Key Takeaways

- Strategic LPG sales agreements and efficient drilling practices enhance capital efficiency and improve net margins by reducing market volatility exposure.

- Wide natural gas collars and stock buyback programs offer revenue predictability and potentially boost EPS and shareholder returns.

- Overcapacity in the global gas market and potential volatility in LPG premiums could limit Antero Resources' pricing power and strategic growth, impacting revenues and earnings.

Catalysts

About Antero Resources- An independent oil and natural gas company, engages in the development, production, exploration, and acquisition of natural gas, natural gas liquids (NGLs), and oil properties in the United States.

- Antero Resources has achieved significant drilling and completion efficiencies, increasing completed feet per day by 15% and setting company records, which enhances capital efficiency and potentially boosts earnings.

- The company has locked in wide natural gas collars for 2026, which secure attractive returns with a floor price of $3.07 and a ceiling of $5.96, offering revenue predictability and safeguarding net margins.

- Antero's strategic LPG sales agreements secure premiums to Mont Belvieu prices, leveraging a strong geographic position for exports and reducing exposure to market volatility, thus potentially improving net margins.

- Increased demand for natural gas from startup LNG facilities and regional power plants is anticipated to lift gas pricing, positively impacting revenues and earnings.

- Antero's strategic share buyback program takes advantage of stock undervaluation, potentially enhancing EPS and shareholder returns over time.

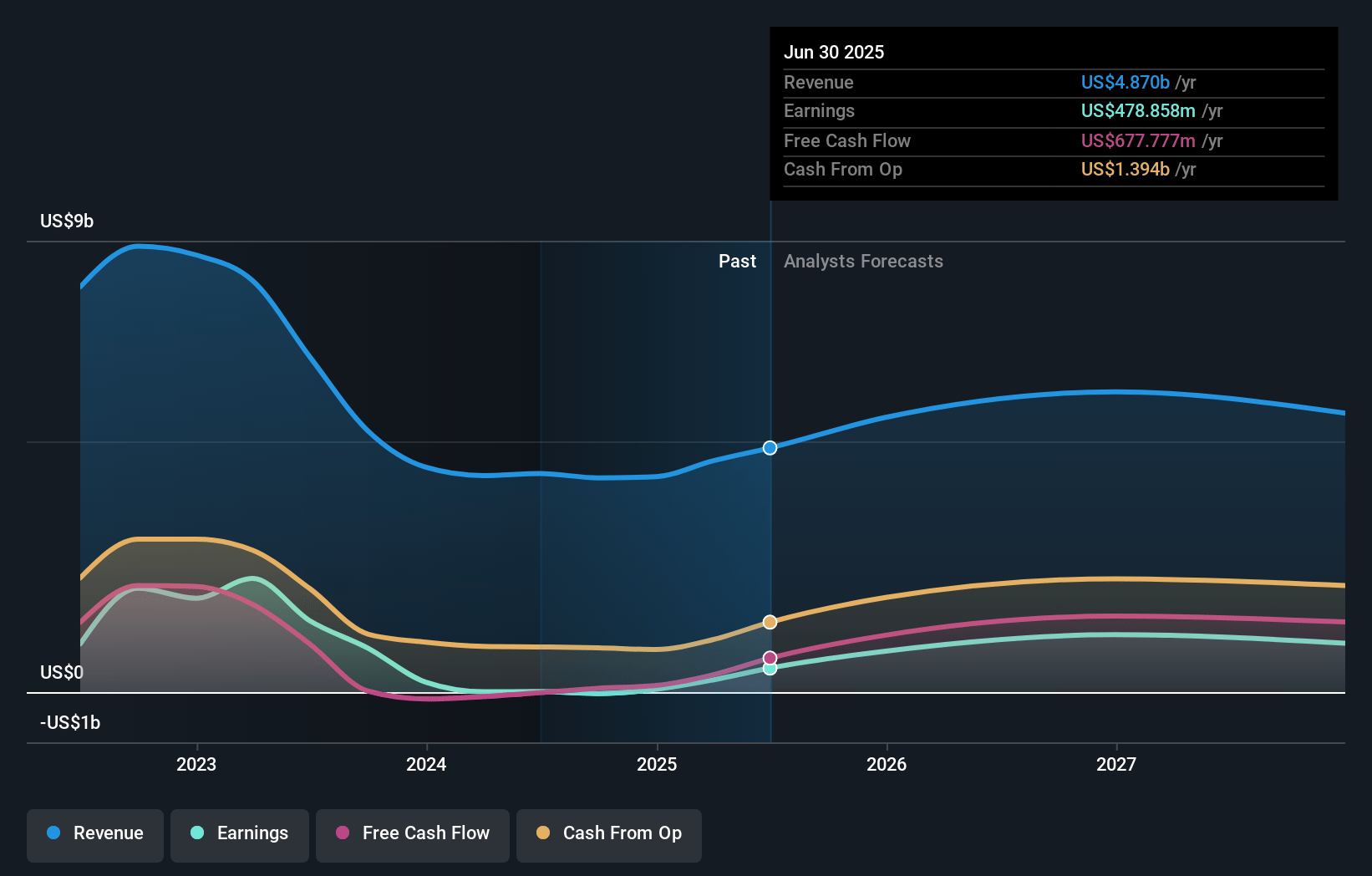

Antero Resources Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Antero Resources's revenue will grow by 11.4% annually over the next 3 years.

- Analysts assume that profit margins will increase from 5.3% today to 14.0% in 3 years time.

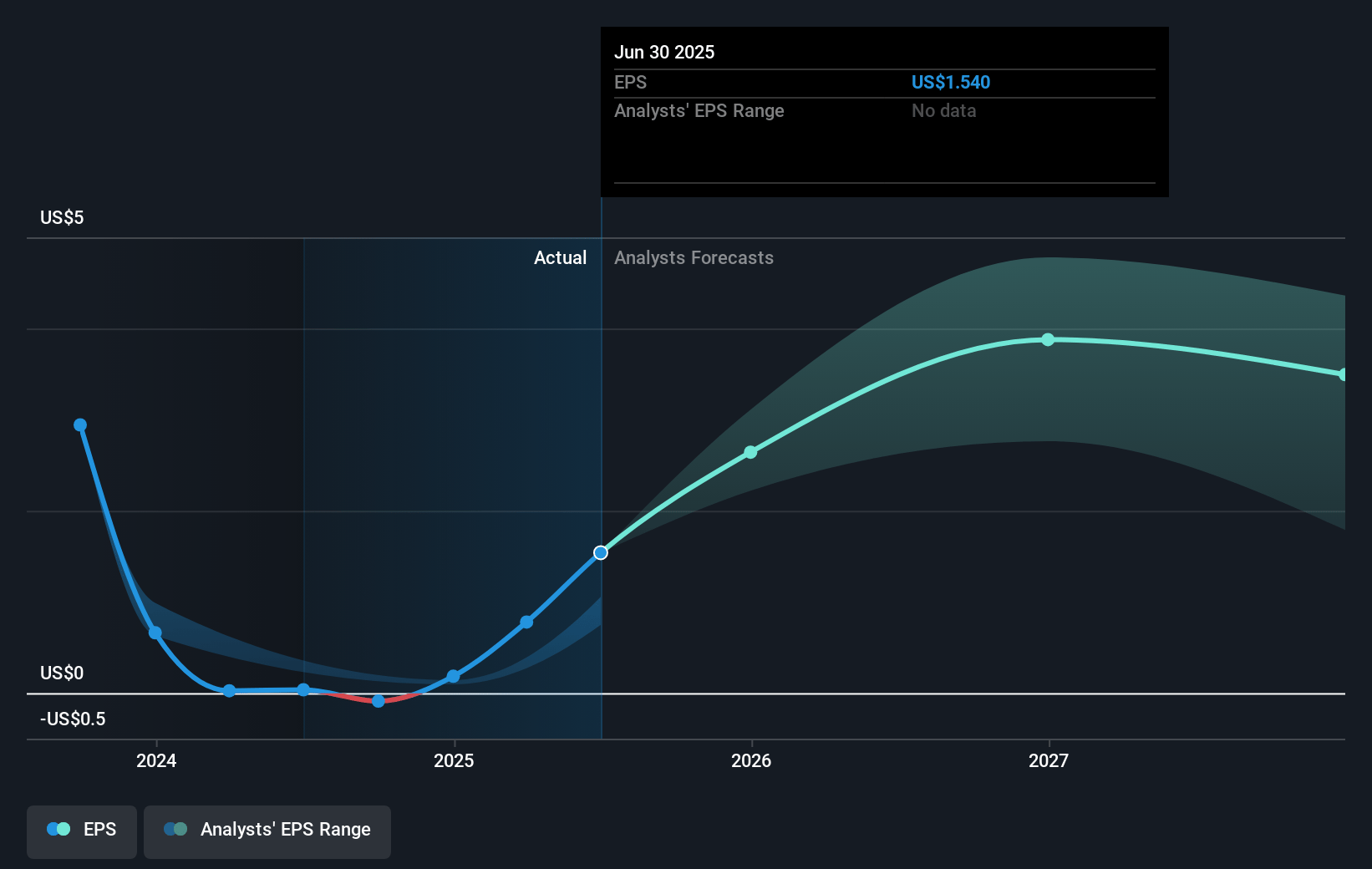

- Analysts expect earnings to reach $892.2 million (and earnings per share of $3.19) by about July 2028, up from $242.5 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $1.3 billion in earnings, and the most bearish expecting $509 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 19.1x on those 2028 earnings, down from 42.5x today. This future PE is greater than the current PE for the US Oil and Gas industry at 12.3x.

- Analysts expect the number of shares outstanding to decline by 0.15% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.82%, as per the Simply Wall St company report.

Antero Resources Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The global gas market could face overcapacity, which might limit price increases and overall revenue potential for Antero Resources.

- The potential volatility in LPG premiums could impact Antero's pricing power, especially if the current premium pricing environment weakens, thus affecting revenues.

- Limited room for debt reduction and heavier reliance on share buybacks may pressure Antero’s capital allocation, impacting earnings if market conditions worsen.

- In-basin demand considerations suggest that new local supply commitments could be constrained by pricing dynamics, which may limit strategic growth and impact future revenues.

- Questions about potential global oversupply might require U.S. gas pricing to align more closely with global hubs, potentially limiting marketable price gains and affecting Antero's net margins and earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $45.143 for Antero Resources based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $58.0, and the most bearish reporting a price target of just $22.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $6.4 billion, earnings will come to $892.2 million, and it would be trading on a PE ratio of 19.1x, assuming you use a discount rate of 6.8%.

- Given the current share price of $33.18, the analyst price target of $45.14 is 26.5% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.