Narratives are currently in beta

Announcement on 23 September, 2024

Cost Cutting and Buybacks Offset Sluggish Sales Growth

PayPal’s Q2 results reflected the same trends that have played out for several quarters:

- Revenue increased 8.2% over the last year, which was a slight slowdown compared to recent quarters. This revenue growth was on the back of an 11% increase in transaction volumes.

- Take rates remain under pressure, though the decline has slowed slightly.

- The biggest contribution to the net income and EPS was once again cost-cutting and share buybacks.

At the moment, revenue growth is well below my projection, while EPS growth is higher. I expect this to reverse as new initiatives drive revenue growth, while cost-cutting and share buybacks are somewhat temporary.

Once again, I’m more concerned with the long-term strategy than current performance, and there have been several positive developments in the last few months:

On 5th September; the company announced PayPal Everywhere. This is an omnichannel payment solution that allows customers to make payments with a debit card, or with their phone - via tap-to-pay or QR code. The solution also offers a range of rewards and cash-back plans.

PayPal’s strategy has come a long way since Alex Chriss became CEO 12 months ago. In January, the company announced new AI-powered tools to help customers make offers and recommendations to customers. More recently, an advertising program was announced that will use customer purchase data to help merchants target ads to customers.

These are the types of initiatives PayPal needs to regain its position. I think PayPal Everywhere will make it very competitive compared to banks, but it will continue to face stiff competition from mobile phone solutions like Apple Pay.

I still believe that transaction fees will continue to fall across the industry, and PayPal will need to find other ways to generate revenue. This is where ‘other merchant services’ is the key catalyst. In particular, advertising could become a game changer for PayPal. Amazon now earns ~$50 billion a year from advertising, and PayPal’s data puts it in a unique position to build an ad business.

These initiatives are all positive, but will still depend on executions and traction. I think it’s too early to build these catalysts into my valuation - but I will be watching their progress carefully. With regard to the immediate future, PayPal’s results are tracking my narrative and I’m going to maintain my assumptions and fair value estimate.

Key Takeaways

- Payments industry is likely going to become increasingly competitive.

- PYPL's margin trouble will likely persist - too many competing firms + high incentive to offer lower fees.

- TPV should increase at 25% annually, but operating margin will fall to 9% (fee pressure and rising costs)

- EPS growth falling into the single digits and the price multiple will remain below 18-20x.

