Narratives are currently in beta

Key Takeaways

- Partnering with WebBank could increase profitability by streamlining operations and enhancing net margins.

- Enhancing shopping features and increased marketing are expected to boost consumer engagement and revenue growth.

- Sezzle's strategic partnerships, product innovations, and marketing initiatives are driving substantial user growth and revenue increases, indicating strong future financial performance and market position.

Catalysts

About Sezzle- Operates as a technology-enabled payments company primarily in the United States and Canada.

- The partnership with WebBank is expected to simplify operations and increase profitability by unifying regulatory procedures across jurisdictions, potentially leading to enhanced net margins.

- The introduction of the On-Demand product is expected to boost user activation by 30%, providing a new monetization avenue and potentially driving revenue growth.

- Sezzle's focus on enhancing shopping features is projected to increase product stickiness and consumer lifetime value, which could positively impact future revenue.

- Expected changes in tax status and associated headwinds in 2025, despite raised EPS guidance, indicate challenges in maintaining profit margins.

- Increased marketing expenditure following the political season aims to drive consumer awareness and acquisition, which could support further revenue growth.

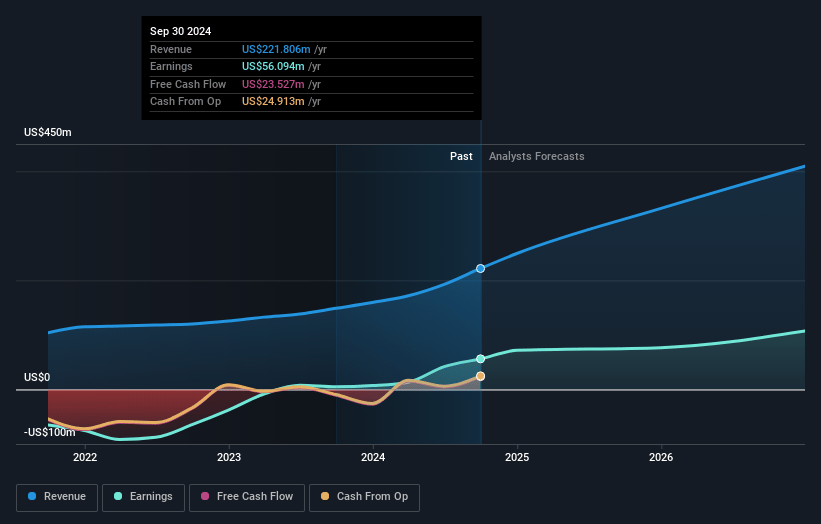

Sezzle Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Sezzle's revenue will grow by 29.5% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 25.3% today to 20.7% in 3 years time.

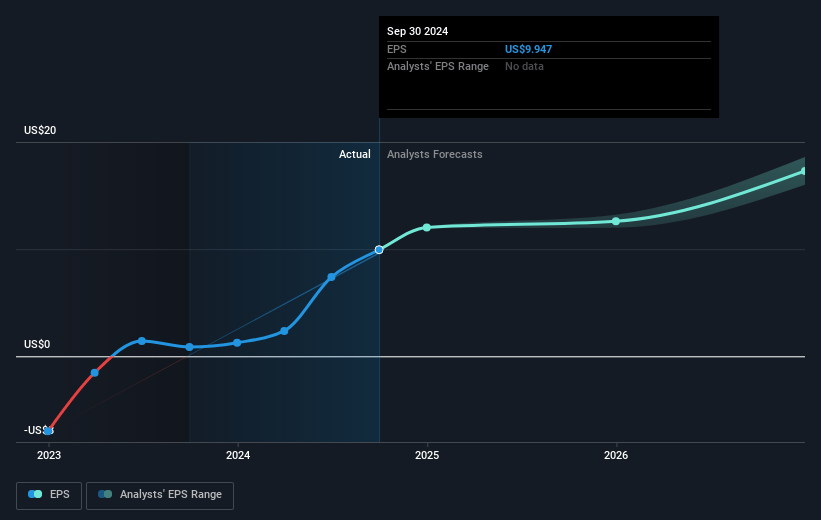

- Analysts expect earnings to reach $99.5 million (and earnings per share of $14.65) by about December 2027, up from $56.1 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 24.0x on those 2027 earnings, down from 32.0x today. This future PE is greater than the current PE for the US Diversified Financial industry at 18.2x.

- Analysts expect the number of shares outstanding to grow by 6.61% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.79%, as per the Simply Wall St company report.

Sezzle Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Sezzle's partnership with WebBank allows it to streamline operations and standardize regulatory practices at a national level, enhancing profitability by reducing complexity and increasing revenue from certain states. This streamlined and unified product structure could positively impact net margins and earnings.

- The launch of the On-Demand product potentially broadens Sezzle's user base by facilitating consumer activation, which could lead to sustainable revenue growth and improved financial performance. This initiative may significantly increase Sezzle's revenues and earnings.

- With a 71.3% year-over-year revenue increase attributable to rising consumer purchase frequency and expanding subscriber count, Sezzle is outpacing industry growth, which could signal robust future revenue and earnings growth.

- Sezzle's product development, such as the On-Demand Pay-in-4 service, aims to enhance user experience and promote user engagement without requiring long-term commitments upfront, which could leverage customer acquisition and boost long-term revenue streams and consumer lifetime value.

- Sezzle's strategic approach to marketing and product awareness, including branding partnerships like the NBA Timberwolves sponsorship, aims to expand product reach and company visibility, potentially driving revenue growth through heightened consumer engagement and brand recognition.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $326.5 for Sezzle based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2027, revenues will be $481.8 million, earnings will come to $99.5 million, and it would be trading on a PE ratio of 24.0x, assuming you use a discount rate of 6.8%.

- Given the current share price of $320.06, the analyst's price target of $326.5 is 2.0% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives