Key Takeaways

- Accelerating global decarbonization and competitive renewables threaten Peabody's long-term coal demand, constraining future revenue growth and earnings stability.

- Regulatory scrutiny, environmental liabilities, and commodity volatility elevate operational risk and may limit future cash flow and valuation upside.

- Regulatory pressures, volatile coal demand, and energy transition trends threaten Peabody's core revenues, margins, and growth opportunities while raising operational and strategic risks.

Catalysts

About Peabody Energy- Engages in coal mining business.

- Although Peabody is benefitting from near-term policy support in the U.S. and ongoing energy demand growth in emerging markets, the company faces long-term risk from accelerating global decarbonization efforts and the widespread retirement of coal-fired assets, which may ultimately constrain future revenue growth as structural energy transitions gather pace.

- While delays in renewable energy infrastructure and concerns about grid reliability are temporarily supporting coal demand, rapid advancements in and cost declines for renewables are likely to reduce coal's competitiveness in electricity generation over time, compressing Peabody's addressable market and weakening long-term earnings visibility.

- Even as Peabody's efficiency measures and strong cost control are currently supporting robust EBITDA margins, the company's continued high exposure to U.S. thermal coal means it remains particularly vulnerable as domestic utilities increasingly commit to cleaner energy sources, leading to gradual declines in volumes and net margins.

- Despite a temporary tightening in global coal supply due to underinvestment and production disruptions, escalating regulatory scrutiny, carbon pricing, and investor activism in major markets raise the risk of higher operating costs, reduced financing flexibility, and persistent downward pressure on Peabody's valuation multiples.

- Although Peabody's diversification and capital discipline have strengthened its balance sheet, significant environmental remediation liabilities and the potential for unpredictable earnings due to commodity price volatility continue to increase the risk premium assigned to its stock and could cap future free cash flow growth.

