Last Update01 May 25Fair value Decreased 2.79%

AnalystConsensusTarget has decreased revenue growth from 12.8% to 10.5%, increased profit margin from 10.7% to 20.2% and decreased future PE multiple from 20.9x to 10.4x.

Read more...Key Takeaways

- Focus on diversified U.S. acreage, technological advances, and strong operator partnerships drives resilient production growth, lower costs, and enhanced profit margins.

- Conservative financial strategy and favorable policy environment ensure flexibility, reduce regulatory risks, and support sustainable shareholder returns.

- Heavy dependence on mature oil assets, external operators, and acquisitions, combined with energy transition pressures, poses significant risks to growth, margins, and long-term value.

Catalysts

About Granite Ridge Resources- Operates as a non-operated oil and natural gas exploration and production company.

- Persistent global energy demand growth and delays in the energy transition are expected to sustain oil and gas consumption over the long term, supporting stable or higher commodity prices and enabling Granite Ridge to maintain steady or increasing revenues and robust free cash flow.

- Granite Ridge’s granular focus on diversified, non-operated and Operated Partnership acreage in prolific U.S. basins positions the company to benefit from strong and resilient production growth (16% forecasted for 2025), while leveraging scale to drive repeatable cost structure improvements and higher net margins.

- Recent advances in drilling and completions technology, combined with best-in-class operator partnerships, are reducing per-unit operating costs and driving well productivity above expectations, enhancing profitability even during periods of commodity price volatility and supporting higher future earnings.

- The industry’s heightened focus on energy security and domestic production underpins favorable policy sentiment and capital allocation, potentially lowering regulatory risks and operational costs for Granite Ridge, which could support expanding net margins over time.

- Conservative capital allocation, a robust hedging program, and a commitment to maintaining low leverage provide Granite Ridge with substantial financial flexibility; this optionality allows the company to adapt quickly to market conditions, secure accretive acquisitions, and support strong shareholder returns—bolstering long-term earnings and dividend sustainability.

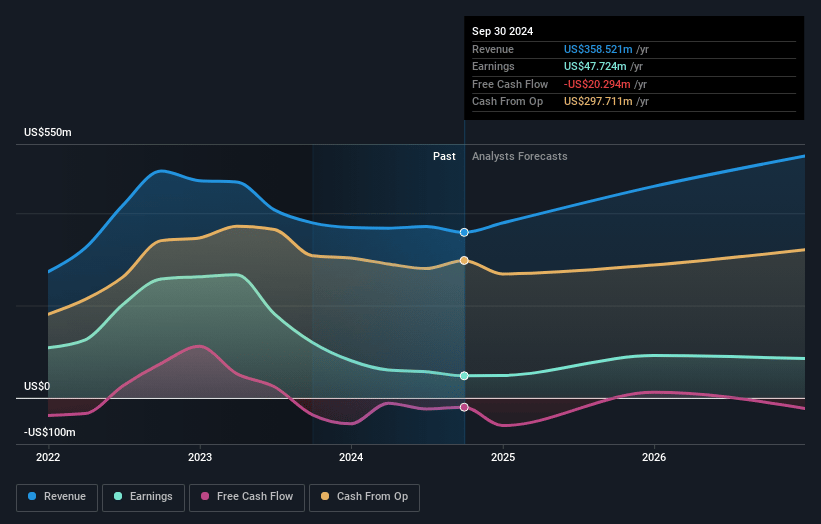

Granite Ridge Resources Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Granite Ridge Resources's revenue will grow by 10.5% annually over the next 3 years.

- Analysts assume that profit margins will increase from 3.1% today to 20.2% in 3 years time.

- Analysts expect earnings to reach $106.3 million (and earnings per share of $0.54) by about May 2028, up from $12.1 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 10.4x on those 2028 earnings, down from 61.2x today. This future PE is lower than the current PE for the US Oil and Gas industry at 12.2x.

- Analysts expect the number of shares outstanding to grow by 0.28% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.53%, as per the Simply Wall St company report.

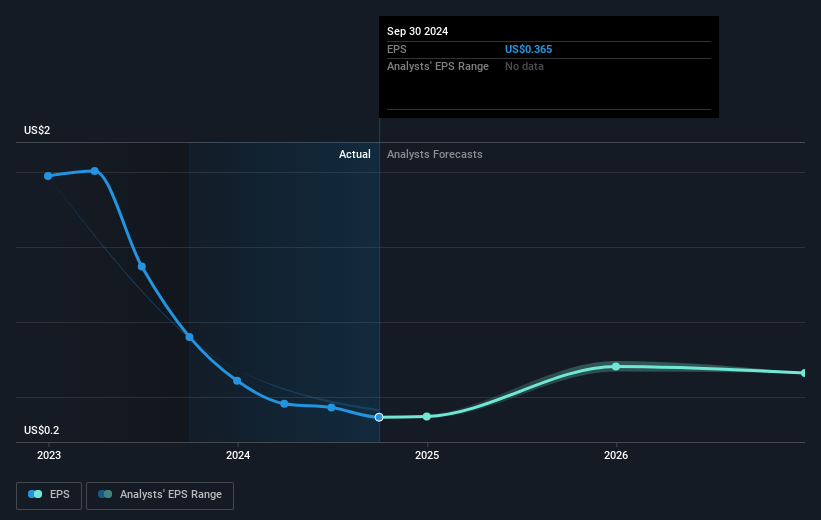

Granite Ridge Resources Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Granite Ridge Resources' long-term growth is exposed to the accelerating global transition toward renewable energy and electrification, which could erode oil and gas demand over time and compress revenues and asset values.

- The company’s increasing reliance on operated partnerships (expected to receive ~60% of capital allocation in 2025) is heavily concentrated in mature U.S. basins like the Permian; these plays may suffer from declining well productivity and require sustained high reinvestment rates, threatening long-term reserve replacement and putting downward pressure on earnings.

- As a non-operator for much of its production, Granite Ridge often lacks control over well timing, operational efficiency, and cost structures—introducing unpredictable capital outlays and potentially higher operating costs, which could compress net margins.

- The positive impact from recent gas price spikes may not be sustainable due to long-term demographic and regulatory shifts, including increased EV adoption, stricter ESG mandates, and potential carbon pricing—all of which can restrict access to capital, increase compliance costs, and curtail future revenue opportunities.

- Overreliance on acquisitions to drive growth, especially with rising competition and asset prices in key basins (evidenced by the “price of poker going up”), raises the risk of overpayment, asset underperformance, and eventual impairments—which could negatively impact future ROIC, earnings, and shareholder value.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $6.96 for Granite Ridge Resources based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $9.0, and the most bearish reporting a price target of just $5.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $527.1 million, earnings will come to $106.3 million, and it would be trading on a PE ratio of 10.4x, assuming you use a discount rate of 6.5%.

- Given the current share price of $5.66, the analyst price target of $6.96 is 18.7% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.