Key Takeaways

- Strategic investments in digital marketing and sales infrastructure, along with new product offerings, are anticipated to drive future revenue growth.

- Focus on AI, automation, and acquisitions, alongside share repurchases, is likely to improve efficiency, security, and earnings per share.

- Declining sales, operational inefficiencies, client transitions, contract delays, and macroeconomic sensitivities are negatively impacting WEX's revenue, earnings, and profit margins.

Catalysts

About WEX- Operates a commerce platform in the United States and internationally.

- WEX's strategic investments in digital marketing and sales infrastructure are expected to enhance the company's ability to generate new business, which should contribute to future revenue growth.

- The launch of new product offerings, such as the 10-4 by WEX app and initiatives in electric vehicle (EV) solutions, are anticipated to expand WEX’s market reach and increase customer spending, potentially impacting future revenue positively.

- The acquisition of Payzer is expected to contribute to revenue growth in the Mobility segment by tapping into adjacent markets and driving cross-selling opportunities.

- Continued focus on AI and automation in operations is likely to enhance efficiency and security, potentially leading to higher net margins in the future.

- Increased share repurchases, supported by a $1 billion authorization from the Board, are expected to drive enhanced earnings per share (EPS) through a reduced share count.

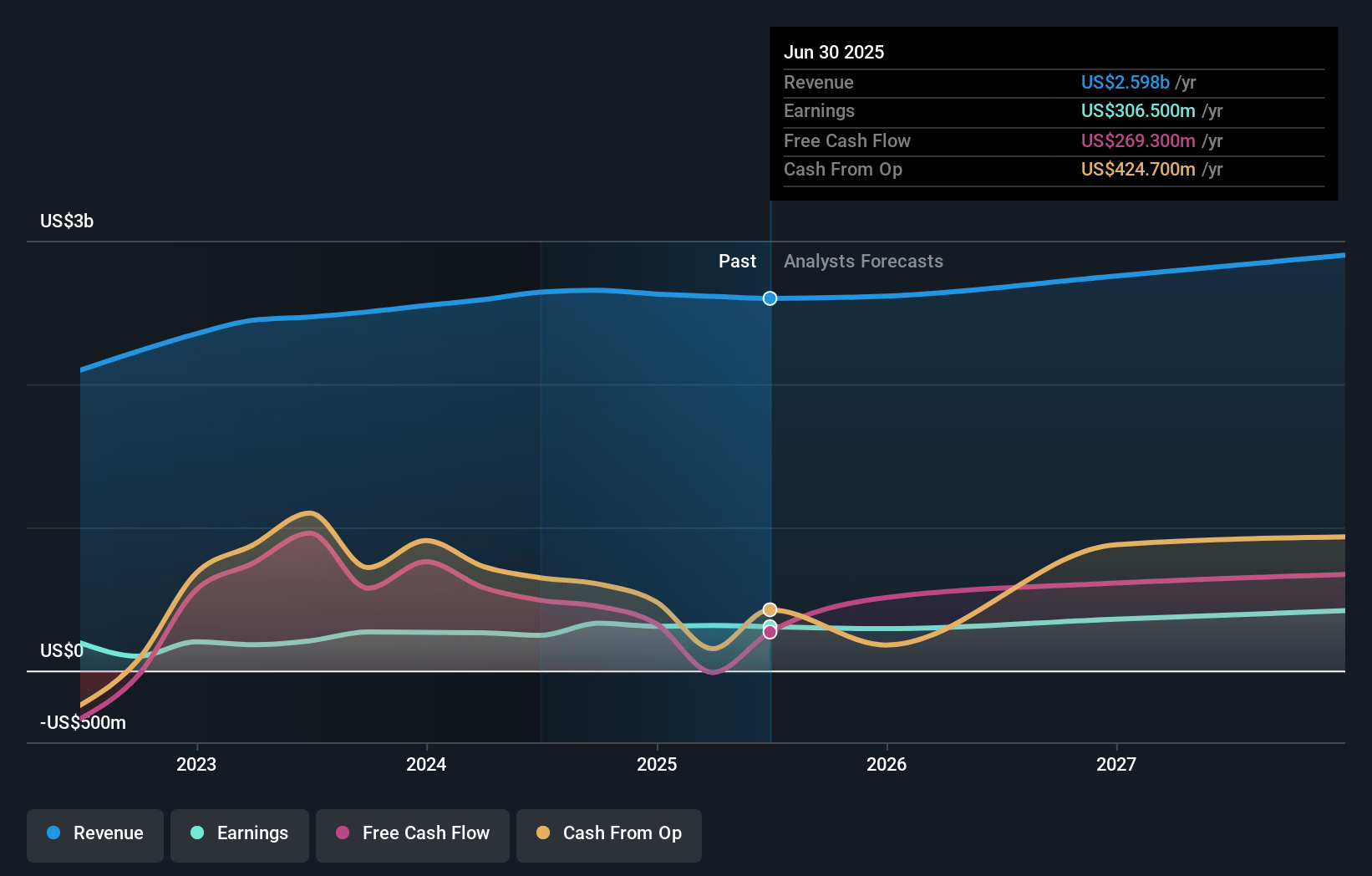

WEX Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming WEX's revenue will grow by 4.4% annually over the next 3 years.

- Analysts assume that profit margins will increase from 12.5% today to 18.8% in 3 years time.

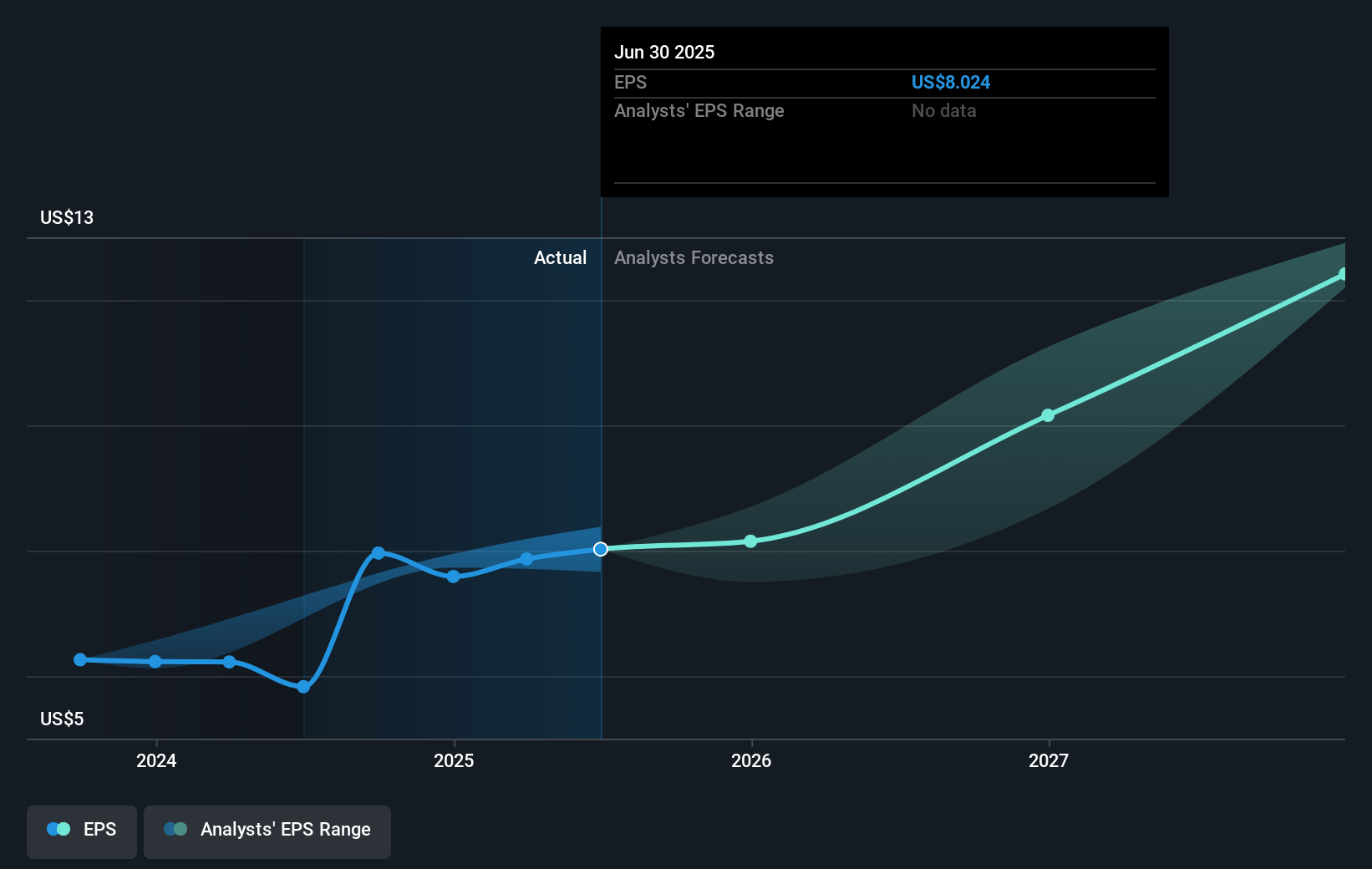

- Analysts expect earnings to reach $569.9 million (and earnings per share of $14.11) by about January 2028, up from $330.6 million today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as $428 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 17.5x on those 2028 earnings, down from 21.8x today. This future PE is lower than the current PE for the US Diversified Financial industry at 18.5x.

- Analysts expect the number of shares outstanding to grow by 0.51% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.99%, as per the Simply Wall St company report.

WEX Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Declining fuel prices and softness in same-store sales have impacted the Mobility segment, leading to lowered revenue and earnings guidance for the remainder of 2024. This may continue to affect revenue and profit margins if the trend persists.

- Isolated operational issues in optimizing the pricing structure have led to unplanned charges, impacting short-term earnings negatively and indicating potential inefficiencies in cost management and pricing strategies.

- The transition of a large online travel agency customer to a new payment model is causing short-term revenue reductions in the Corporate Payments segment, reflecting a potential vulnerability to significant client transitions which could impact overall revenue.

- Delays in new contract implementations in the Benefits segment have deferred expected revenue, pointing to challenges in capturing projected earnings momentum and impacting revenue growth forecasts.

- Lower interest rates are expected to reduce fourth-quarter revenue, showcasing the company's sensitivity to macroeconomic conditions which could impact profitability, despite hedging strategies that offset the impact on overall earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $198.01 for WEX based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $220.0, and the most bearish reporting a price target of just $170.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $3.0 billion, earnings will come to $569.9 million, and it would be trading on a PE ratio of 17.5x, assuming you use a discount rate of 8.0%.

- Given the current share price of $181.5, the analyst's price target of $198.01 is 8.3% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives