Narratives are currently in beta

Key Takeaways

- Expanding in back-up care and technology initiatives enhances revenue growth, net margins, and client engagement.

- U.K. progress and education advisory investments boost profitability and long-term earnings potential.

- Slow recovery in key segments and challenges in U.K. operations, along with potential center closures, could impact revenue growth and overall profitability.

Catalysts

About Bright Horizons Family Solutions- Provides early education and childcare, back-up care, educational advisory, and other workplace solutions services for employers and families in the United States, Puerto Rico, the United Kingdom, the Netherlands, Australia, and India.

- Bright Horizons Family Solutions is expanding its client base in the back-up care segment, adding new clients such as Progressive Corporation and Brookfield Property, which is expected to drive revenue growth and improve operating margins due to economies of scale.

- The company is making operational and financial progress in the U.K. and anticipates continued improvements towards pre-pandemic performance levels, which should lead to better net margins and overall profitability.

- Investments in technology initiatives and personalized marketing in the back-up care segment are resulting in increased use and employee engagement, positioning the company for revenue growth and improved net margins through operational efficiencies.

- The education advisory business is focusing on revitalizing participant growth through investments in team, product, and marketing, which is expected to boost revenue growth and improve long-term earnings potential.

- The successful hosting of the On the Horizon Summit has reinforced client relationships and could lead to increased client retention and expansion opportunities, positively impacting future revenue growth and earnings.

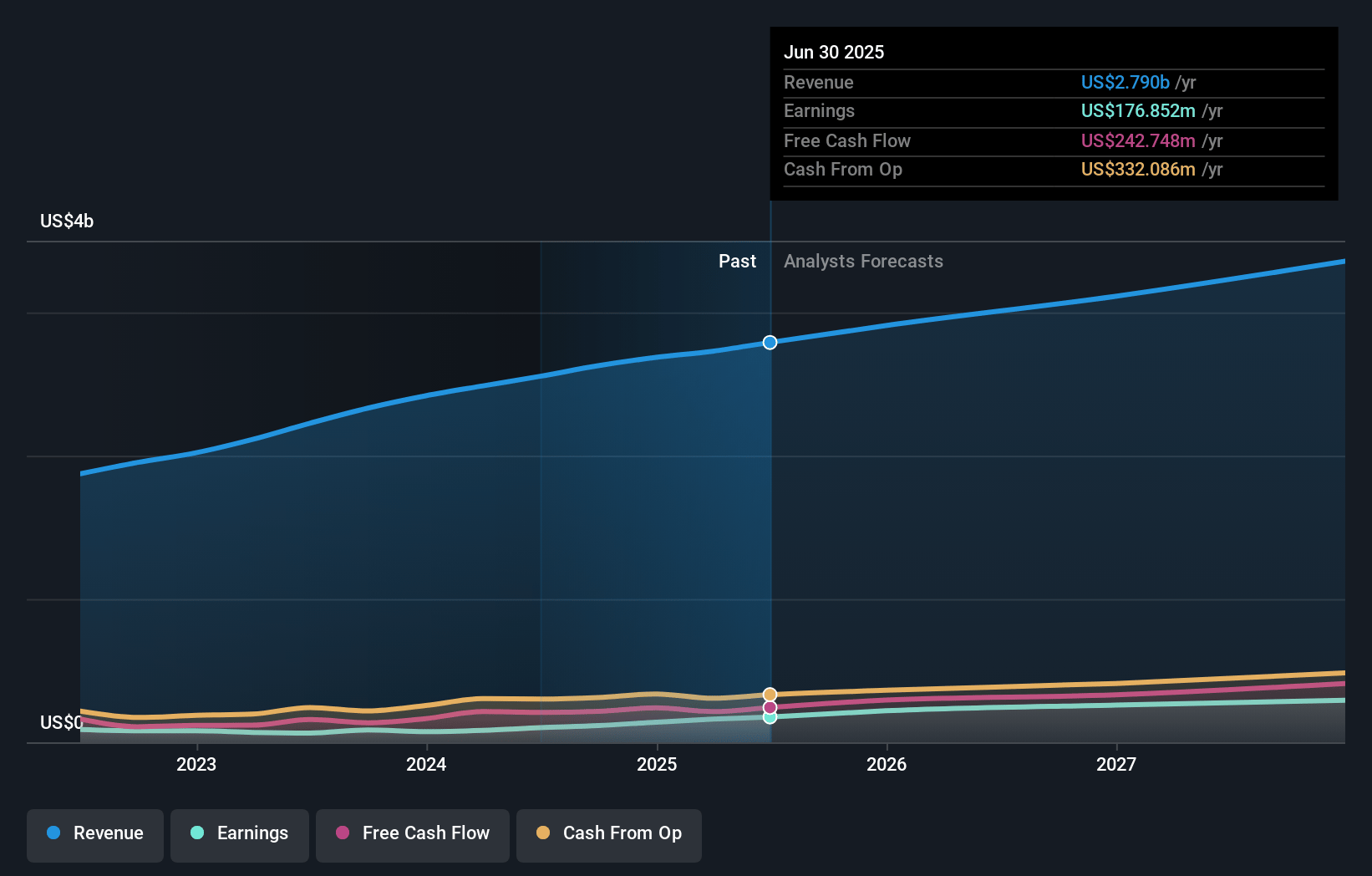

Bright Horizons Family Solutions Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Bright Horizons Family Solutions's revenue will grow by 7.9% annually over the next 3 years.

- Analysts assume that profit margins will increase from 4.4% today to 9.8% in 3 years time.

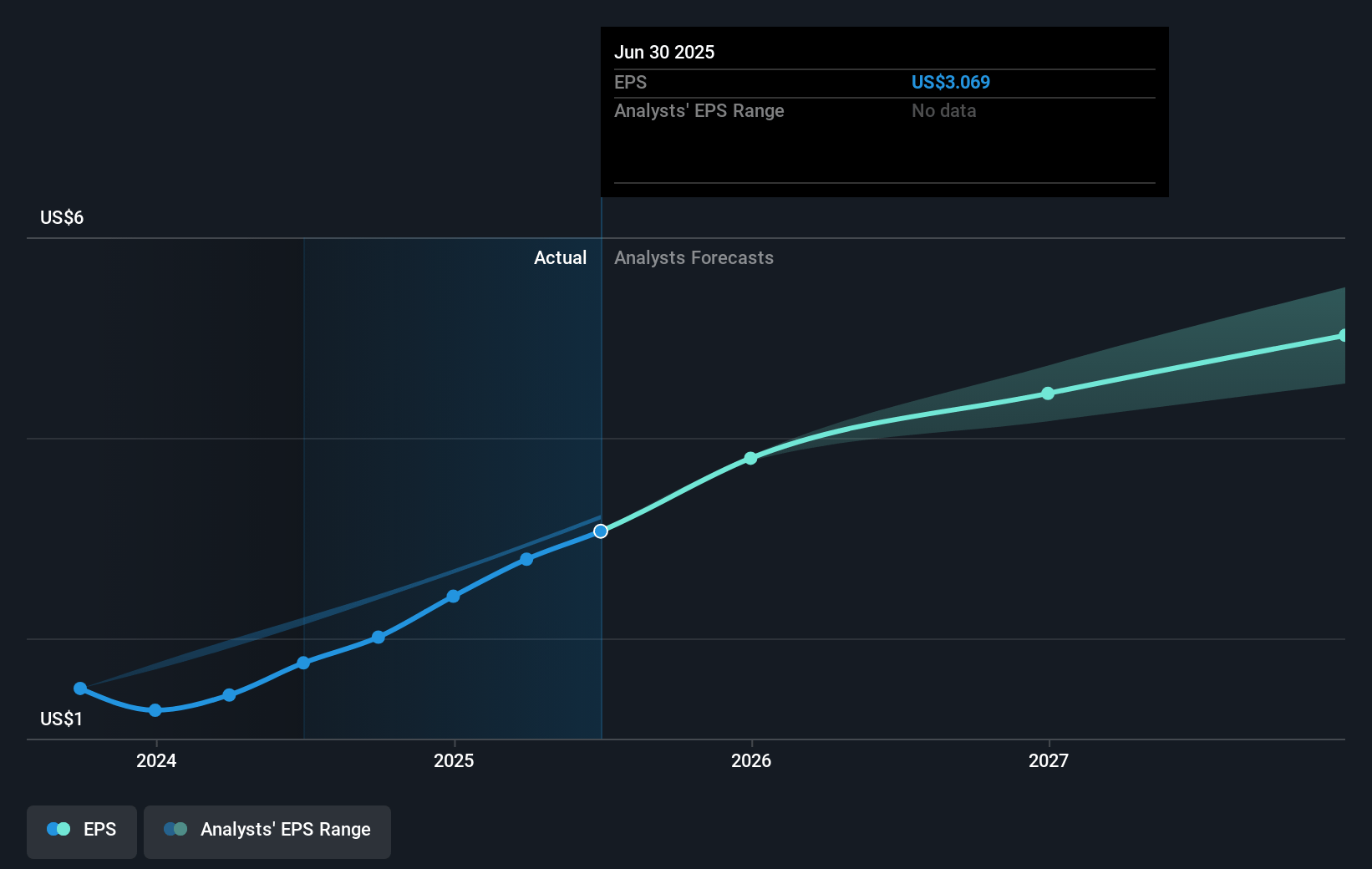

- Analysts expect earnings to reach $323.6 million (and earnings per share of $5.06) by about January 2028, up from $116.6 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 32.1x on those 2028 earnings, down from 60.9x today. This future PE is greater than the current PE for the US Consumer Services industry at 20.7x.

- Analysts expect the number of shares outstanding to grow by 3.23% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.79%, as per the Simply Wall St company report.

Bright Horizons Family Solutions Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The low single-digit enrollment growth and occupancy rates in the low 60s suggest a slow recovery in full-service child care centers, which could limit revenue growth potential.

- The U.K. operations, while improving, continue to face challenges and lag behind pre-pandemic performance levels, potentially impacting net margins due to ongoing operational inefficiencies.

- The muted participant growth in the Education Advisory segment, specifically EdAssist, indicates challenges in revitalizing this part of the business, potentially affecting overall earnings growth.

- Continued reliance on pricing increases to drive revenue growth may face limitations if inflation and wage pressures taper, impacting future profitability and net margins.

- The closure of centers, including up to 50 globally in 2024 (with a significant portion in the U.K.), reflects ongoing struggles with underperforming centers that could negatively impact overall operational efficiency and earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $133.31 for Bright Horizons Family Solutions based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $160.0, and the most bearish reporting a price target of just $102.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $3.3 billion, earnings will come to $323.6 million, and it would be trading on a PE ratio of 32.1x, assuming you use a discount rate of 6.8%.

- Given the current share price of $122.01, the analyst's price target of $133.31 is 8.5% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives