looking statements introduces uncertainty that can lead to material differences from expected results, impacting earnings and net margins.

- The complexities associated with integrating distressed acquisitions could pose execution risks, potentially affecting revenue stability and operational efficiency.

- Variations in state budgets and reimbursement systems, particularly in Medicare and Medicaid rates, can lead to revenue uncertainties and margin pressures.

- The potential cessation of supplemental payments or changes in funding mechanisms could impact expected revenue streams.

- High competition in acquisition markets and the risk of overpaying for assets could pressure margins and long-term profitability.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $167.5 for Ensign Group based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $5.7 billion, earnings will come to $408.3 million, and it would be trading on a PE ratio of 30.2x, assuming you use a discount rate of 5.9%.

- Given the current share price of $140.37, the analyst's price target of $167.5 is 16.2% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives