Last Update 24 Jun 26

Fair value Decreased 1.26%CME: Crypto Perpetual Futures Dispute Will Shape Future Earnings Power

The analyst price target for CME Group has shifted slightly lower, with fair value moving from about $306.47 to $302.60 as analysts weigh ongoing concerns around perpetual futures and potential multiple compression against views that recent share weakness and structural demand drivers still support an attractive long term setup.

Analyst Commentary

Recent research on CME Group shows a split between bullish analysts who see the recent pullback and product portfolio as supportive for long term value, and more cautious voices focused on competitive threats from perpetual futures and the potential impact on valuation multiples.

Bullish Takeaways

- Bullish analysts highlight what they view as an attractive risk and reward setup after the recent share selloff, arguing that current pricing already reflects considerable concern around perpetual futures.

- Some see CME Group as a key beneficiary of what they describe as structural tailwinds around retail trading, prediction markets, and ledger technology efficiencies, which they link to the company’s existing franchise and product reach.

- Positive commentary points to high margins, strong cash generation and an attractive dividend yield as supporting factors for equity holders focused on income and capital discipline.

- Several bullish analysts keep or raise targets in the US$300 range or higher. They indicate that they still see room for upside versus the latest trading levels, even after accounting for new competitive developments.

Bearish Takeaways

- Bearish analysts focus on the emergence of bitcoin perpetual futures and potential extensions into other asset classes, which they see as a source of ongoing terminal value concerns that could limit stock multiples for CME Group.

- Some expect that if geopolitical uncertainties ease, trading volumes and related transaction fees could soften, which they link to a possible moderation in revenue momentum over time.

- Cautious views also emphasize competitive risk from new products targeting the retail segment, particularly around perpetual futures, and argue that this may pressure valuation even if current institutional demand remains limited.

- Several research notes reference target cuts across exchange stocks, including CME Group. Analysts factor in what they regard as a more competitive setup and the possibility of lower long term growth assumptions in their models.

What’s in the News for CME Group

- CME Group has filed a federal lawsuit against the CFTC over its approval of bitcoin perpetual futures offered by Kalshi and Coinbase, arguing these products should be treated as swaps under Dodd Frank and that the regulator bypassed required public comment and overstepped its legal authority, source: recent lawsuit coverage.

- Chairman and CEO Terry Duffy is set to step down from the CEO role on March 1, 2027, moving to Executive Chairman, while current President and CFO Lynne Fitzpatrick will become CEO on the same transition date, signaling an internal succession plan, source: company leadership transition announcement.

- CME Group has launched Nasdaq CME Crypto Index Futures, cash settled contracts tied to a Nasdaq CME index that tracks several large cryptocurrencies, aiming to give traders a single regulated futures contract for diversified digital asset exposure, source: crypto index futures launch reports.

- The company has outlined plans for 24/7 trading in smaller sized WTI crude oil and 1 ounce gold futures, subject to regulatory approval, with the CFTC reviewing whether continuous oil trading could increase volatility during market stress, source: commodity futures expansion coverage.

- CME Group continues to broaden its equity and crypto product suite with new E mini futures on broad U.S. equity benchmarks, Micro E mini S&P 500 and Nasdaq 100 options, and a multi year Morningstar index licensing agreement to support new equity index derivatives, source: product launch announcements.

Valuation Changes for CME Group

- Fair Value: The analyst fair value estimate for CME Group has edged lower from $306.47 to $302.60, indicating a small downward adjustment in the modeled price level.

- Discount Rate: The discount rate has risen slightly from 7.77% to 7.82%, reflecting a modest increase in the required return used in the valuation model.

- Revenue Growth: The modeled revenue growth rate has moved up from 5.14% to 5.40%, indicating a small uptick in forward growth assumptions for revenue in dollar terms.

- Net Profit Margin: The projected net profit margin has increased from 58.35% to 60.78%, pointing to higher expected profitability on future earnings in dollar terms.

- Future P/E: The future P/E multiple has been marked down from 30.87x to 29.08x, suggesting slightly lower valuation multiples applied to CME Group’s expected earnings.

Key Takeaways

- Strong global demand for risk management, retail engagement, and international expansion drives volume and revenue growth, diversifying CME's client base.

- Innovation in products, technology, and partnerships enhances efficiency and margins, positioning CME for sustainable long-term earnings growth.

- Competitive threats from DeFi, regulatory shifts, and low volatility could erode CME Group's market share, trading volumes, and profit margins over time.

Catalysts

About CME Group- Operates contract markets for the trading of futures and options on futures contracts worldwide.

- Heightened global macroeconomic uncertainty, record sovereign debt issuance, persistent geopolitical tensions, and ongoing trade disputes are fueling sustained demand for risk management and hedging solutions, evidenced by record contract volumes and open interest; this trend is likely to support continued revenue and fee growth.

- Robust international expansion-with record-breaking double-digit ADV growth across EMEA and APAC and rising participation from both institutional and retail clients globally-broadens CME's addressable market and underpins future volume and revenue growth.

- The rapid acceleration of retail engagement, highlighted by a 56% increase in new retail traders and five consecutive quarters of double-digit retail client acquisition growth, diversifies CME's client base and supports both volume and transaction-based revenue growth.

- New product innovations (e.g., Micro contracts, expansion into crypto, FX Spot+), ongoing tech-driven operating efficiencies (cloud migration and tokenization initiatives), and strengthening of strategic partnerships (such as the long-term NASDAQ index license extension and Google Cloud collaboration) are enhancing operating leverage and EBITDA/net margin performance.

- The ongoing global shift toward electronic trading, greater regulatory demands for transparency and standardized clearing, and a proven ability to grow non-transactional revenue (e.g., record market data revenue) position CME to capture a larger share of trading activity and support durable long-term earnings growth.

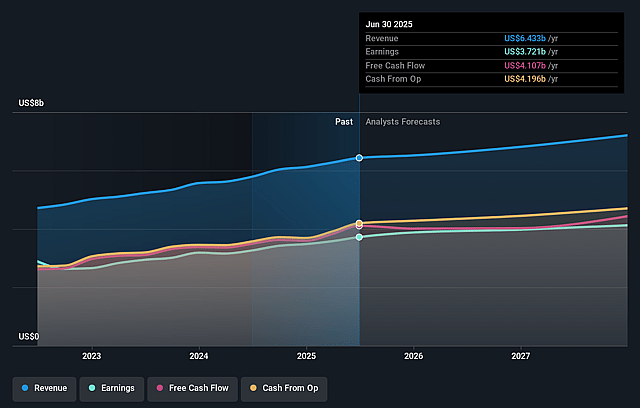

CME Group Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming CME Group's revenue will grow by 5.4% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 62.9% today to 60.8% in 3 years time.

- Analysts expect earnings to reach $4.8 billion (and earnings per share of $13.43) by about June 2029, up from $4.2 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 29.1x on those 2029 earnings, up from 19.8x today. This future PE is lower than the current PE for the US Capital Markets industry at 40.5x.

- Analysts expect the number of shares outstanding to grow by 0.55% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.82%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Prolonged periods of geopolitical stability and reduced headline risk could curb market volatility, lowering overall demand for risk-hedging and derivatives trading, which may lead to declining trading volumes and negatively impact CME Group's revenue and earnings growth.

- The accelerating adoption of decentralized finance (DeFi) and tokenization technologies poses a long-term competitive threat, as new market structures could enable trading and settlement of derivatives outside of centralized venues like CME, potentially reducing future market share and fee revenues.

- CME's continued heavy reliance on trading activity in interest rate and equity futures exposes the company to periods of subdued volatility or volume in those sectors, which could result in revenue stagnation or contraction and put pressure on net margins.

- Regulatory changes-such as potential increased oversight of retail derivatives trading, limitations on certain products (e.g., perpetuals in the U.S.), or global moves to further tighten derivatives market participation-may dampen speculative activity and reduce overall transaction fees and open interest.

- Intensifying industry competition from alternative electronic trading venues, lower-fee platforms, and the proliferation of OTC derivatives and algorithmic solutions could create sustained pricing pressure, eroding net margins and constraining CME's long-term earnings growth.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $302.6 for CME Group based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $353.0, and the most bearish reporting a price target of just $230.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $7.9 billion, earnings will come to $4.8 billion, and it would be trading on a PE ratio of 29.1x, assuming you use a discount rate of 7.8%.

- Given the current share price of $231.58, the analyst price target of $302.6 is 23.5% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on CME Group?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.