Key Takeaways

- Structural shifts toward decarbonization and renewables threaten long-term demand for pipeline assets, putting sustained pressure on revenue growth and earnings stability.

- Operational concentration in the Permian Basin and intensifying regulatory challenges elevate both regional and compliance risks, constraining expansion and profitability.

- Strategic growth in core energy infrastructure, stable fee-based contracts, disciplined capital management, and industry consolidation all position the company for resilient and expanding profitability.

Catalysts

About Plains GP Holdings- Through its subsidiary, Plains All American Pipeline, L.P., owns and operates midstream infrastructure systems in the United States and Canada.

- Intensifying global decarbonization efforts and tightening climate policies threaten to decrease long-term demand for oil and gas, which could structurally reduce utilization of Plains GP Holdings' pipeline network, leading to declining volumes and significant pressure on revenue growth.

- Rapid adoption of electric vehicles and alternative fuels is set to erode transportation fuel consumption in key markets, diminishing the flow of crude oil through Plains' assets and further constraining top-line growth prospects.

- The company's heavy operational reliance on the Permian Basin exposes it to concentrated regional risks such as production declines, policy headwinds, or regulatory changes in Texas and New Mexico, which may materially impact both revenue generation and earnings stability.

- Mounting regulatory and permitting hurdles for new pipeline construction or expansions will likely restrict Plains' ability to develop new infrastructure, curtailing future growth opportunities while increasing compliance-driven capital expenditures and compressing net margins.

- The accelerating transition toward renewable energy and risk of stranded pipeline assets raise the likelihood of future asset impairments and write-downs, directly undermining profitability and ultimately threatening Plains GP Holdings' long-term earnings power.

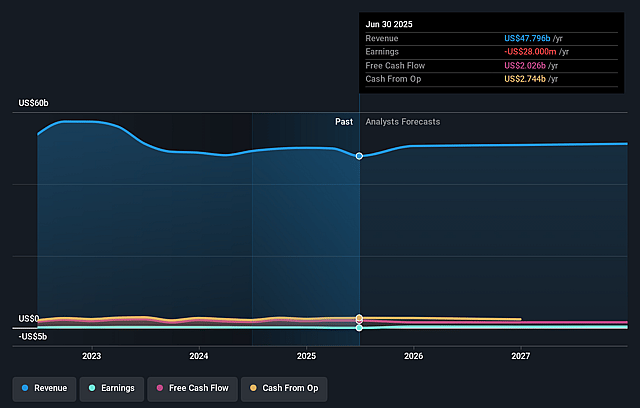

Plains GP Holdings Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more pessimistic perspective on Plains GP Holdings compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming Plains GP Holdings's revenue will decrease by 3.7% annually over the next 3 years.

- The bearish analysts assume that profit margins will increase from 0.3% today to 0.5% in 3 years time.

- The bearish analysts expect earnings to reach $225.6 million (and earnings per share of $1.14) by about July 2028, up from $145.0 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 23.6x on those 2028 earnings, down from 27.1x today. This future PE is greater than the current PE for the US Oil and Gas industry at 12.3x.

- Analysts expect the number of shares outstanding to grow by 0.24% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.17%, as per the Simply Wall St company report.

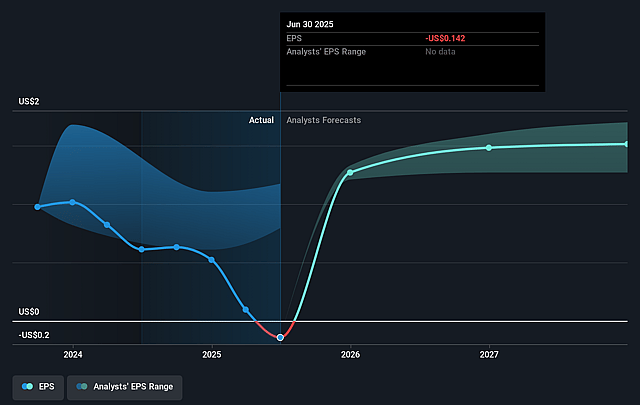

Plains GP Holdings Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Plains GP Holdings continues to expand and optimize its infrastructure in the Permian Basin-the fastest-growing crude oil producing region-and recent strategic acquisitions, especially in core Permian locations, are poised to enhance market share, throughput volumes, and revenue growth over the long term.

- The company is shifting an increasing proportion of its revenues to fee-based, long-term contracts and has implemented robust hedging on its NGL business, which together improve earnings stability and protect net margins from commodity price volatility.

- Management is committed to disciplined capital allocation, ongoing deleveraging, and maintaining a highly flexible balance sheet, which supports lower interest expenses, substantial free cash flow, and potential future dividend growth, thereby directly strengthening profitability and shareholder returns.

- The midstream sector continues to benefit from strong secular demand for energy commodities, due to global population growth, industrialization in emerging markets, and ongoing needs for secure, reliable energy transport infrastructure over the next decade, all of which are likely to support Plains GP Holdings' asset utilization, contract volumes, and core revenue streams.

- Consolidation opportunities and ongoing bolt-on M&A, facilitated by Plains' financial capacity and network integration, enable operational scale and cost synergies that can drive margin expansion and improved earnings resilience, especially as the company leverages its strong relationships and dominant network position.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bearish price target for Plains GP Holdings is $17.5, which represents the lowest price target estimate amongst analysts. This valuation is based on what can be assumed as the expectations of Plains GP Holdings's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $26.0, and the most bearish reporting a price target of just $17.5.

- In order for you to agree with the bearish analysts, you'd need to believe that by 2028, revenues will be $44.8 billion, earnings will come to $225.6 million, and it would be trading on a PE ratio of 23.6x, assuming you use a discount rate of 9.2%.

- Given the current share price of $19.85, the bearish analyst price target of $17.5 is 13.4% lower. Despite analysts expecting the underlying buisness to improve, they seem to believe the market's expectations are too high.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.