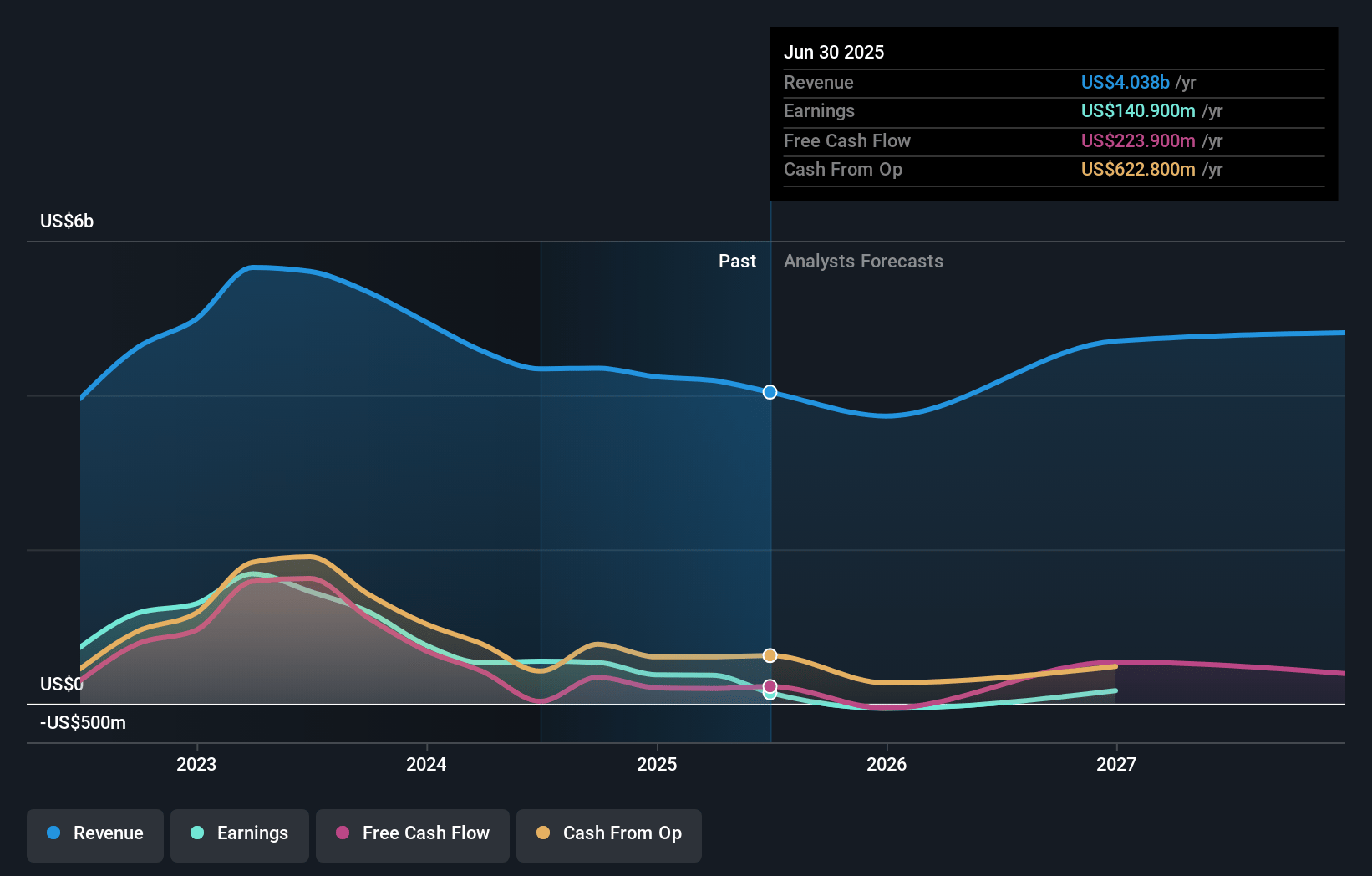

Peabody Energy Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more pessimistic perspective on Peabody Energy compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming Peabody Energy's revenue will grow by 2.3% annually over the next 3 years.

- The bearish analysts assume that profit margins will shrink from 8.8% today to 6.2% in 3 years time.

- The bearish analysts expect earnings to reach $280.5 million (and earnings per share of $2.34) by about July 2028, down from $369.1 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 7.5x on those 2028 earnings, up from 4.8x today. This future PE is lower than the current PE for the US Oil and Gas industry at 12.4x.

- Analysts expect the number of shares outstanding to decline by 3.42% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.6%, as per the Simply Wall St company report.

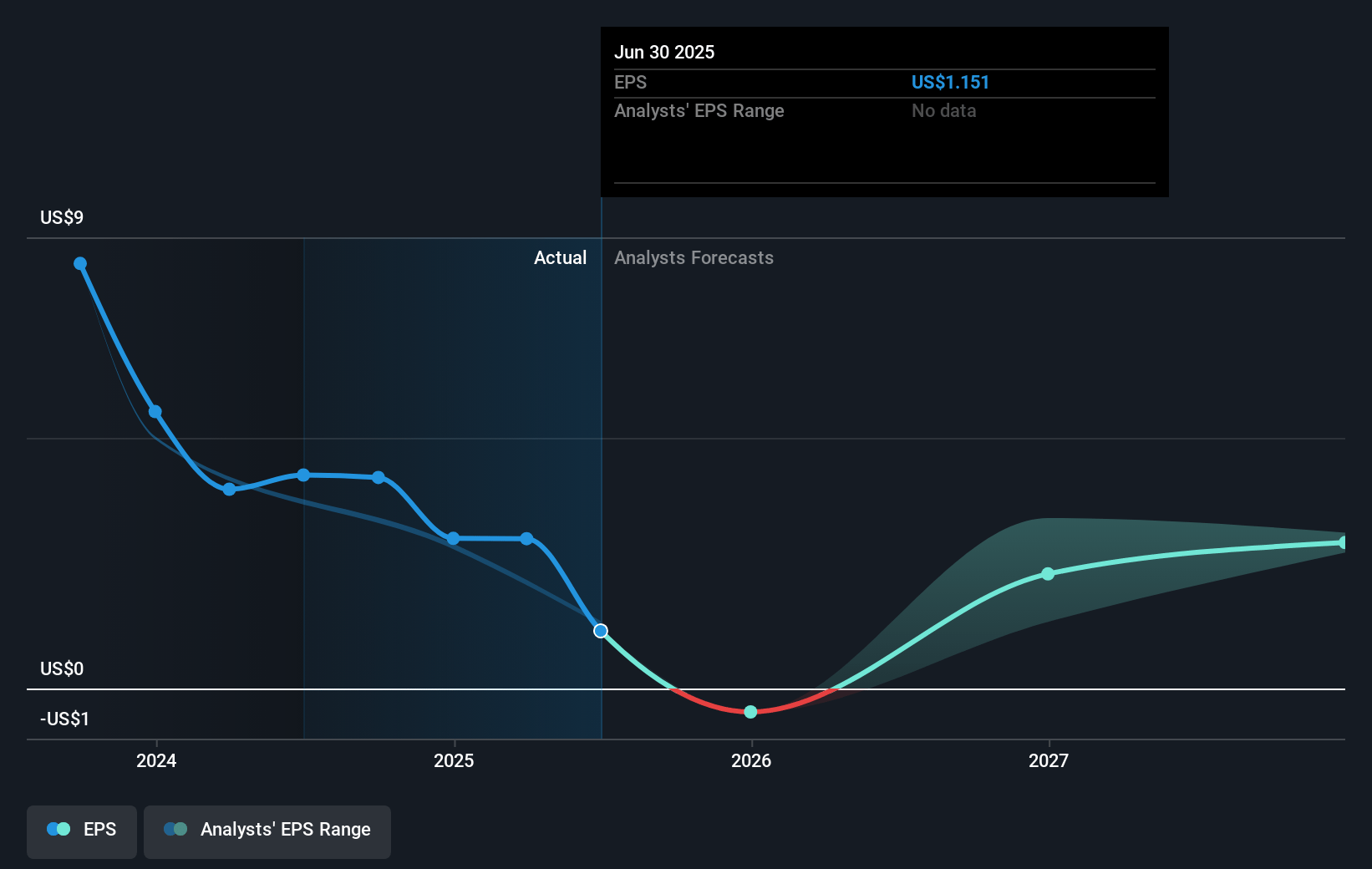

Peabody Energy Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Increased global decarbonization efforts and the advancement of climate policy in the U.S. and internationally could accelerate utility coal plant retirements over the coming decade, placing long-term pressure on Peabody Energy's core U.S. thermal coal revenue streams despite current policy support and recent agreements.

- The company's high exposure to volatile commodity prices and cyclical demand was highlighted by weak thermal and metallurgical coal pricing in the first quarter and cost increases anticipated in coming quarters, which could negatively impact earnings and margins during cyclical downturns.

- Delays, uncertainty, or potential termination of the Moranbah North mine acquisition, which was positioned as a high-margin growth driver, introduce material risk to Peabody's long-term expansion strategy and could hinder future revenue and margin growth in its metallurgical coal segment.

- Increasing regulatory scrutiny, such as the sweeping mine safety review in Queensland and environmental requirements for reclamation, could raise operating costs and lead to additional charges over time, reducing net margins and free cash flow.

- The long-term competitiveness of coal is threatened by steady improvements and falling costs in renewables, battery storage, and natural gas; as utilities continue to diversify or transition generation, Peabody may see further volume declines and contracting revenues in its major markets.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bearish price target for Peabody Energy is $16.0, which represents the lowest price target estimate amongst analysts. This valuation is based on what can be assumed as the expectations of Peabody Energy's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $23.0, and the most bearish reporting a price target of just $16.0.

- In order for you to agree with the bearish analysts, you'd need to believe that by 2028, revenues will be $4.5 billion, earnings will come to $280.5 million, and it would be trading on a PE ratio of 7.5x, assuming you use a discount rate of 6.6%.

- Given the current share price of $14.68, the bearish analyst price target of $16.0 is 8.3% higher. Despite analysts expecting the underlying buisness to decline, they seem to believe it's more valuable than what the market thinks.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.