Key Takeaways

- Leadership changes and strategic initiatives at IHOP aim to boost innovation, global strategy, and sales, positively impacting revenue and earnings.

- Expanding value offerings, off-premise sales, and brand partnerships are expected to drive traffic, enhance margins, and increase revenue.

- Increased competition and consumer financial pressures challenge Dine Brands' revenue growth, while strategic changes create uncertainty and execution risks affecting operational stability.

Catalysts

About Dine Brands Global- Owns, franchises, and operates restaurants in the United States and internationally.

- The leadership transition at IHOP, with Lawrence Kim taking over as President, is anticipated to bring fresh perspectives, potentially driving innovation, global brand strategy, and sales growth at IHOP, thereby positively impacting future revenue and earnings.

- The introduction of more stable value offerings at both Applebee's and IHOP aims to address consumer demand for all-encompassing value experiences, which could enhance customer traffic and positively affect revenue and net margins by reducing promotional volatility.

- Applebee's partnership with the NFL and new promotional campaigns, such as the $0.50 Boneless Wings and new Big Meal Deal, are expected to leverage brand alliances, drive traffic, and improve average check size, potentially enhancing future revenue.

- Expanding off-premise sales, focusing on extending promotions and limited-time offers to off-premise channels, is expected to capitalize on the growing demand for convenience, thereby positively impacting revenue and margins at Applebee's and IHOP.

- The dual brand concept, combining IHOP and Applebee's offerings in the same location, has shown to generate significantly higher revenue than single-brand restaurants, and its expansion could drive improved revenue and earnings across the system, particularly with upcoming domestic openings.

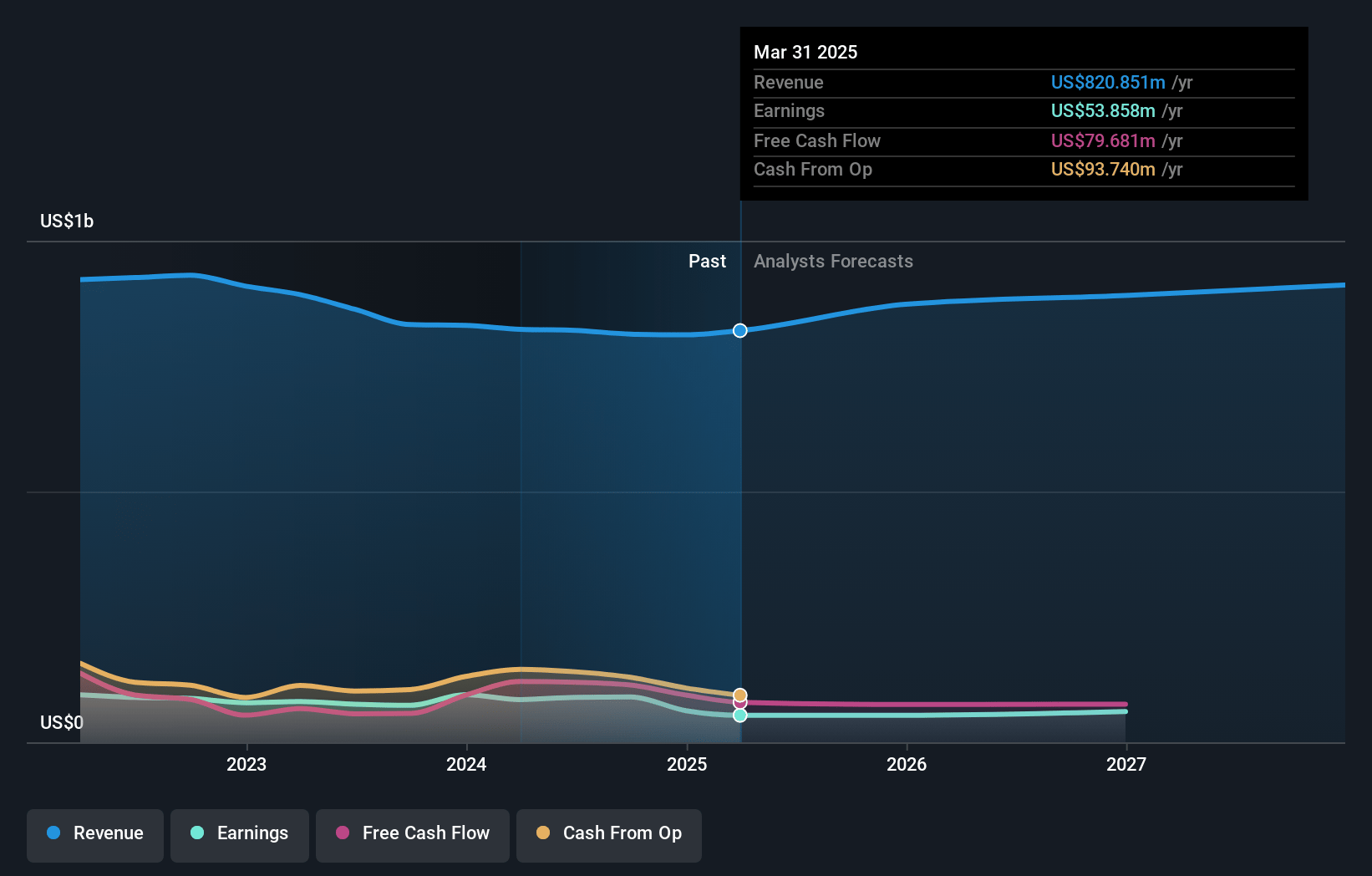

Dine Brands Global Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Dine Brands Global's revenue will decrease by 0.3% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 11.1% today to 6.8% in 3 years time.

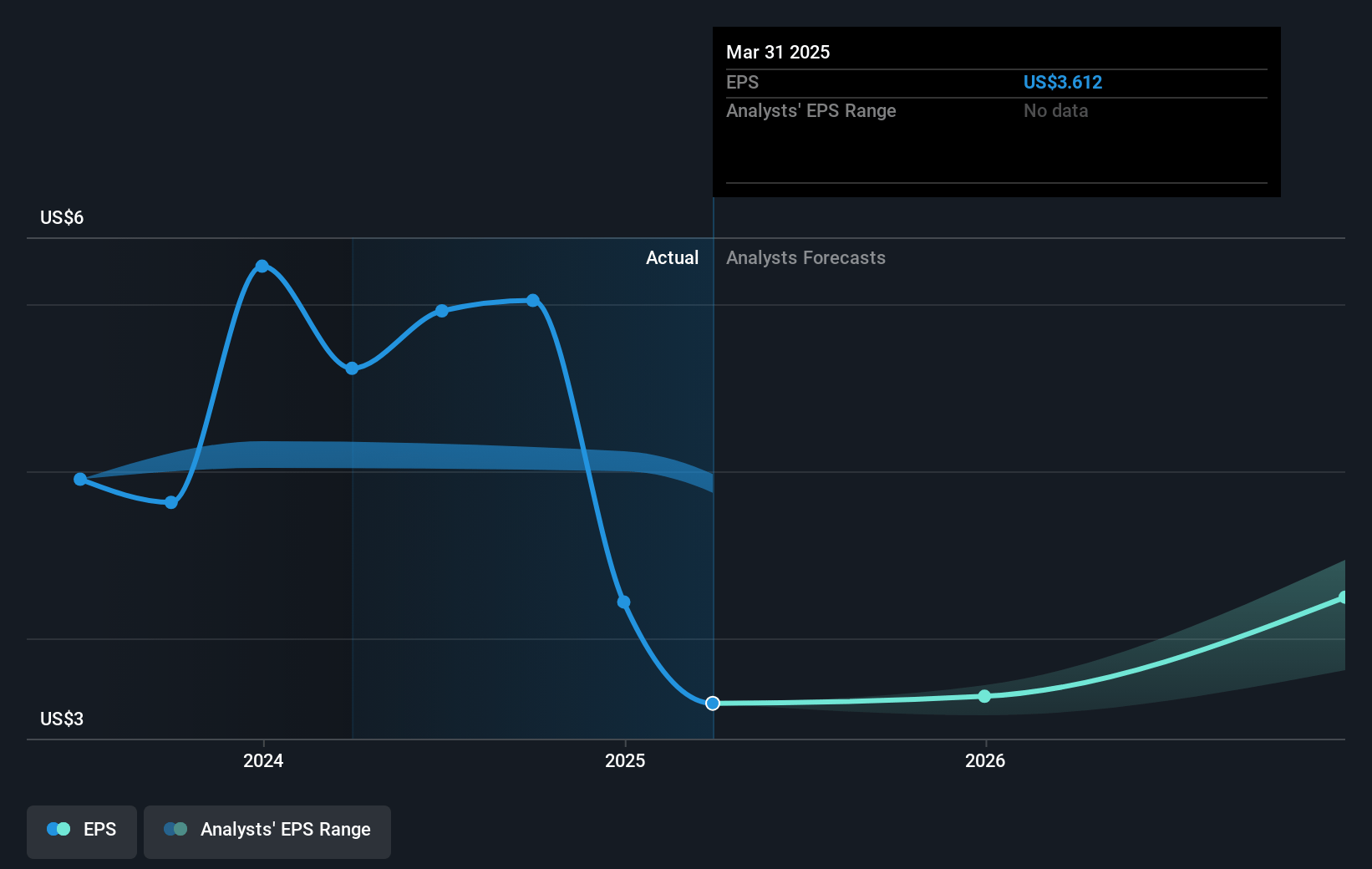

- Analysts expect earnings to reach $56.1 million (and earnings per share of $3.87) by about January 2028, down from $90.2 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 13.0x on those 2028 earnings, up from 5.2x today. This future PE is lower than the current PE for the US Hospitality industry at 24.3x.

- Analysts expect the number of shares outstanding to decline by 1.62% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 10.86%, as per the Simply Wall St company report.

Dine Brands Global Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The competitive and promotional environment in the dining sector remains a challenge, impacting the ability of Dine Brands' core brands, Applebee's and IHOP, to drive traffic and same-store sales growth, which could pressure revenue.

- Consumer demographics, particularly the lower-income segment, are under financial pressure and are opting to eat at home more, potentially impacting sales revenue and customer traffic further.

- Consolidated revenues decreased $7.6 million, with Applebee's reporting a 5.9% decline and IHOP a 2.1% decline in comparable sales, indicating challenges in maintaining top-line growth.

- Financial results showed a decrease in franchise and rental revenues due primarily to terminations and market pressures, which can affect net margins and overall profitability.

- Operational and strategic transitions, such as IHOP's leadership change, bring uncertainty and execution risk, which might affect the operational stability and potentially impact earnings in the near term.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $38.14 for Dine Brands Global based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $47.0, and the most bearish reporting a price target of just $32.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $821.6 million, earnings will come to $56.1 million, and it would be trading on a PE ratio of 13.0x, assuming you use a discount rate of 10.9%.

- Given the current share price of $31.06, the analyst's price target of $38.14 is 18.6% higher. Despite analysts expecting the underlying buisness to decline, they seem to believe it's more valuable than what the market thinks.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives