Key Takeaways

- Growth in health-focused products and innovation aligns with consumer trends, supporting premium pricing and nationwide expansion.

- Operational efficiencies and targeted new launches in snacks and portion sizes improve margins and capitalize on changing demographic needs.

- Shifting consumer preferences, category decline, cost pressures, and lack of diversification threaten Flowers Foods’ long-term revenue, margins, and competitiveness.

Catalysts

About Flowers Foods- Produces and markets packaged bakery food products in the United States.

- An expected rebound in consumer health and confidence is likely to drive renewed demand for packaged baked goods, positioning Flowers Foods to capture revenue growth as consumers return to higher levels of consumption and favor convenience-oriented meal solutions.

- Expansion and innovation within health-focused product lines—including Dave’s Killer Bread, Canyon Bakehouse, Keto offerings, and the recent Simple Mills acquisition—directly support shifting consumer preferences towards wellness and clean-label foods, which should lift both revenue and gross margins as premium products are scaled nationwide.

- Ongoing investments in automation, supply chain optimization, and bakery rationalization are projected to improve operational efficiency and lower production costs over time, providing a pathway for EBITDA margin expansion and enhanced net income.

- Strategic new product launches in high-growth adjacencies, such as snacking and on-trend innovations like Wonder cake, are achieving early distribution gains and incremental shelf presence, supporting incremental sales growth and providing a strong foundation for future earnings.

- The successful pursuit of value-added offerings tailored to smaller households and evolving demographic trends—such as smaller loaf sizes—enables Flowers Foods to capture untapped volume opportunities and maintain stable unit share, which will underpin long-term revenue stability and growth.

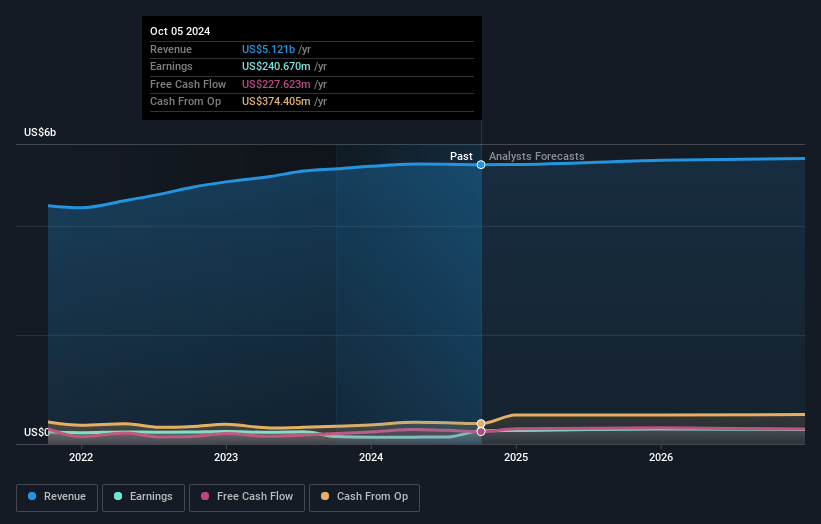

Flowers Foods Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more optimistic perspective on Flowers Foods compared to the consensus, based on a Fair Value that aligns with the bullish cohort of analysts.

- The bullish analysts are assuming Flowers Foods's revenue will grow by 2.9% annually over the next 3 years.

- The bullish analysts assume that profit margins will increase from 4.5% today to 4.8% in 3 years time.

- The bullish analysts expect earnings to reach $265.7 million (and earnings per share of $1.25) by about July 2028, up from $228.1 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bullish analyst cohort, the company would need to trade at a PE ratio of 21.1x on those 2028 earnings, up from 14.6x today. This future PE is greater than the current PE for the US Food industry at 19.5x.

- Analysts expect the number of shares outstanding to grow by 0.26% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.4%, as per the Simply Wall St company report.

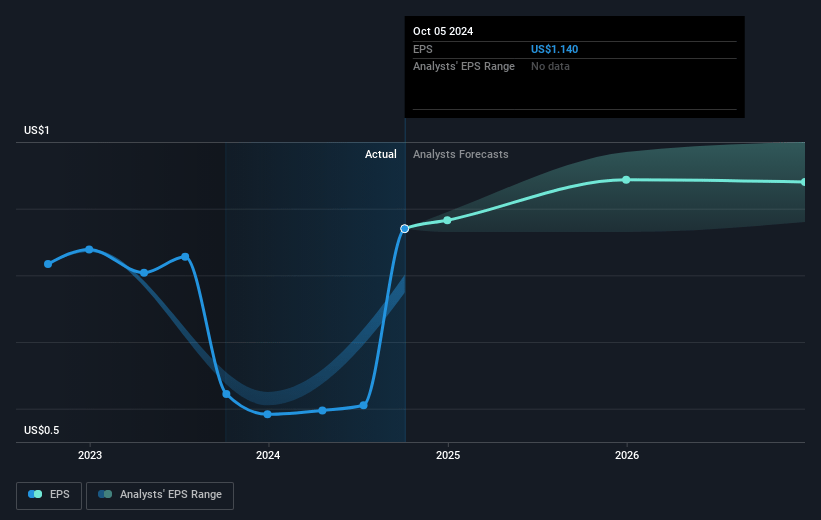

Flowers Foods Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The ongoing shift in consumer health trends toward low-carb, gluten-free, and alternative diets, compounded by the rising adoption of GLP-1 drugs and structural changes in eating habits, is driving persistent declines in the traditional packaged bread category, posing a significant long-term risk to Flowers Foods’ core revenues.

- Flowers Foods’ overexposure to traditional loaf and white bread products, which are being squeezed between premium and value segments and experiencing pronounced volume declines, could accelerate share losses and undermine revenue stability if the company fails to diversify meaningfully beyond its legacy brands.

- Intensifying pricing pressure due to retailer consolidation and increased promotional activity, along with a consumer environment focused on value, may trigger further margin compression and limit Flowers Foods’ ability to improve EBITDA margins in the long-term.

- Heightened vulnerability to tariffs and rising input costs, especially given the company’s reliance on imported ingredients such as sugar, wheat gluten, and palm oil, could increase cost of goods sold and erode net margins if Flowers Foods is unable to fully offset these increases through cost savings or price adjustments.

- Flowers Foods faces operational headwinds such as elevated fixed costs and limited automation, evidenced by ongoing bakery closures and the slow pace of supply chain optimization, that may hinder its agility and negatively impact operating margins and earnings over time.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bullish price target for Flowers Foods is $22.0, which is the highest price target estimate amongst analysts. This valuation is based on what can be assumed as the expectations of Flowers Foods's future earnings growth, profit margins and other risk factors from analysts on the bullish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $22.0, and the most bearish reporting a price target of just $14.0.

- In order for you to agree with the bullish analysts, you'd need to believe that by 2028, revenues will be $5.5 billion, earnings will come to $265.7 million, and it would be trading on a PE ratio of 21.1x, assuming you use a discount rate of 6.4%.

- Given the current share price of $15.77, the bullish analyst price target of $22.0 is 28.3% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystHighTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystHighTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystHighTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.