Narratives are currently in beta

Key Takeaways

- Strategic acquisitions and partnerships aim to enhance revenue, market reach, and sustainable growth through improved loan pricing and product offerings.

- Technology advancements and customer-focused tools are set to increase user engagement, retention, and financial stability, boosting long-term value.

- Acquiring a large loan portfolio may enhance earnings but strain liquidity, impacting LendingClub's capacity for new investments and margin maintenance.

Catalysts

About LendingClub- Operates as a bank holding company, that provides range of financial products and services in the United States.

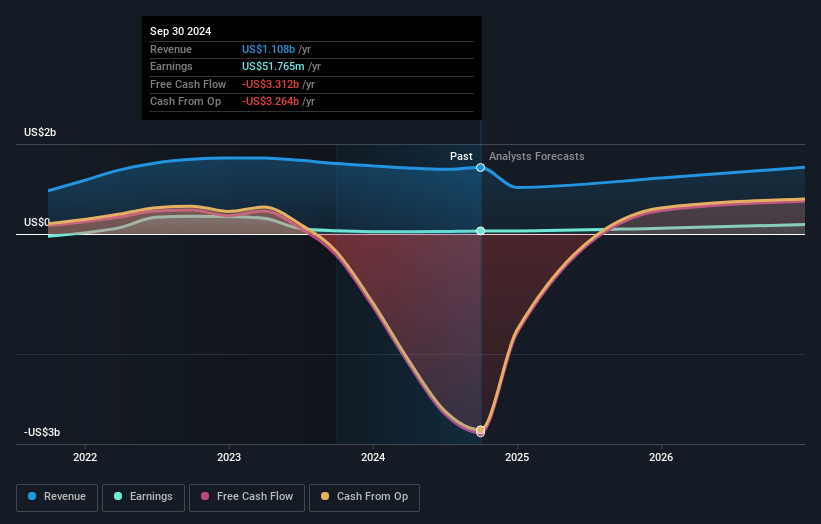

- LendingClub's acquisition of a $1.3 billion portfolio of previously sold loans is expected to be immediately accretive to earnings, highlighting strategic growth in their balance sheet that could boost future recurring revenue streams.

- The partnership with banks to purchase over $1 billion worth of loans in the next 12 months is anticipated to enhance loan sale pricing, which will potentially grow revenue and enable the reopening of marketing channels that were previously uneconomic.

- The acquisition of Tally's technology to bolster their credit card management solution is set to accelerate LendingClub's product roadmap, offering higher user engagement and potentially increasing cross-selling opportunities, thus impacting future revenue growth positively.

- The development and rollout of customer-centric tools like the app and DebtIQ are designed to drive deeper consumer engagement and retention, which may translate into increased lifetime value from their member base, positively impacting long-term earnings and margins.

- The recent launch of LevelUp Savings to incentivize saving behavior reflects a strategic method to manage deposit costs while offering competitive value to members, suggesting potential positive effects on LendingClub’s net interest margin and revenue stability.

LendingClub Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming LendingClub's revenue will decrease by 0.6% annually over the next 3 years.

- Analysts assume that profit margins will increase from 4.7% today to 19.0% in 3 years time.

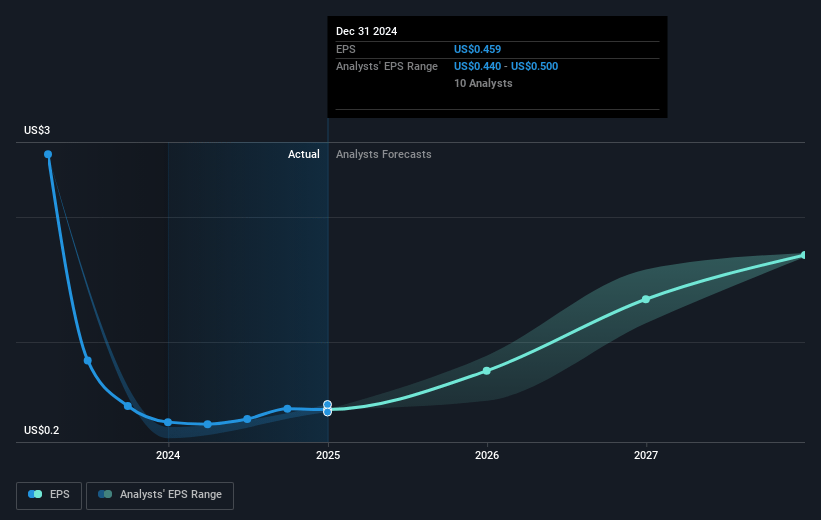

- Analysts expect earnings to reach $214.6 million (and earnings per share of $1.8) by about January 2028, up from $51.8 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 12.6x on those 2028 earnings, down from 35.4x today. This future PE is greater than the current PE for the US Consumer Finance industry at 11.6x.

- Analysts expect the number of shares outstanding to grow by 1.94% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.8%, as per the Simply Wall St company report.

LendingClub Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The acquisition of a $1.3 billion portfolio of previously sold loans, while immediately accretive to earnings, might strain future liquidity and capital allocation, impacting LendingClub's ability to invest in new originations and maintain net margins.

- Retaining a high percentage of originations on the balance sheet could limit short-term profitability due to upfront provisioning requirements under CECL (Current Expected Credit Loss), potentially affecting earnings.

- Increased operating expenses driven by recent technology investments and hiring could pressure net margins if such investments fail to yield expected returns and efficiencies.

- Dependency on favorable interest rate environments to stimulate growth in bank participation and loan sales pricing introduces a macroeconomic risk; adverse rate changes could hinder revenue expansion.

- The potential challenge of competition from irrational players in the loan market, particularly in the near-prime and high-prime segments, might compress margins, impact pricing strategy, and consequently affect revenue and earnings stability.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $18.65 for LendingClub based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $28.0, and the most bearish reporting a price target of just $11.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $1.1 billion, earnings will come to $214.6 million, and it would be trading on a PE ratio of 12.6x, assuming you use a discount rate of 6.8%.

- Given the current share price of $16.29, the analyst's price target of $18.65 is 12.7% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives