Narratives are currently in beta

Key Takeaways

- Patria's diversification and expansion into new markets and products are expected to boost revenue and drive long-term growth.

- Recent acquisitions and strong growth in real estate and credit platforms offer efficiency gains and income enhancement opportunities.

- Increased operating expenses and tax rates, along with potential M&A activities, may pressure net margins and earnings amidst rising debts and uncertain revenue performance.

Catalysts

About Patria Investments- Operates as a private market investment firm focused on investing in Latin America.

- Patria's robust fundraising momentum, with over $4.2 billion raised year-to-date and on track to exceed their $5 billion target for 2024, indicates strong revenue growth potential as Fee Earning AUM continues to expand.

- The diversification strategy and expansion into new products and geographies, including the integration of the GPMS platform and entering new markets like Colombia and potentially Mexico, are expected to impact revenue and long-term growth positively.

- The integration of recent acquisitions, such as the Global Private Market Solutions business from abrdn and the Credit Suisse Real Estate Investment Trust, provides opportunities for efficiency gains and margin improvements, which should enhance net margins in the future.

- Patria's real estate and credit platforms are experiencing strong growth, with private credit strategies poised to leverage ongoing high interest rate environments. This could lead to enhanced fee-related earnings and revenue compounding over time.

- The expected performance fees from infrastructure strategies, notably Infrastructure Fund III in its catch-up phase, and the anticipated further deployment opportunities are likely to boost earnings and contribute to distributable earnings growth.

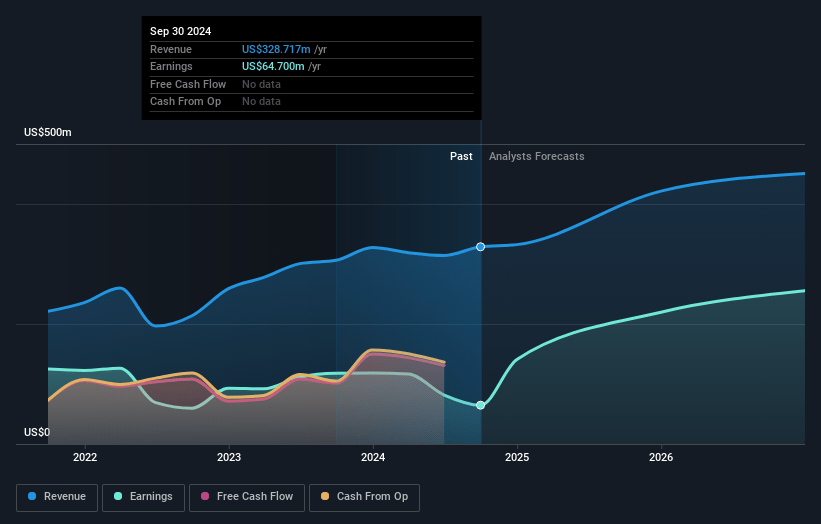

Patria Investments Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Patria Investments's revenue will grow by 14.4% annually over the next 3 years.

- Analysts assume that profit margins will increase from 19.7% today to 68.2% in 3 years time.

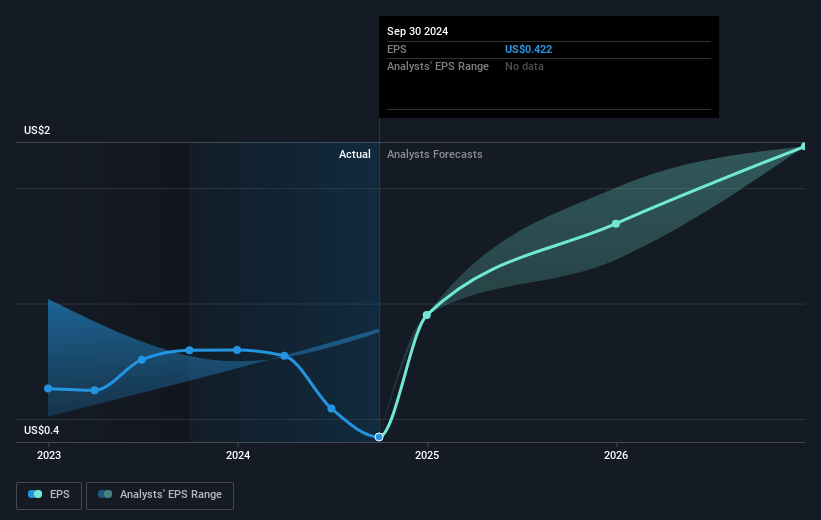

- Analysts expect earnings to reach $336.0 million (and earnings per share of $2.13) by about January 2028, up from $64.7 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 8.7x on those 2028 earnings, down from 28.3x today. This future PE is lower than the current PE for the US Capital Markets industry at 23.1x.

- Analysts expect the number of shares outstanding to grow by 0.95% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.07%, as per the Simply Wall St company report.

Patria Investments Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The company has seen an increase in operating expenses primarily due to acquisitions, increased personnel costs, inflation, and expanded equity compensation, which could put pressure on net margins and earnings.

- The effective tax rate is expected to increase in the coming years due to geographic diversification and a shift in income mix, which could negatively impact net earnings.

- While the company has no current M&A plans for the next few quarters, previous acquisitions have had short-term negative impacts on margins, and any future M&A could again lead to similar outcomes, affecting net margins and earnings.

- The company’s debt is expected to peak at $190 million by year-end due to M&A and year-end payments, and while they plan to reduce it, higher interest expenses could impact bottom-line earnings.

- Performance fees were not realized in the quarter, and dependency on future performance fees could introduce variability in revenues and earnings if investment performance does not meet expectations.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $15.17 for Patria Investments based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $18.0, and the most bearish reporting a price target of just $13.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $492.4 million, earnings will come to $336.0 million, and it would be trading on a PE ratio of 8.7x, assuming you use a discount rate of 7.1%.

- Given the current share price of $11.93, the analyst's price target of $15.17 is 21.3% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives