Key Takeaways

- Accelerating environmental regulations and new technologies could drive up costs, require rapid investments, and challenge Scorpio's earnings and industry position.

- Shifting energy demand and decarbonization present significant risks to long-term revenue stability despite current industry supply constraints and robust shareholder returns.

- Geopolitical instability, regulatory changes, demand uncertainty, rising costs, and industry overcapacity threaten future profitability and expose the company to long-term operational and market risks.

Catalysts

About Scorpio Tankers- Engages in the seaborne transportation of crude oil and refined petroleum products worldwide.

- While Scorpio Tankers benefits from a young, fuel-efficient fleet and ongoing retirement of older, less efficient vessels in the industry may support higher freight rates and improved margins, environmental regulations could accelerate fleet renewal requirements and drive up capital and compliance costs, putting pressure on long-term net margins and capital expenditure.

- Although persistent global demand for refined products and the redistribution of refining capacity to export-oriented regions are increasing trade distances, the eventual acceleration of global decarbonization efforts and adoption of alternative energy sources could structurally reduce refined oil product consumption, negatively impacting core revenue growth and utilization in the longer term.

- Despite Scorpio's strong balance sheet, significant liquidity and consistent capital discipline, tighter ESG mandates and increasing regulatory scrutiny may restrict future access to low-cost capital, raising financing costs, and limiting financial flexibility even as shareholder returns remain a near-term focus.

- While ton-mile demand is underpinned by ongoing refinery closures in developed markets and a lack of new capacity in emerging economies, any major technological disruption-such as the rapid adoption of new green shipping fuels or autonomous vessels-could require unexpected reinvestment and threaten Scorpio's industry leadership, constraining future earnings and return on assets.

- Even as long-term product tanker supply growth remains constrained by limited newbuild activity and increased scrapping of aged vessels, the risk of demand destruction from a faster-than-anticipated energy transition or sharply lower oil product consumption in emerging markets could undermine the anticipated favorable rate environment, resulting in revenue and cash flow volatility.

Scorpio Tankers Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more pessimistic perspective on Scorpio Tankers compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

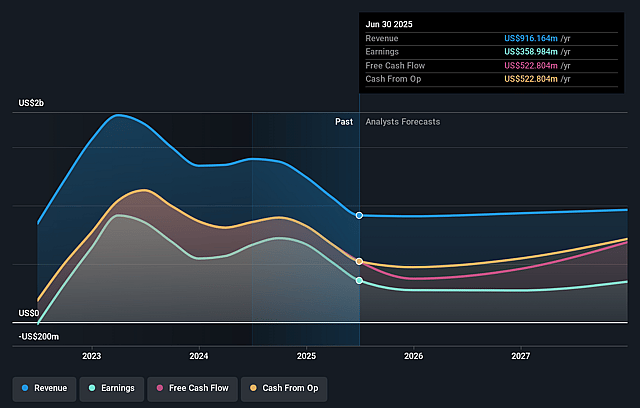

- The bearish analysts are assuming Scorpio Tankers's revenue will decrease by 2.6% annually over the next 3 years.

- The bearish analysts assume that profit margins will shrink from 39.2% today to 21.7% in 3 years time.

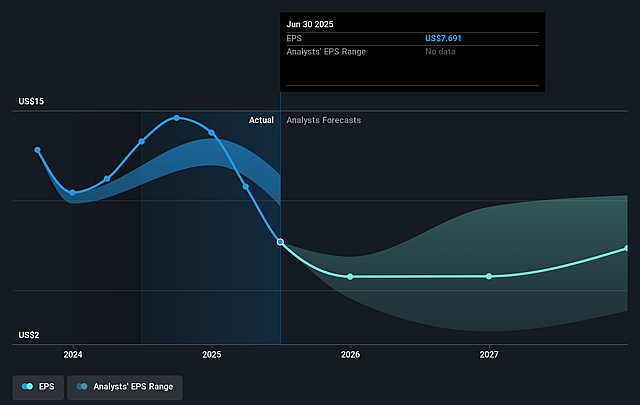

- The bearish analysts expect earnings to reach $183.7 million (and earnings per share of $3.82) by about August 2028, down from $359.0 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 13.7x on those 2028 earnings, up from 6.0x today. This future PE is greater than the current PE for the US Oil and Gas industry at 13.2x.

- Analysts expect the number of shares outstanding to decline by 5.45% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.67%, as per the Simply Wall St company report.

Scorpio Tankers Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The company emphasized ongoing and unresolved macroeconomic, policy, and geopolitical risks, such as tariffs, uncertainty between major economic blocs like Europe and China, and continuing instability in regions like Russia-Ukraine and the Middle East, which could disrupt trade flows and negatively impact Scorpio Tankers' revenues and cash flow in the long term.

- Despite current demand strength, executives remain cautious about capital allocation due to global uncertainty, indicating that unforeseen economic slowdowns or demand shocks could erode shipping rates and compress future earnings.

- The company acknowledges that vessel operating expenses are temporarily lower due to recent dry docks, but cautions that costs will rise again over time from natural wear and tear, and stricter regulatory requirements may further increase OpEx, leading to potential margin compression in future periods.

- Long-term energy transition trends are mentioned as a source of uncertainty, with the company engaging in pilot projects for carbon capture but expressing skepticism about rapid shifts to new propulsion or fuel technologies, leaving Scorpio Tankers exposed to structural decline in demand for oil products and possible asset obsolescence, which would directly impact fleet utilization and long-term revenue potential.

- There is a significant product tanker order book at 20% of fleet size, and while management downplays near-term oversupply risk due to aging vessels and crude/product market dynamics, a persistent imbalance or sharp increase in newbuild orders-combined with declining demand-could drive overcapacity, suppress charter rates, and erode industry-wide profitability, including Scorpio's earnings and return on invested capital.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bearish price target for Scorpio Tankers is $49.0, which represents the lowest price target estimate amongst analysts. This valuation is based on what can be assumed as the expectations of Scorpio Tankers's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $75.0, and the most bearish reporting a price target of just $49.0.

- In order for you to agree with the bearish analysts, you'd need to believe that by 2028, revenues will be $846.1 million, earnings will come to $183.7 million, and it would be trading on a PE ratio of 13.7x, assuming you use a discount rate of 9.7%.

- Given the current share price of $45.7, the bearish analyst price target of $49.0 is 6.7% higher. Despite analysts expecting the underlying buisness to decline, they seem to believe it's more valuable than what the market thinks.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.