Catalysts

Industry Catalysts

Competition will compress margins for everyone

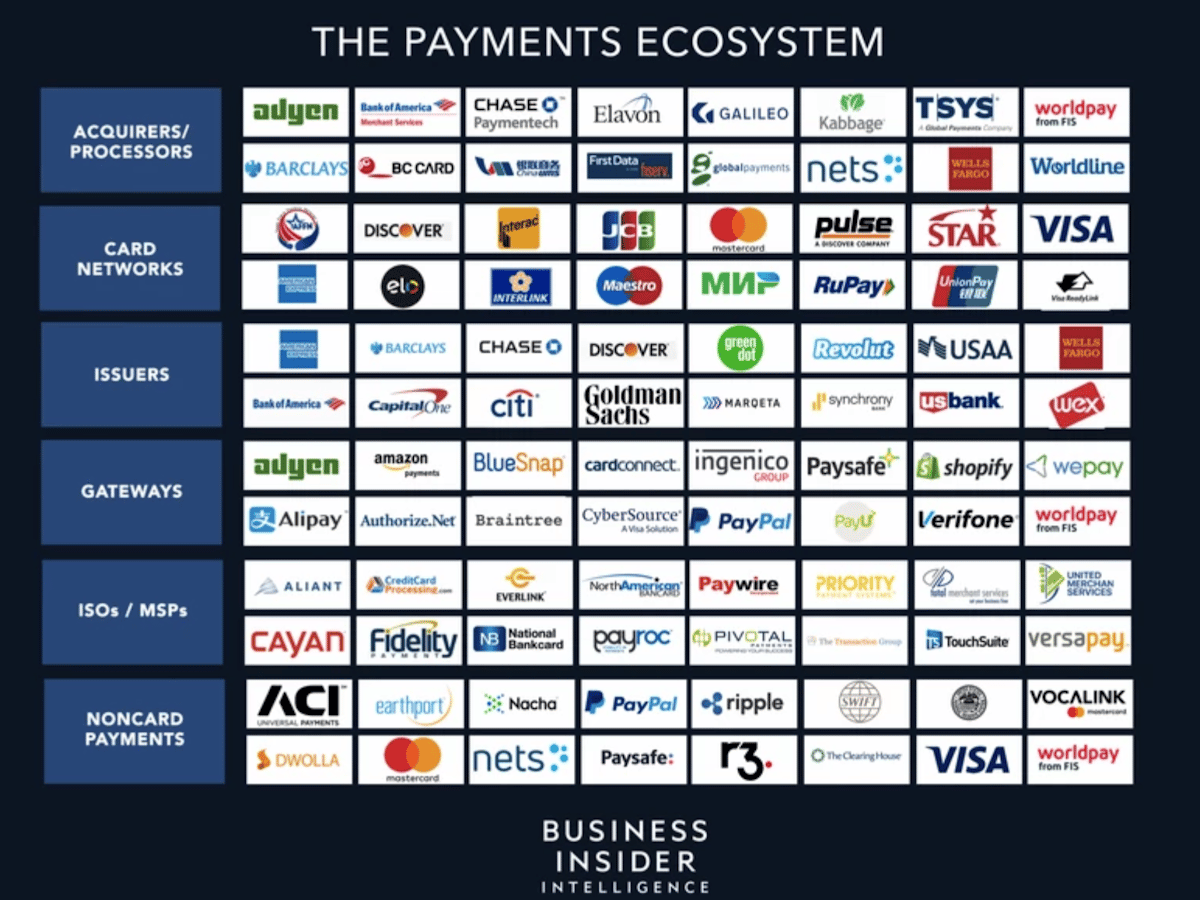

In recent years, the payments industry has become extremely crowded. There are also lots of different types of companies competing for varying slices of the fees charged to businesses and consumers.

Source: Business Insider

Prominent examples include:

- Payment platforms and wallets: PayPal, Block (Square and Cash App), Payoneer, Skrill.

- Cross border services: Wise, Western Union

- Ecommerce backend providers: Stripe, Adyen, Shopify/Shop Pay, Amazon

- Payment Networks: Visa, Mastercard, Amex

- Big tech: Apple Pay, Google Pay, Samsung Pay

- Regional solutions: Alipay, WeChat Pay, UnionPay, RuPayI, Mercado Pago, Rapyd, M-Pesa

- Banks: JP Morgan, HSBC, etc

- Neobanks: Nubank, Atom, Revolut.

- Other: Crypto platforms, mobile wallets etc

I believe the industry will become increasingly competitive and fees will continue to fall. I think fees across the entire industry are still much higher than they could be, particularly the fees charged to merchants.

As markets become more saturated, I think platforms are going to need to become more aggressive with their pricing. In addition, I think banks will be forced to enter this battle to remain relevant. I see the payment industry following a similar path to ride hailing, food delivery and classifieds publications - ie, going all out to win market share regardless of the cost.

In addition companies like Shopify can bundle payment services with other services to increase its overall value proposition. These platforms can focus on their overall margin rather than the margin from payment services.

The market seems to be expecting PayPal’s margins to improve after a temporary contraction. In fact, the company’s margins have been deteriorating steadily for the last ten years.

These are the change between 2013 and 2022:

- Revenue/TPV: 3.6% to 2%

- Gross profit/TPV: 1.86% to 0.86%

- Operating profit/TPV: 0.59% to 0.3%

- Net Profit/TPV: 0.52% to 0.18%

(TPV = total payment volume)

The bulk of this margin contraction can be attributed to the loss of eBay as a client. But I believe PayPal’s margins will likely remain under pressure due to the intense competition in the industry.

I believe all this competition will keep PayPal’s margins under pressure for a long time.

Source: CB Insights

Tailwinds will Continue to Drive Global Payment Volumes

I do think current tailwinds (ecommerce and the move toward a cashless society) will keep digital payment volumes growing at a healthy rate. I believe PayPal will allow its margins to be squeezed rather than lose market share, and so I think it will be able to keep payment volumes growing at around 25% annually.

Company Catalysts

The Product Mix Also Points to Margin Pressure

PayPal made two great acquisitions: Venmo and Braintree.

Braintree, the unbranded checkout option, is probably PayPal’s most important asset apart from the core checkout service. It’s also growing payment volumes faster than the core business. TPV growth for Braintree has been 40% a year over the last four years, compared to 25% for the company as a whole.

In 2022 Braintree accounted for 30% of the company’s transaction volume. Now that Braintree is becoming a larger part of the pie, its margins are increasingly important. This service competes directly with Adyen and Stripe, and doesn’t come with the brand equity of the PayPal button. I believe margins will inevitably be squeezed for this segment.

Venmo, PayPal’s peer to peer payment app is also growing payment volumes quickly. TPV increased by 55% a year in the three years to 2021, before slipping 7% in 2022. It now accounts for 18% of total TPV.

Source: Batch Processing

Venmo only charges a fee for instant payments, but it appears that most users don’t use this option, hence Venmo’s take rate of 0.38% is well below the overall rate of 2.02%. In addition, the recent introduction of government run instant payment systems like FedNow in the US and UPI in India could put the fees Venmo has been able to charge at risk.

PayPal has been reluctant to share the operational data for the individual segments and I think this is the reason. I think detailed data would paint a bleak picture on where margins are heading.

PayPal has had mixed success with other acquisitions like Hyperwallet, Zettle, and Xoom. Regardless, I think these are still too small to have a meaningful impact on the outlook.

Paypal Lacking Innovation and Strategy

PayPal’s past success can in large part be attributed to its symbiotic relationship with eBay, and great acquisitions in the form of Venmo and Braintree. When it was part of eBay, PayPal’s brand became well known and trusted as consumers became used to ecommerce. This made the ‘pay with PayPal’ button valuable to merchants and helped them increase sales. It also created a network effect for PayPal driving account growth and merchant adoption.

But that’s all in the past, and I don’t believe PayPal’s brand is nearly as valuable as it used to be. Consumers are more comfortable with ecommerce, and competing payment options like Skrill and Payoneer are now well known. Apple and Google have also entered the space with their already well known brands and customers.

I think PayPal has been resting on its laurels, relying on its brand and the acquisitions which also lessened the effect of losing eBay. But the company hasn’t been an innovation leader, while many of its competitors have. It seems to me that the company is now following industry trends with services like BNPL (buy now pay later), crypto, and merchant services, rather than leading the way.

Dan Schulman, PayPal’s CEO is leaving at the end of the year, and a successor has yet to be named. I think the company’s strategy will be in limbo until a new CEO is in place and a new strategy announced.

Assumptions

Payment Volumes will Keep Growing, but the Take Rate will Fall

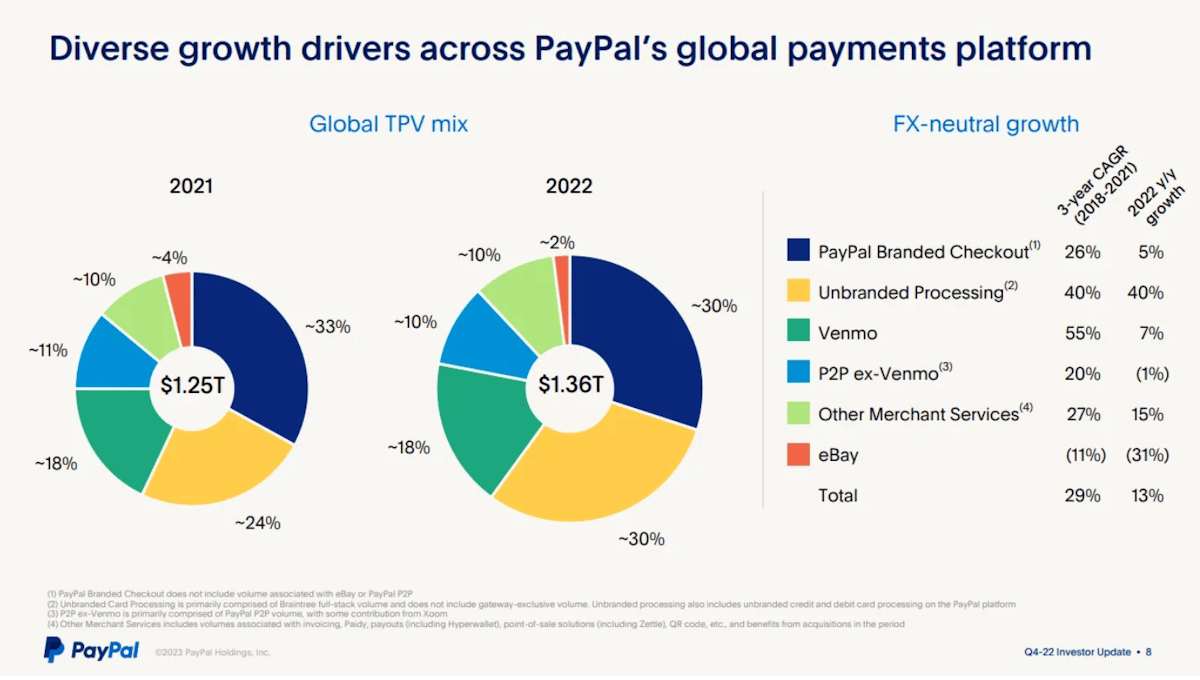

I’m expecting PayPal to keep the volume of payments it processes growing at 25% annually. This is roughly equal to growth rates over the last decade. This would result in TPV increasing from $1.36 trillion in 2022 to $5.2 trillion in 2028.

I believe that pressure on fees, and the growth of Venmo within the mix will result in the take rate (revenue as a percentage of TPV) falling from 2.03% to 1.4% by 2028. PayPal would therefore earn revenue $72.5 billion (1.4% of $5.2 trillion) in 2028, which is a 20% annual revenue growth rate

I also expect PayPal’s gross margin to fall as the company will need to share more revenue with partners. I’m expecting the gross margin to fall from the 2022 level of 42.3% to 34% by 2028. This implies a gross profit will be $26.7 billion based on the above assumptions.

OpEx Margin will Stabilize at 25%

PayPal has cut costs (head count and stock based compensation) in the last year which has resulted in operating expenses falling from around 28% of revenue to 24%. I think the company will need to settle on a long term opex margin of 25% to remain competitive.

This assumption implies 2028 operating expenses of $17 billion, and operating income of $6.2 billion, or around 9% of revenue.

I’m calculating net income for 2028 at 83% of operating income which is the average over the last decade, since interest and taxes make up around 17% of operating income.

That means, OPERATING income of $6.2bn (income before interest and taxes) would deliver NET income (income after interest and taxes) of $5.14bn.

This implies net margins will compress from 14.3% today, to 7% by 2028. While the company will have plenty of revenue growth, earnings will grow much slower.

Share Buybacks to Continue

I’m assuming that share buy backs will continue at the current rate of 1% of outstanding shares per year, as the company will have enough cash flow to do so. This would imply that the outstanding share count will be 1.09 billion in 2028.

Risks

The narratives I’ve outlined are based on PayPal’s current strategy. The outlook could change completely with a major partnership (or merger) with a company that compliments its products. This could be a bank, or an e-commerce or media business.

There is a particular set of catalysts that could derail the narrative I’ve outlined. PayPal is in the process of cutting costs, which may well result in margins improving over the next 6 to 24 months. If that happens, and at the same time a new strategy or set of partnerships leads to an improved outlook going forward, then margins may not ever decline in the way I expect, and I would update my forecasts accordingly.

How well do narratives help inform your perspective?