Key Takeaways

- Strategic acquisitions and partnerships aim to broaden market reach and improve operational efficiencies, enhancing revenue growth and margin expansion.

- Innovative products and expanded distribution channels target new consumer segments, potentially boosting market penetration and sales volume.

- Fluctuating inventory management, regulatory delays, and intense competition may impact revenue stability, margins, and earnings growth for Celsius Holdings in the energy drink market.

Catalysts

About Celsius Holdings- Develops, processes, manufactures, markets, sells, and distributes functional energy drinks in the United States, North America, Europe, the Asia Pacific, and internationally.

- The acquisition of Alani Nu is expected to enhance Celsius's platform with complementary, profitable, better-for-you lifestyle energy brands, potentially driving additional revenue by tapping into a new consumer segment focused on health and wellness, particularly among millennials and Gen Z. This could improve revenue growth due to expanded audience reach and portfolio diversification.

- The launch of CELSIUS HYDRATION and new product varieties and flavors is projected to excite consumers and increase daily product usage occasions. This innovation in the product lineup could drive revenue growth and improved market penetration.

- The expansion of distribution, including availability in Subway restaurants and Home Depot, is likely to increase Celsius's sales volume and visibility, potentially impacting top-line revenue growth positively.

- Collaborating with Pepsi on optimizing supply chain operations and enhancing distribution could improve operational efficiencies and cost management, which may support gross margin improvements and net margin expansion in the long term.

- The acquisition of co-packer Big Beverages aims to provide greater control over supply chain and innovation capabilities, potentially realizing financial benefits and cost synergies that could lead to EBITDA margin improvements over time.

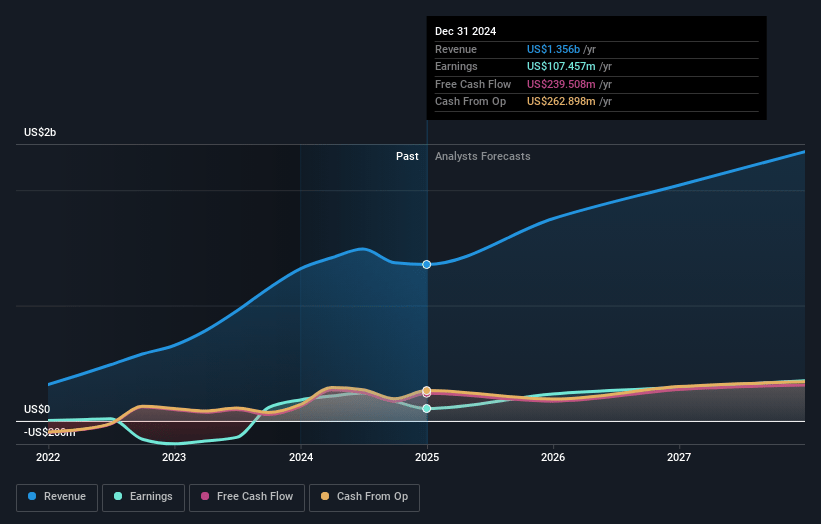

Celsius Holdings Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Celsius Holdings's revenue will grow by 19.9% annually over the next 3 years.

- Analysts assume that profit margins will increase from 7.9% today to 14.9% in 3 years time.

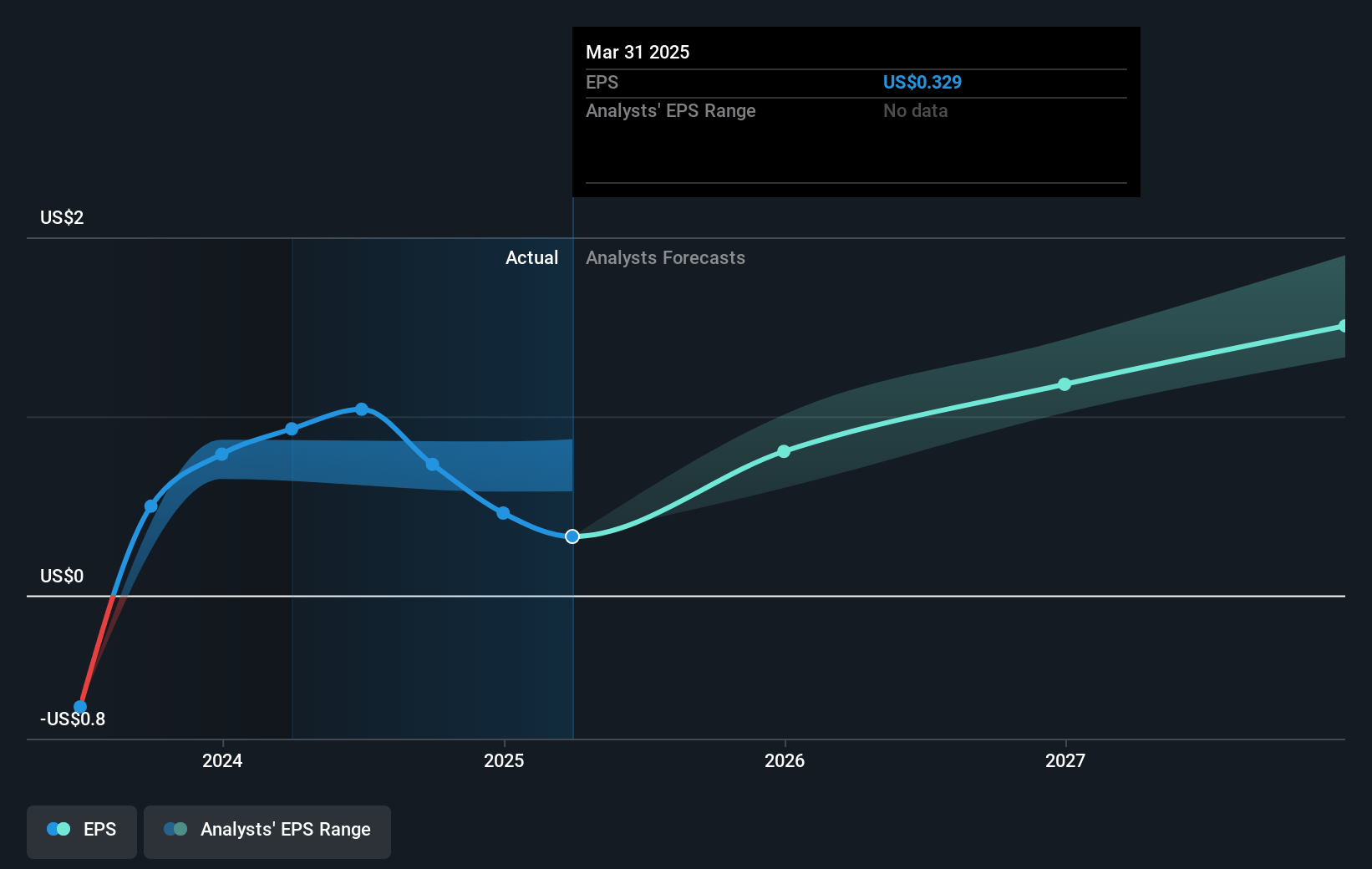

- Analysts expect earnings to reach $348.3 million (and earnings per share of $1.38) by about March 2028, up from $107.5 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $406.0 million in earnings, and the most bearish expecting $250.7 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 32.4x on those 2028 earnings, down from 66.5x today. This future PE is greater than the current PE for the US Beverage industry at 28.1x.

- Analysts expect the number of shares outstanding to grow by 0.88% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.21%, as per the Simply Wall St company report.

Celsius Holdings Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The fluctuating inventory management and promotional allowances with key distributors like Pepsi could impact Celsius's revenue stability and adjusted EBITDA in the short term.

- Legal and restructuring costs, along with one-time charges related to co-packers, have increased SG&A expenses significantly, impacting net income and potentially affecting net margins.

- Any potential complications or delays in regulatory approvals for the acquisition of Alani Nu could negatively affect expected synergistic growth and contribute to uncertainty in projected earnings.

- Intense competition and increased promotional activities in the sugar-free energy drink market could compress gross margins as major competitors release competing products.

- The successful integration of Alani Nu, including managing potential distribution changes and consumer base overlap, will be crucial; any challenges here could disrupt both revenue streams and earnings projections.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $39.105 for Celsius Holdings based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $62.0, and the most bearish reporting a price target of just $26.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $2.3 billion, earnings will come to $348.3 million, and it would be trading on a PE ratio of 32.4x, assuming you use a discount rate of 6.2%.

- Given the current share price of $30.37, the analyst price target of $39.1 is 22.3% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.