Narratives are currently in beta

Key Takeaways

- Strategic international expansion and product innovation could drive future revenue growth by capturing diverse consumer segments and increasing market share.

- Commitment to shareholder value through dividends and share repurchases may enhance investor returns and earnings per share.

- Increased regulation, illegal market dominance, and economic challenges may hinder RLX's revenue and market share, with potential decline in earnings from interest income.

Catalysts

About RLX Technology- Engages in the manufacture and sale of e-vapor products in the People's Republic of China and internationally.

- The expansion into multiple international markets and becoming the leading brand in several countries indicates potential for future revenue growth through increased market share outside China.

- The development of multi-category product lines and innovations to meet local regulations and consumer demands is expected to enhance the company's revenue and gross margins by capturing diverse consumer segments and optimizing costs.

- Improved regulatory compliance and action against illicit products in the Chinese market could lead to higher revenue by reducing unfair competition from non-compliant products.

- The strategic focus on product innovation and tailored solutions for different user segments and international markets is likely to boost earnings by meeting consumer preferences and differentiating the brand from competitors.

- The announcement of cash dividends and commitment to share repurchase programs suggest that the company is focused on shareholder value, potentially leading to an enhanced EPS and attractive returns for investors.

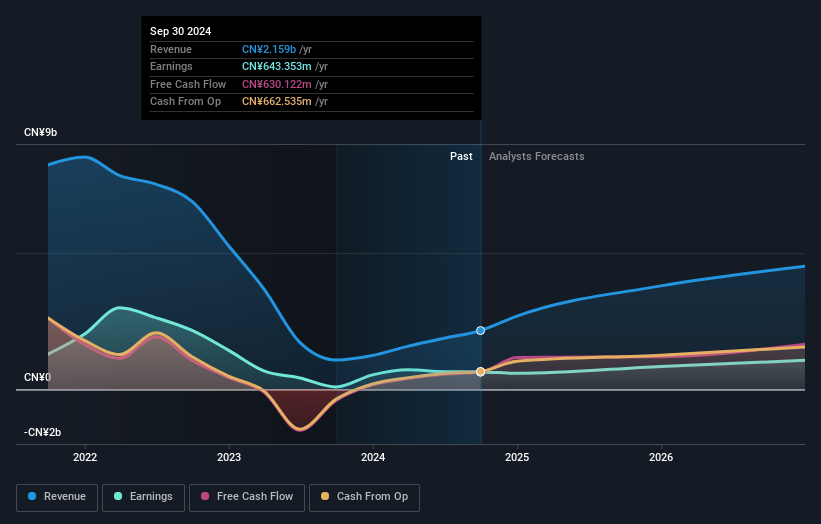

RLX Technology Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming RLX Technology's revenue will grow by 40.1% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 29.8% today to 18.5% in 3 years time.

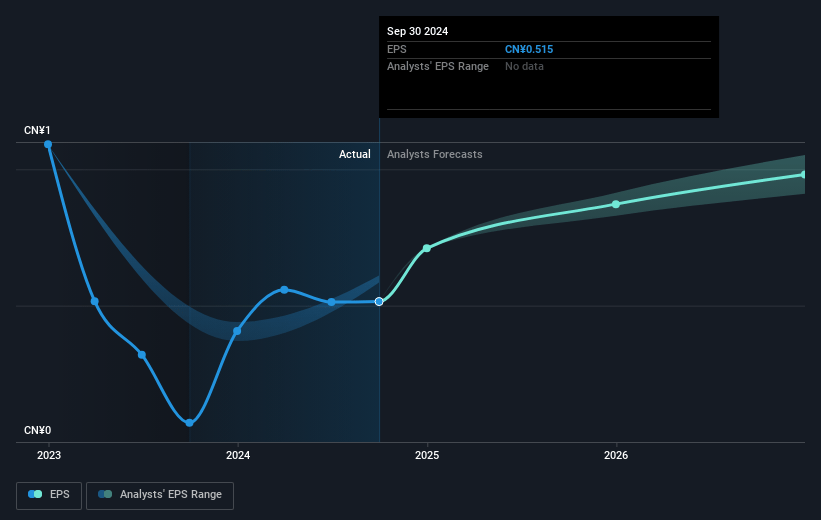

- Analysts expect earnings to reach CN¥1.1 billion (and earnings per share of CN¥1.07) by about January 2028, up from CN¥643.4 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 25.5x on those 2028 earnings, down from 31.1x today. This future PE is greater than the current PE for the US Tobacco industry at 22.4x.

- Analysts expect the number of shares outstanding to decline by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.76%, as per the Simply Wall St company report.

RLX Technology Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Increased regulatory activity, including bans on disposable products and stricter enforcement, may complicate operations and hinder revenue growth in international markets.

- The dominance of illegal e-vapor products in China, capturing 80-90% of the market, poses a significant threat to RLX's market share and revenue in its domestic market.

- Compliance challenges with evolving regulatory frameworks could lead to higher operational costs and impact net margins due to necessary adjustments in business strategies.

- Economic headwinds and conservative consumer behavior in China may affect consumer spending on e-vapor products, potentially impacting revenues.

- Interest income, a substantial part of RLX's earnings, could decline due to anticipated rate cuts, negatively affecting overall earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $3.11 for RLX Technology based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $4.77, and the most bearish reporting a price target of just $2.64.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be CN¥5.9 billion, earnings will come to CN¥1.1 billion, and it would be trading on a PE ratio of 25.5x, assuming you use a discount rate of 6.8%.

- Given the current share price of $2.17, the analyst's price target of $3.11 is 30.2% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives