Last Update 06 Dec 25

NBR: Offshore Cycle Normalization Will Likely Cap Gains Despite Recent Optimism

Analysts have modestly increased their price target on Nabors Industries, reflecting a recalibrated discount rate and generally constructive Street research citing improved international growth, stronger balance sheet leverage from the $625M Quail Tools sale, and updated guidance that collectively support a fair value estimate near $51 per share.

Analyst Commentary

Street research remains broadly constructive on Nabors Industries, with several firms lifting their price targets in response to stronger fundamentals, while still highlighting execution and cycle risk over the medium term.

Bullish Takeaways

- Bullish analysts point to year over year growth in international markets as a key driver of higher earnings power, supporting the recent upward revisions to fair value estimates.

- The $625M Quail Tools divestiture is seen as materially improving financial leverage, enhancing balance sheet flexibility for capital allocation and debt reduction.

- Updated guidance and recent results are viewed as broadly aligned with expectations, reinforcing confidence that management can execute on its multi year growth and margin expansion plans.

- The sequence of target increases into the mid 50s and mid 60s per share is framed as recognition that Nabors is better positioned in the current Energy Services and Equipment cycle than previously modeled.

Bearish Takeaways

- Bearish analysts maintain more cautious ratings despite raising their targets, reflecting concern that current valuation already discounts much of the expected operational improvement.

- There is explicit focus on potential downside to performance estimates in 2026, with some seeing risk that the current drilling upcycle could normalize faster than embedded in forecasts.

- More conservative views stress that guidance upgrades are incremental rather than transformational, leaving limited room for error if international growth moderates or pricing power softens.

- Residual leverage and capital intensity in the business model are cited as ongoing constraints, with downside risk if macro conditions weaken or if free cash flow underdelivers against current projections.

What's in the News

- The Trump administration is reportedly drafting a plan to resume offshore oil drilling off California between 2027 and 2030, potentially boosting activity and equipment demand for drillers including Nabors Industries, as well as peers such as Baker Hughes, Halliburton and SLB (Washington Post)

- Caturus Energy has awarded Nabors a multi year contract for its high spec PACE X Ultra X33 rig, supporting Nabors position in advanced onshore drilling and high pressure, long lateral wells in the Eagle Ford and Austin Chalk (company announcement)

- The X33 deployment incorporates natural gas powered Cat Dynamic Gas Blending technology, highlighting Nabors role in lowering fuel costs and emissions intensity in challenging drilling environments (company announcement)

- Nabors has completed its long running share repurchase program initiated in 2015, retiring a total of 14,012,000 shares for approximately $121 million, with no additional shares repurchased in the most recent quarter (company filing)

Valuation Changes

- Fair Value Estimate is unchanged at approximately $51.13 per share, indicating no material revision to the core valuation target.

- The Discount Rate has fallen modestly from 12.50 percent to approximately 12.07 percent, reflecting slightly lower perceived risk in the cash flow outlook.

- Revenue Growth is effectively unchanged at about 3.96 percent, signaling stable assumptions for top line expansion.

- Net Profit Margin is essentially flat at roughly 6.63 percent, indicating no meaningful change in long term profitability expectations.

- The Future P/E has decreased slightly from about 533.1x to roughly 527.1x, pointing to a marginally less demanding valuation multiple on forward earnings.

Key Takeaways

- Strong global energy demand and energy security initiatives are driving multi-year drilling contracts, ensuring revenue stability and growth opportunities across key regions.

- Technological advancements and successful integration of acquisitions are boosting margins, expanding market presence, and enhancing free cash flow for potential shareholder returns.

- Ongoing margin pressure, international uncertainty, high capital needs, slow diversification, and heavy debt expose Nabors to significant operational and financial vulnerability amid sector headwinds.

Catalysts

About Nabors Industries- Provides drilling and drilling-related services for land-based and offshore oil and natural gas wells in the United States and internationally.

- Robust global energy demand growth-especially for natural gas in emerging markets-paired with increasing LNG exports supports ongoing and future drilling activity across key geographies where Nabors operates, underpinning long-term revenue stability and growth potential.

- The acceleration of national energy security initiatives, particularly in regions like the Middle East, is driving significant new multi-year drilling rig awards (e.g., SANAD joint venture's 10-year, 50-rig program with firm deployment milestones), providing unmatched contract visibility and undergirding multi-year backlog, which enhances future earnings visibility.

- Rising industry adoption of automation, digitalization, and advanced data analytics is increasing demand for technologically superior drilling solutions-a core offering through Nabors' Drilling Solutions and proprietary SmartRig/performance automation platforms-enabling premium pricing and improving margin expansion prospects.

- The strategic integration of Parker Wellbore is delivering acquisition synergies above initial targets and strengthening Nabors' presence in high-value regions and segments (such as offshore, Alaska, and the Middle East), supporting EBITDA growth and opening new revenue streams.

- Ongoing focus on deleveraging, disciplined capital allocation, and improved free cash flow generation-supported by stable or increasing margins as operational efficiencies are realized-positions Nabors to lower interest costs, enhance net income, and potentially return capital to shareholders (e.g., through buybacks or dividends).

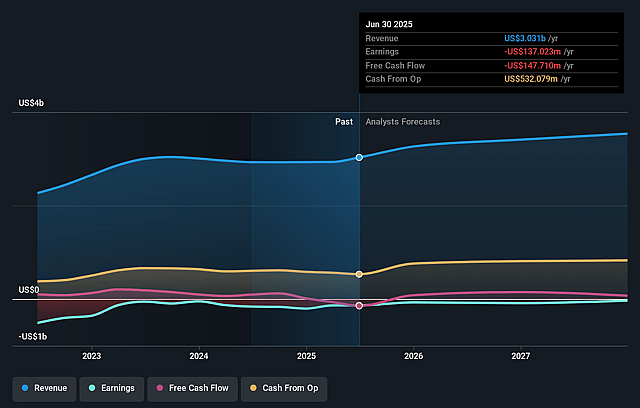

Nabors Industries Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Nabors Industries's revenue will grow by 4.5% annually over the next 3 years.

- Analysts are not forecasting that Nabors Industries will become profitable in next 3 years. To represent the Analyst Price Target as a Future PE Valuation we will estimate Nabors Industries's profit margin will increase from -4.5% to the average US Energy Services industry of 7.0% in 3 years.

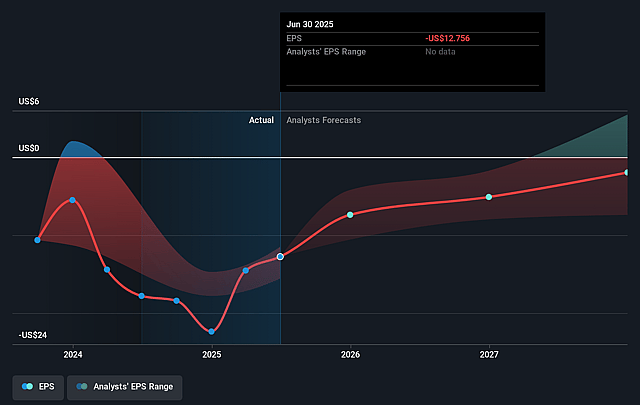

- If Nabors Industries's profit margin were to converge on the industry average, you could expect earnings to reach $243.3 million (and earnings per share of $14.31) by about September 2028, up from $-137.0 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 3.4x on those 2028 earnings, up from -3.8x today. This future PE is lower than the current PE for the US Energy Services industry at 14.6x.

- Analysts expect the number of shares outstanding to grow by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.29%, as per the Simply Wall St company report.

Nabors Industries Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Persistent margin pressure in the U.S. Lower 48, with daily rig margins continuing to decline due to contract renewals at lower day rates and ongoing operator consolidation in oil basins, which could lead to further reductions in drilling activity and weaker revenue and EBITDA from this segment.

- Uncertainty and softening in key international markets, notably with Saudi Arabia's idling of land rigs and Mexico's investment cutbacks and slow receivables collections, increasing the risk of reduced international asset utilization and impairing revenue consistency and free cash flow.

- Elevated and growing capital expenditure requirements, driven by newbuild programs in the Middle East, recertification, and fleet expansion, could strain free cash flow and increase the risk of overextension, especially if rig deployments or contract wins are delayed.

- Dependency on oil & gas drilling demand and the slow pace of diversification into new energy or production-related services, leaving Nabors exposed to longer-term secular headwinds like decarbonization, energy transition, and potential regulatory tightening, which could erode future revenue streams and net margins if the industry shifts accelerate.

- High absolute debt levels, with free cash flow gains prioritized for debt reduction and significant upcoming maturities, mean any market or operational setback could threaten the company's ability to refinance on favorable terms, impact interest costs, or constrain net income available to shareholders.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $38.111 for Nabors Industries based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $50.0, and the most bearish reporting a price target of just $28.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $3.5 billion, earnings will come to $243.3 million, and it would be trading on a PE ratio of 3.4x, assuming you use a discount rate of 8.3%.

- Given the current share price of $35.33, the analyst price target of $38.11 is 7.3% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Nabors Industries?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.