Narratives are currently in beta

Key Takeaways

- Reduction of problematic paper is set to improve portfolio quality and reduce credit losses, positively impacting margins and earnings.

- AI and e-contracting enhance processing speed and accuracy, leading to cost reduction and increased scalability, potentially boosting net margins.

- Rising expenses, increased charge-offs, and higher delinquencies could pressure profitability, with technology reliance posing additional operational risk.

Catalysts

About Consumer Portfolio Services- Operates as a specialty finance company in the United States.

- The reduction of problematic paper from 2022 and early 2023 to less than 33% of the portfolio is expected to improve the quality of the portfolio and reduce future credit losses, positively impacting net margins and earnings.

- The strong origination growth, particularly in October, is an indicator of increasing revenue potential, as the company is on track to achieve a year-over-year growth rate of 18% to 20%.

- The successful reduction of funding time to 1.79 days and improvement in same-day funding is likely to strengthen dealer relationships and capture more business, driving future revenue growth.

- The implementation of AI and e-contracting to enhance processing speed and accuracy can lead to operational efficiencies, potentially improving net margins through reduced costs and increased scalability.

- The anticipated rate cuts by the Federal Reserve, coupled with the company's strong positioning in securitization markets, could lower interest expenses and enhance net interest margins and earnings in the future.

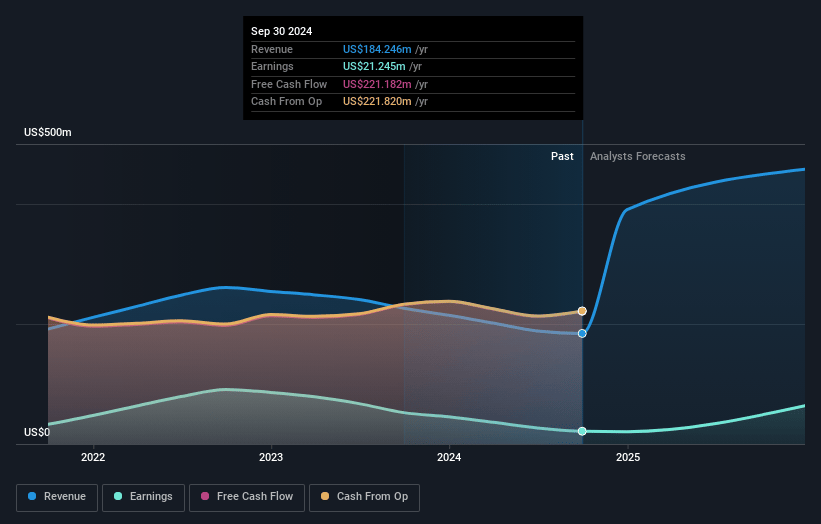

Consumer Portfolio Services Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Consumer Portfolio Services's revenue will grow by 76.1% annually over the next 3 years.

- Analysts assume that profit margins will increase from 11.5% today to 21.9% in 3 years time.

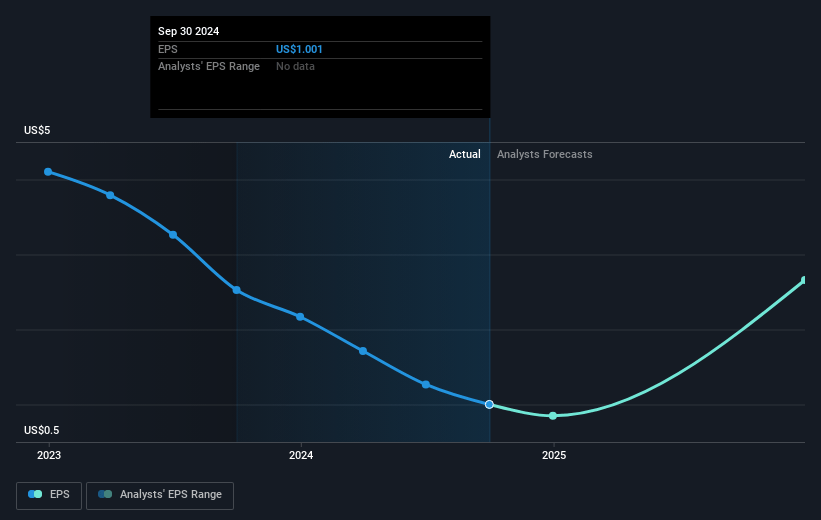

- Analysts expect earnings to reach $220.7 million (and earnings per share of $8.58) by about November 2027, up from $21.2 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 2.8x on those 2027 earnings, down from 10.7x today. This future PE is lower than the current PE for the US Consumer Finance industry at 12.1x.

- Analysts expect the number of shares outstanding to grow by 6.3% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 10.86%, as per the Simply Wall St company report.

Consumer Portfolio Services Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The net income for the quarter decreased significantly to $4.8 million from $10.4 million the previous year, indicating potential challenges in maintaining profitability. This decline could impact future earnings growth.

- Rising expenses, particularly a 28% increase in the securitization and credit line debt balance, driven by higher interest expenses, may continue to pressure net margins if interest rates remain high or increase further.

- The annualized net charge-offs increased to 7.53% from 6.86%, and delinquencies over 30 days rose to 14.04% from 12.31%. These higher delinquency rates could adversely affect the net interest margin and lead to increased future losses.

- While the portfolio and origination growth are substantial, the fact that pretax earnings dropped from $14.2 million to $6.9 million suggests that revenue growth may not be translating effectively into bottom-line growth, potentially impacting future profitability.

- The heavy reliance on AI and new technologies for fraud prevention and processing may present technology risk if these systems fail or do not operate as expected, potentially leading to higher losses and impacting earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $18.0 for Consumer Portfolio Services based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2027, revenues will be $1.0 billion, earnings will come to $220.7 million, and it would be trading on a PE ratio of 2.8x, assuming you use a discount rate of 10.9%.

- Given the current share price of $10.59, the analyst's price target of $18.0 is 41.2% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives