Narratives are currently in beta

Key Takeaways

- Launching new ETFs and focusing on global expansion could drive revenue and AUM growth through diversified offerings and increased inflows.

- Investments in infrastructure and diversification into private real estate signal a strategic emphasis on organic growth and enhanced future earnings.

- Rising expenses and declining AUM, coupled with competitive pressures and strategic reallocations, pose risks to revenue growth and net margins.

Catalysts

About Cohen & Steers- A publicly owned asset management holding company.

- Cohen & Steers plans to launch three new ETFs in Q1 of 2025, focusing on the wealth management channel, potentially leading to new revenue streams and growth in AUM as these products gain traction. (Revenue, AUM)

- The firm is seeing increased interest and activity in listed real assets due to favorable macro conditions and attractive valuations, indicating potential for growth in asset allocation and revenue from these asset classes. (Revenue, AUM)

- Diversification into private real estate and nontraded REITs, alongside a strong initial performance, suggests potential for expanding their real estate franchise, positively impacting future earnings and AUM. (Earnings, AUM)

- Expansion of international offices and strategic focus on growing presence outside the U.S., particularly in regions like Singapore and Japan, could increase global client base and boost future inflows. (Revenue, AUM)

- Continued investment in infrastructure, technology, marketing, and expanding sales and distribution resources indicates a strategic push for organic growth, expected to improve operating margins and enhance net earnings over time. (Operating margins, Earnings)

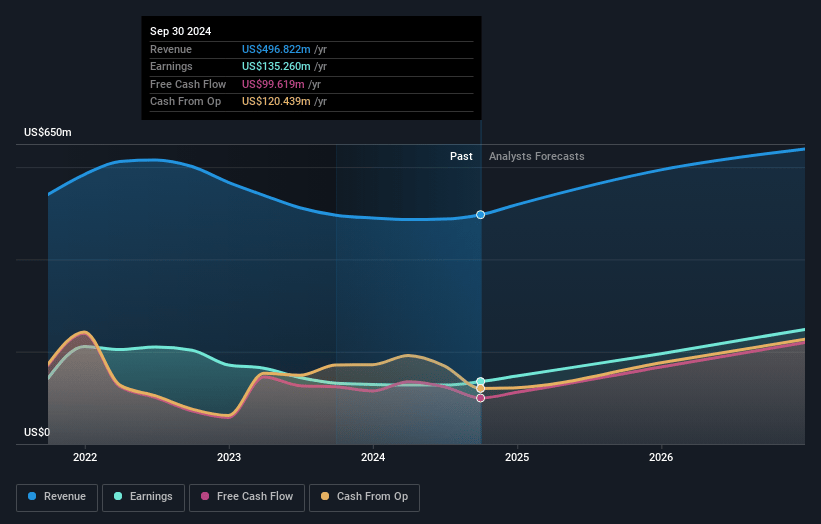

Cohen & Steers Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Cohen & Steers's revenue will grow by 9.4% annually over the next 3 years.

- Analysts assume that profit margins will increase from 29.2% today to 49.3% in 3 years time.

- Analysts expect earnings to reach $333.6 million (and earnings per share of $6.67) by about January 2028, up from $151.3 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 17.1x on those 2028 earnings, down from 30.1x today. This future PE is lower than the current PE for the US Capital Markets industry at 23.1x.

- Analysts expect the number of shares outstanding to decline by 0.36% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.86%, as per the Simply Wall St company report.

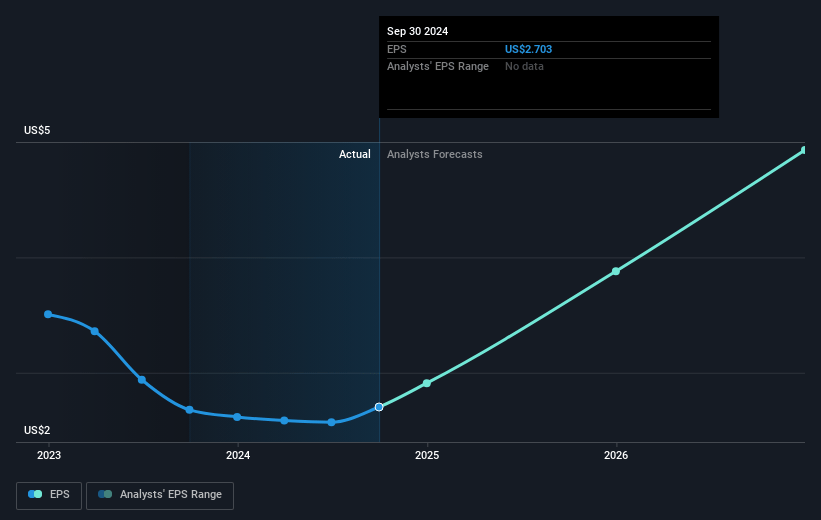

Cohen & Steers Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The increase in operating expenses, particularly due to rising compensation, benefits, distribution fees, and G&A expenses, could outpace revenue growth, impacting net margins and earnings.

- The decline in AUM from $91.8 billion in Q3 to $85.8 billion by year-end due to market depreciation poses a risk to revenue generation as it directly affects fee-based income.

- The competitive pressure and increased availability of private credit options could limit inflows into preferred securities, which could negatively affect revenue from this segment.

- The guidance of $800 million in expected redemptions in the first half of 2025 due to reallocations to private investments and client rebalancing could further reduce AUM, impacting future revenues.

- Initial foray into active ETFs, while potentially a growth area, is a new endeavor for the firm and carries execution risks that may affect projected revenues and market share.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $93.33 for Cohen & Steers based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $677.2 million, earnings will come to $333.6 million, and it would be trading on a PE ratio of 17.1x, assuming you use a discount rate of 6.9%.

- Given the current share price of $90.11, the analyst's price target of $93.33 is 3.5% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives