Last Update 20 Dec 25

BRSL: Jackpot Normalization Will Drive Multiple Expansion And Sustain Next Phase Of Upside

Analysts modestly lifted their Brightstar Lottery price target to about $20 per share from the prior $18 level, citing building estimate momentum, multiple growth vectors, and the potential for a valuation multiple re rating as organic growth accelerates.

Analyst Commentary

Bullish analysts highlight that the recent lift in the price target reflects growing confidence in Brightstar Lottery's ability to convert its robust pipeline and product portfolio into faster organic revenue growth, supporting a higher valuation framework over the medium term.

They point to the recent Powerball and Mega Millions jackpots as a key near term catalyst that is likely to drive Q3 upside, reinforcing the view that normalized jackpot activity can sustain elevated ticket volumes and strengthen earnings visibility.

As management continues to engage the investment community through investor meetings, bullish analysts also see improved execution transparency and clearer communication around growth initiatives as incremental positives for both sentiment and the potential for a valuation multiple re rating.

At the same time, some market participants caution that the pace of organic growth and the durability of jackpot driven upside will need to be demonstrated consistently before the shares can fully re rate to the higher end of peer valuation ranges.

Bullish Takeaways

- Recent target increases are framed around accelerating organic growth, with bullish analysts expecting multiple growth vectors to support sustained top line expansion and justify a higher price target range.

- Jackpot normalization and recent high profile jackpots are viewed as structural and cyclical tailwinds that can lift near term earnings and reduce volatility in forward estimates.

- Stronger estimate momentum, driven by improved visibility into Q3 upside, is seen as a catalyst for continued positive revisions and incremental multiple expansion.

- Ongoing investor engagement by management is interpreted as a sign of execution confidence, helping to narrow perception gaps and support a re rating closer to growth oriented lottery and gaming peers.

Bearish Takeaways

- Bearish analysts remain cautious that a portion of the recent upside is tied to jackpot driven demand, which may not be fully repeatable and could lead to choppier results once jackpot levels normalize.

- There is concern that expectations for an inflection in organic growth may now be embedded in the valuation, leaving less room for error if execution around new initiatives or markets is slower than anticipated.

- Some investors worry that the case for a sustained multiple re rating still relies heavily on external demand catalysts rather than fully proven, internally driven growth levers.

- A higher price target range increases the bar for future performance, and any signs of estimate cuts or softer ticket trends could prompt a pullback in the shares from current levels.

What's in the News

- Signed a 19 year lottery technology and digital products contract with Lotterywest in Western Australia, including a new central gaming system, 775 Retailer Pro S2 terminals, and expanded local economic commitments (Client Announcements).

- Launched patented Cash Pop draw based game with the Pennsylvania Lottery, the 17th U.S. state to offer the game and the first to debut with a $20 price point; this supports higher per ticket spending (Product Related Announcements).

- Entered a five year exclusive global licensing agreement with Spin Master to develop Rubik's themed omnichannel lottery games, adding a high profile branded franchise to the portfolio (Client Announcements).

- Extended its technology and services contract with the Texas Department of Licensing and Regulation through August 31, 2028, reinforcing its position with a major U.S. lottery customer (Client Announcements).

- Completed a $250 million share repurchase totaling 6.69% of shares outstanding and raised the quarterly dividend 10% to $0.22 per share while reaffirming 2025 guidance and targeting $2.75 billion of revenue by 2028, which implies over 5% organic CAGR (Buyback Tranche Update, Dividend Increases, Corporate Guidance).

Valuation Changes

- The fair value estimate remains unchanged at approximately $20.17 per share, indicating no shift in the underlying intrinsic value assessment.

- The discount rate edged lower from about 13.40% to 13.25%, reflecting a slightly reduced perceived risk profile in the valuation model.

- The revenue growth assumption increased from roughly 1.21% to 1.30%, signaling a modest improvement in expected top line expansion over the forecast period.

- The net profit margin was nudged down marginally from about 12.03% to 12.00%, suggesting a slightly more conservative view on future profitability.

- The future P/E multiple ticked down from roughly 14.93x to 14.88x, implying a very small recalibration of the earnings multiple applied in the forward valuation.

Key Takeaways

- Expansion of digital channels and contract renewals are providing stable, long-term revenue growth and higher-margin opportunities.

- Investments in technology, cost-cutting, and product innovation enhance customer engagement, reduce expenses, and strengthen recurring revenues.

- Regulatory risks, earnings volatility, geographic concentration, rising competition, and high contract costs threaten revenue stability, margin growth, and financial flexibility.

Catalysts

About Brightstar Lottery- Provides lottery solutions in the United States, Italy, rest of Europe, and internationally.

- Accelerating digital adoption and smartphone penetration are driving double-digit growth in iLottery wagers globally (over 30% growth cited), with Italy and US adoption rates outpacing the overall market-likely supporting higher future revenue growth and improving the business mix toward higher-margin digital channels.

- Regulatory liberalization and successful contract renewals (notably Italy Lotto secured through 2034 and new/extended deals in Missouri, Portugal, and France) are expanding the addressable market and extending Brightstar's average revenue-weighted contract life to 7 years, thus providing long-term revenue stability and enhanced cash flow visibility.

- Ongoing investment in proprietary digital platforms (including the MYLOTTERIES app and integrated OMNIA solution) is reducing customer acquisition costs while bolstering direct-to-consumer engagement, suggesting further net margin expansion as platform scale and technology investments pay off.

- Implementation and expansion of structural cost-cutting initiatives (OPtiMa 3.0) are expected to drive $50 million in annualized savings by 2026 (60% realized this year), helping to offset temporary profit headwinds and support a rebound to normalized EBITDA and free cash flow, directly benefiting earnings in the coming years.

- Secular trends toward gamification and instant play, combined with innovation in ticket technology (Gleam, Infinity Instants) and expanded instant ticket printing capacity (running 25% above last year's output), position Brightstar to capture sustained demand and cross-selling opportunities, increasing both recurring revenues and customer lifetime value.

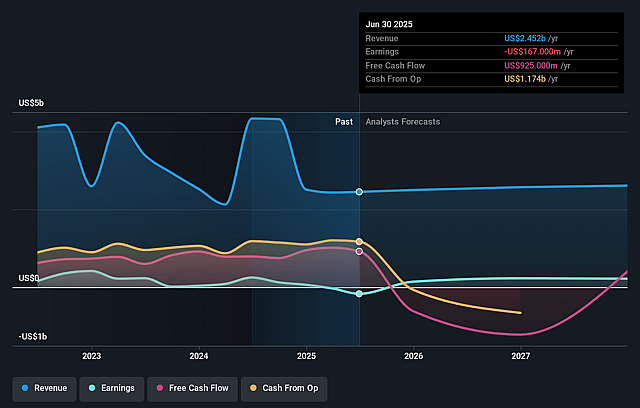

Brightstar Lottery Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Brightstar Lottery's revenue will grow by 2.5% annually over the next 3 years.

- Analysts assume that profit margins will increase from -6.8% today to 11.2% in 3 years time.

- Analysts expect earnings to reach $295.9 million (and earnings per share of $0.87) by about September 2028, up from $-167.0 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 17.5x on those 2028 earnings, up from -18.5x today. This future PE is lower than the current PE for the US Hospitality industry at 24.0x.

- Analysts expect the number of shares outstanding to grow by 0.5% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 13.28%, as per the Simply Wall St company report.

Brightstar Lottery Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Increasing regulatory scrutiny and possible tightening of gambling regulations or tax changes in key markets (such as the U.S., Italy, or emerging international markets) could limit growth opportunities, heighten compliance costs, or reduce overall profitability, negatively impacting revenue and net margins.

- Heavy reliance on extremely large, sporadic multistate jackpots for windfall periods of higher revenue creates ongoing earnings volatility and uncertainty, as periods without such jackpots have already shown EBITDA compression and weaker momentum in top line growth and profit, affecting both revenue and earnings stability.

- Geographic concentration risk remains, as Italy is described repeatedly as the company's most important market and a major profit driver; any adverse regulatory, economic, or competitive changes in Italy could significantly disrupt the company's revenue streams and earnings consistency.

- The lottery sector faces intensifying competition from both new digital entrants (including private operators and government-backed platforms) and alternative entertainment options (like digital gaming and esports), which may erode Brightstar's market share, create pricing pressures, and stagnate or reduce ticket sales, impacting long-term revenue growth and net margins.

- The high upfront capital requirements and ongoing amortization costs of securing long-term operator contracts (as seen with the Italy Lotto license) may pressure cash flows and constrain financial flexibility; if growth or margin expansion does not offset these significant obligations, free cash flow and profitability could be negatively affected.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $18.517 for Brightstar Lottery based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $28.0, and the most bearish reporting a price target of just $12.52.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $2.6 billion, earnings will come to $295.9 million, and it would be trading on a PE ratio of 17.5x, assuming you use a discount rate of 13.3%.

- Given the current share price of $16.29, the analyst price target of $18.52 is 12.0% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Brightstar Lottery?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.