Narratives are currently in beta

Key Takeaways

- Expansion in refinance and purchase segments and leveraging AI technology are aimed at driving revenue growth and improving operational efficiency.

- Targeting diverse demographics and launching innovative mortgage products position Rocket Companies for long-term success in evolving market segments.

- Unpredictable interest rates and housing affordability could challenge Rocket Companies' revenue growth amid reliance on home equity and execution risks in technological investments.

Catalysts

About Rocket Companies- A fintech holding company, provides mortgage lending, title and settlement services, and other financial technology services in the United States and Canada.

- Rocket Companies is focused on expanding its market share in both the purchase and refinance segments, targeting a doubling of its purchase market share and a significant increase in refinance market share by 2027. This is expected to drive future revenue growth.

- The company has a strategic partnership with Annaly for subservicing, allowing it to expand its servicing portfolio capital-efficiently, which could improve net margins by reducing client acquisition costs through high client recapture rates.

- Rocket Companies is leveraging its AI-driven technology, such as its Navigator platform and Rocket Logic, to enhance operational efficiency, aiming to reduce costs and boost earnings by increasing team member productivity without adding fixed costs.

- The introduction of innovative mortgage products, like the Welcome Home Rate Break, is intended to enhance affordability for clients, potentially increasing loan origination volumes and thus revenues as market conditions become more favorable.

- A strong brand and a focus on target growth demographics such as female heads of households, Hispanics, and aging first-time buyers position Rocket Companies for long-term revenue growth by capturing evolving segments of the homebuying market.

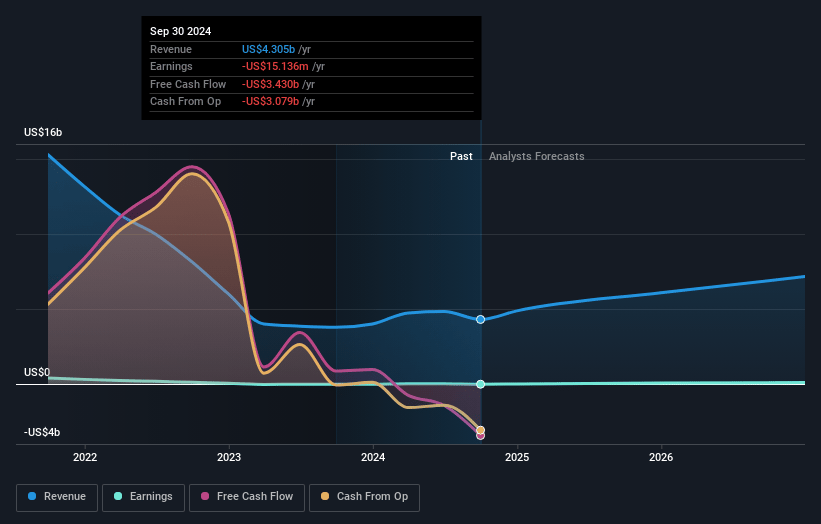

Rocket Companies Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Rocket Companies's revenue will grow by 24.9% annually over the next 3 years.

- Analysts assume that profit margins will increase from -0.4% today to 1.5% in 3 years time.

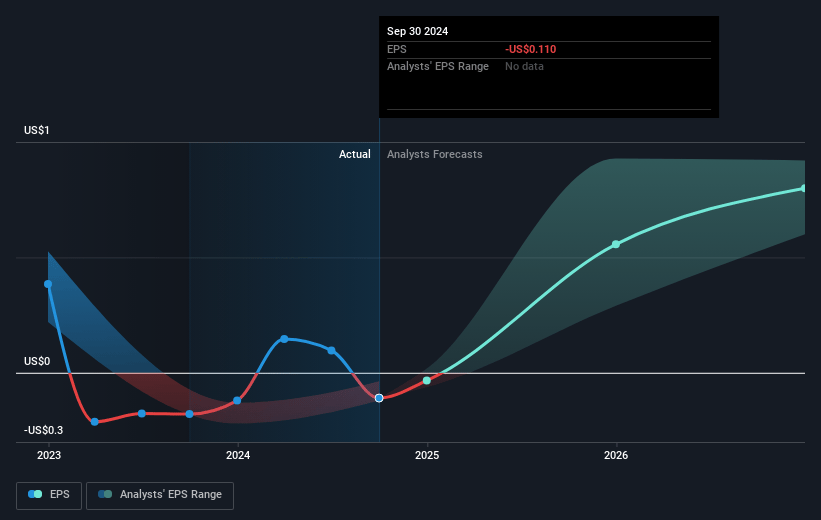

- Analysts expect earnings to reach $127.1 million (and earnings per share of $0.97) by about January 2028, up from $-15.1 million today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as $78.3 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 16.7x on those 2028 earnings, up from -125.4x today. This future PE is lower than the current PE for the US Diversified Financial industry at 18.5x.

- Analysts expect the number of shares outstanding to decline by 59.6% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.07%, as per the Simply Wall St company report.

Rocket Companies Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Despite the optimism around the mortgage market, the unpredictability of interest rates and their decoupling from Federal rate changes could impact Rocket Companies' revenue if rates remain high or increase, affecting consumer demand.

- The company faces affordability challenges in the housing market, which could hinder its ability to increase purchase and refinance market shares, thereby affecting its revenue growth.

- Dependent on the home equity market for growth, Rocket Companies could face stagnation if interest rates dissuade homeowners from second lien products or refinancing, impacting revenue streams.

- The potential for pricing pressures, particularly around the holidays, could impact the company's gain on sale margins and profitability, as hinted at by expected slight expansion influenced by competitive dynamics.

- While the company highlights technological investments and AI to drive efficiency, reliance on these innovations in a volatile market environment introduces execution risks that could affect operating margins and earnings if not realized as expected.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $13.21 for Rocket Companies based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $18.0, and the most bearish reporting a price target of just $10.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $8.4 billion, earnings will come to $127.1 million, and it would be trading on a PE ratio of 16.7x, assuming you use a discount rate of 7.1%.

- Given the current share price of $13.02, the analyst's price target of $13.21 is 1.5% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives