Key Takeaways

- Strategic cost reduction and asset sales aim to boost net margins through enhanced operational efficiency and market scalability.

- Expanding protein business and carbon platform monetization expected to drive significant revenue growth and unlock future earnings potential.

- Ongoing financial strain with net losses, impacted by operational challenges and market volatility, hinders profitability and delays in diversifying revenue streams.

Catalysts

About Green Plains- Produces low-carbon fuels in the United States and internationally.

- Green Plains is executing a significant cost reduction initiative, targeting $50 million in savings through the sale of nonstrategic assets and cost structure optimization, expected to enhance net margins.

- The company's ethanol production achieved 100% utilization in Q1 2025, the highest rate on record, and projects continued high utilization rates, which are anticipated to improve operational efficiency and earnings.

- The Eco-Energy marketing partnership is anticipated to deliver transportation and logistics efficiencies, strengthening revenue streams through enhanced market access and scalability.

- Green Plains is expanding its protein business, with volume growth expected from 20,000 tons in 2024 to over 80,000 tons in 2025, projected to significantly contribute to revenue growth, and further expansion into high-margin sectors like pet food is expected by 2026.

- The ongoing construction and monetization of the carbon platform, including the Advantage Nebraska initiative, is set to unlock new revenue streams and potential value creation from carbon credits, thereby enhancing future earnings potential.

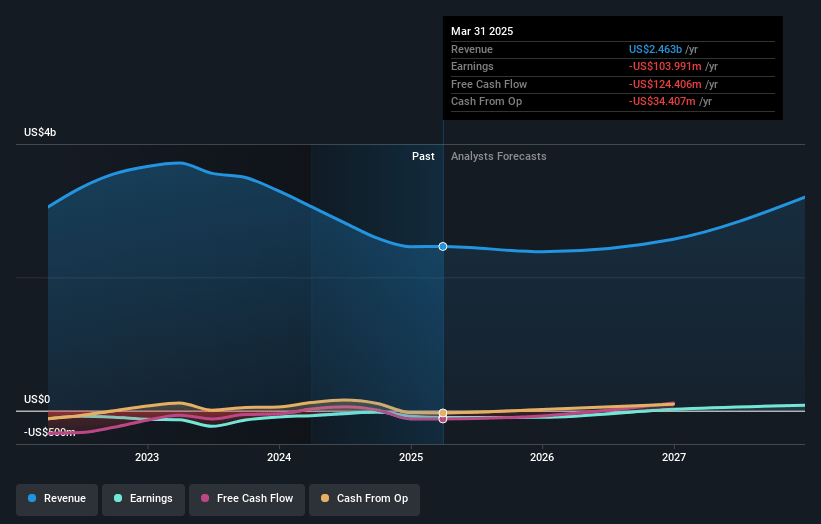

Green Plains Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Green Plains's revenue will grow by 10.3% annually over the next 3 years.

- Analysts assume that profit margins will increase from -4.2% today to 3.5% in 3 years time.

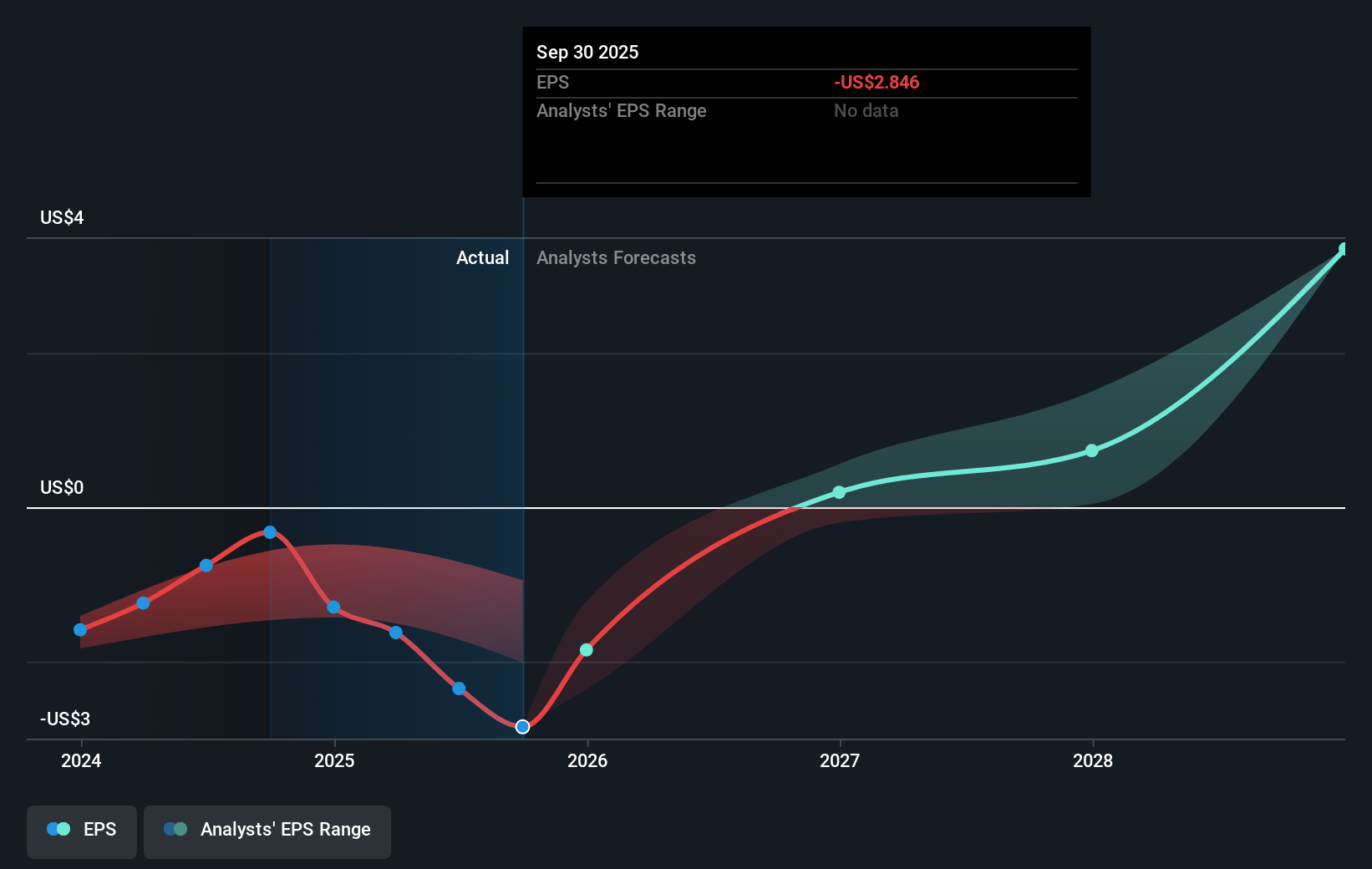

- Analysts expect earnings to reach $117.1 million (and earnings per share of $3.89) by about July 2028, up from $-104.0 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 6.2x on those 2028 earnings, up from -5.0x today. This future PE is lower than the current PE for the US Oil and Gas industry at 12.3x.

- Analysts expect the number of shares outstanding to grow by 1.15% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.07%, as per the Simply Wall St company report.

Green Plains Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The company's performance has not met expectations, and it is working to return to sustained profitability, which indicates that its current financial situation, particularly earnings, is not stable.

- The reported net loss of $72.9 million for the first quarter of 2025, and the consistent losses from previous years, imply continued financial strain impacting net margins and overall profitability.

- Operational challenges, such as wastewater issues affecting the Clean Sugar Technology initiative, indicate potential delays in diversifying revenue streams and improving profit margins.

- The ethanol market faced seasonal weakness, reflecting an overproduction and high inventory levels, which may impede efforts to stabilize or increase revenues from this segment.

- The reliance on securing hedges and margin management due to market volatility underscores the risk of fluctuating earnings and the reliance on external factors to maintain financial stability.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $8.625 for Green Plains based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $25.0, and the most bearish reporting a price target of just $4.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $3.3 billion, earnings will come to $117.1 million, and it would be trading on a PE ratio of 6.2x, assuming you use a discount rate of 8.1%.

- Given the current share price of $7.89, the analyst price target of $8.62 is 8.5% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.