Last Update08 Oct 25Fair value Decreased 1.57%

Narrative Update on Ingredion

Analysts have lowered their price target for Ingredion from $144 to $130 per share. This reflects a modest downward revision due to updated profit margin and valuation expectations.

Analyst Commentary

Recent research coverage provides updated perspectives on Ingredion’s prospects, highlighting both areas of optimism and points of caution as analysts assess the company’s execution and valuation.

Bullish Takeaways

- Bullish analysts note that Ingredion has demonstrated steady operational performance, supporting stability in its earnings outlook.

- They see ongoing cost management initiatives as a potential driver for improved profit margins over the longer term.

- Resilient demand in core customer segments is viewed as a positive indicator for future revenue streams.

Bearish Takeaways

- Bearish analysts remain cautious about the softer profit margin trajectory reflected in the new price target.

- They highlight continued uncertainties in margin expansion and competitive market conditions that may limit valuation upside.

- There are concerns that near-term catalysts for earnings growth could be constrained, weighing on investor sentiment.

What's in the News

- Ingredion issued updated full-year 2025 guidance, projecting reported EPS in the range of $11.25 to $11.75 and mid-single-digit growth in operating income. Net sales are expected to remain flat, with T&HS volume growth offset by lower price mix and foreign exchange impacts (Key Developments).

- The company provided third quarter 2025 guidance, forecasting net sales to be flat to up low single digits and operating income to be flat to down low single digits compared to the same quarter last year (Key Developments).

- Ingredion’s board of directors declared a quarterly dividend of $0.82 per share, marking the 11th consecutive year of a third quarter dividend increase. The dividend is payable on October 21, 2025 (Key Developments).

- The company has completed the repurchase of 3,062,000 shares, representing 4.68% of shares outstanding, for $369.76 million under its ongoing buyback program as of August 1, 2025 (Key Developments).

- Ingredion announced an upcoming Analyst/Investor Day, offering further insights into strategic direction and company performance (Key Developments).

Valuation Changes

- Fair Value Estimate has decreased slightly from $148.67 to $146.33 per share.

- Discount Rate remains unchanged at 6.78%.

- Revenue Growth projection has edged down marginally from 2.05% to 2.03%.

- Net Profit Margin expectation has risen from 8.95% to 9.57%.

- Future P/E (Price to Earnings) multiple has declined from 15.86x to 14.61x.

Key Takeaways

- Expanding specialty portfolio, innovation, and sustainability focus are driving growth, higher margins, and new business opportunities across strategic food industry segments.

- Operational efficiencies, cost optimization, and targeted investments are boosting profitability and positioning the company for sustained international and long-term expansion.

- Global economic and trade instability, input cost pressures, and declines in legacy product demand threaten revenue and margin growth, heightening reliance on specialty ingredient expansion.

Catalysts

About Ingredion- Manufactures and sells sweeteners, starches, nutrition ingredients, and biomaterial solutions derived from wet milling and processing corn, and other starch-based materials to a range of industries worldwide.

- Strong consumer and customer demand for health and wellness-focused, clean label, and sugar reduction solutions continues to drive double-digit growth in Ingredion's higher-value specialty portfolio, including clean label starches, high-intensity sweeteners, and protein isolates. This trend is expected to sustain above-average revenue and margin growth for the Texture & Healthful Solutions segment.

- Ongoing innovation and investments in R&D-especially in customized formulations and proprietary plant-based ingredients-are widening Ingredion's opportunities with small and medium-sized food brands and insurgent category disruptors, expanding future revenues and allowing for premium pricing that elevates net margins.

- Enhanced operational efficiencies, supply chain digitalization, and cost optimization initiatives have resulted in a structural step-change in segment margins (notably in Texture & Healthful Solutions), with management expecting these higher levels of profitability and operating leverage to persist, improving overall net margins and earnings.

- The company's commitment to sustainable ingredient sourcing and strong ESG credentials is attracting new business from large CPG customers seeking to reformulate for environmental and regulatory objectives. This alignment with evolving food industry standards opens new revenue streams and supports long-term margin resilience.

- Selective capital allocation to high-return organic growth projects and sustained share buybacks, coupled with further international expansion (even amidst temporary LATAM headwinds), position Ingredion to accelerate both top-line growth and EPS over the long run, as secular themes around a growing middle-class and dietary shifts in emerging markets resume momentum.

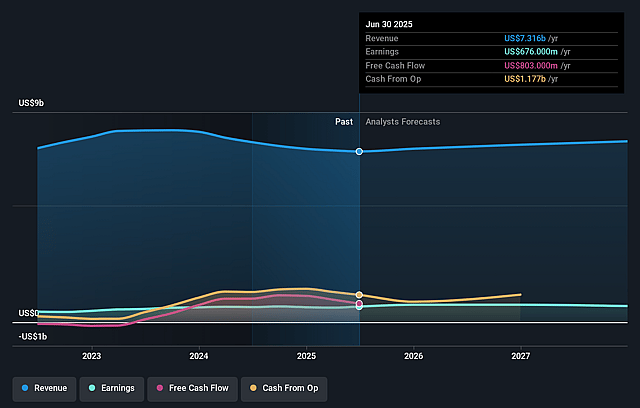

Ingredion Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Ingredion's revenue will grow by 2.0% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 9.2% today to 9.0% in 3 years time.

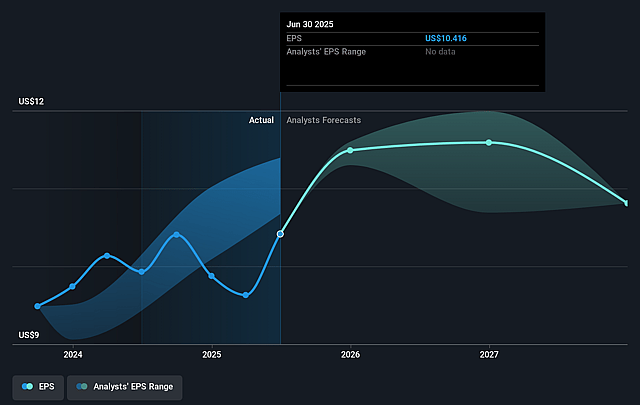

- Analysts expect earnings to reach $696.0 million (and earnings per share of $10.82) by about September 2028, up from $676.0 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 15.9x on those 2028 earnings, up from 12.1x today. This future PE is lower than the current PE for the US Food industry at 19.5x.

- Analysts expect the number of shares outstanding to decline by 1.5% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.78%, as per the Simply Wall St company report.

Ingredion Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Economic and currency volatility in key emerging markets, especially in LATAM (notably Argentina, Brazil, and Mexico), is contributing to declining volumes and negative foreign exchange impacts, which could lead to persistent revenue and earnings headwinds if macroeconomic weakness and currency depreciation continue.

- Ongoing tariff uncertainties and global trade friction create unpredictability for Ingredion and its customers, leading to conservative guidance, customer inventory rebalancing, and the risk of indirect impacts on demand that may pressure near-term and longer-term revenues and margins.

- The company continues to face price/mix headwinds across major business segments due to pass-through of lower corn and input costs, raising concerns that Ingredion's ability to maintain or grow top-line sales and net income will become more challenging if commodity cost deflation persists.

- Weaknesses in legacy product demand-such as industrial starches (impacted by soft box demand and tariffs) and high fructose corn syrup (HFCS; at risk from consumer trends toward natural or clean-label sweeteners)-put pressure on Ingredion's core revenues and increase the company's dependence on breakout growth from new, higher-margin specialty ingredients.

- While margins in Texture & Healthful Solutions have reached record highs, management acknowledged some results reflected exceptional one-time raw material procurement benefits and cost absorption, and they are signaling caution about sustaining current margin levels amid sourcing, transportation, and potential tariff challenges that could lead to net margin contraction in future periods.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $148.667 for Ingredion based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $168.0, and the most bearish reporting a price target of just $140.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $7.8 billion, earnings will come to $696.0 million, and it would be trading on a PE ratio of 15.9x, assuming you use a discount rate of 6.8%.

- Given the current share price of $127.07, the analyst price target of $148.67 is 14.5% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.