Last Update07 May 25Fair value Decreased 0.82%

Key Takeaways

- Strong client retention and new client wins are expected to drive stable revenue growth and net new business expansion.

- AI-driven supply chain efficiencies and strategic integrations aim to improve operational costs and enhance margins.

- Macroeconomic and external uncertainties, including tariffs and currency fluctuations, pose risks to Aramark's cost structure, revenue growth, and international financial stability.

Catalysts

About Aramark- Provides food and facilities services to education, healthcare, business and industry, sports, leisure, and corrections clients in the United States and internationally.

- Aramark's strong client retention rate of above 98% could lead to stable and potentially increased revenue. The high retention rate indicates consistent client satisfaction and reduces the risk of revenue loss from existing contracts.

- The company's ability to generate significant new client wins, totaling $760 million fiscal year-to-date, is expected to boost net new business growth by 4% to 5% for fiscal '25. This expansion is likely to drive overall revenue growth in the coming quarters.

- Aramark's focus on leveraging AI-driven technology for supply chain efficiencies and purchasing compliance is expected to result in improved operational cost management. These efficiencies are likely to enhance net margins by reducing costs and optimizing resource allocation.

- The integration of Quantum into Avendra International presents opportunities for procurement synergies and significant growth. These synergies could lead to improved margins through better purchasing power and cost savings.

- Aramark's capital allocation strategies, including share repurchases and extending debt maturities to 2030 and beyond, are expected to enhance shareholder value and provide financial flexibility. This could potentially lead to improved earnings per share (EPS) over time as the cost of capital is optimized and shares outstanding are reduced.

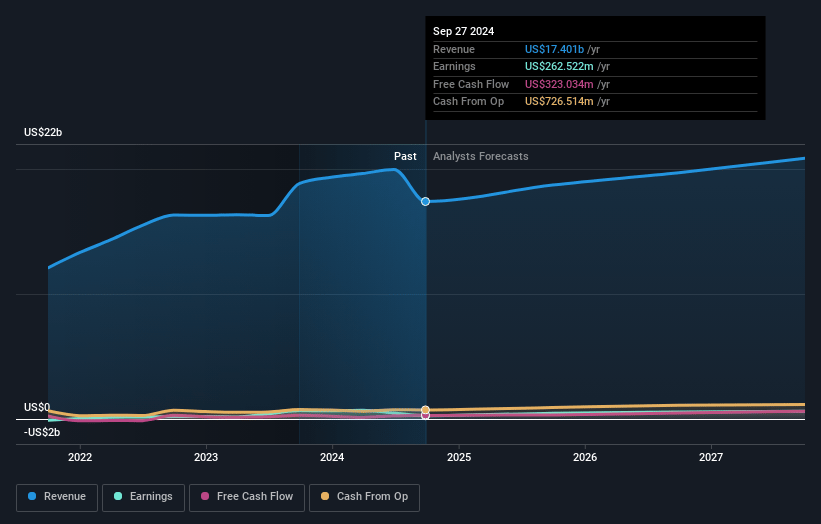

Aramark Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Aramark's revenue will grow by 7.0% annually over the next 3 years.

- Analysts assume that profit margins will increase from 2.0% today to 3.3% in 3 years time.

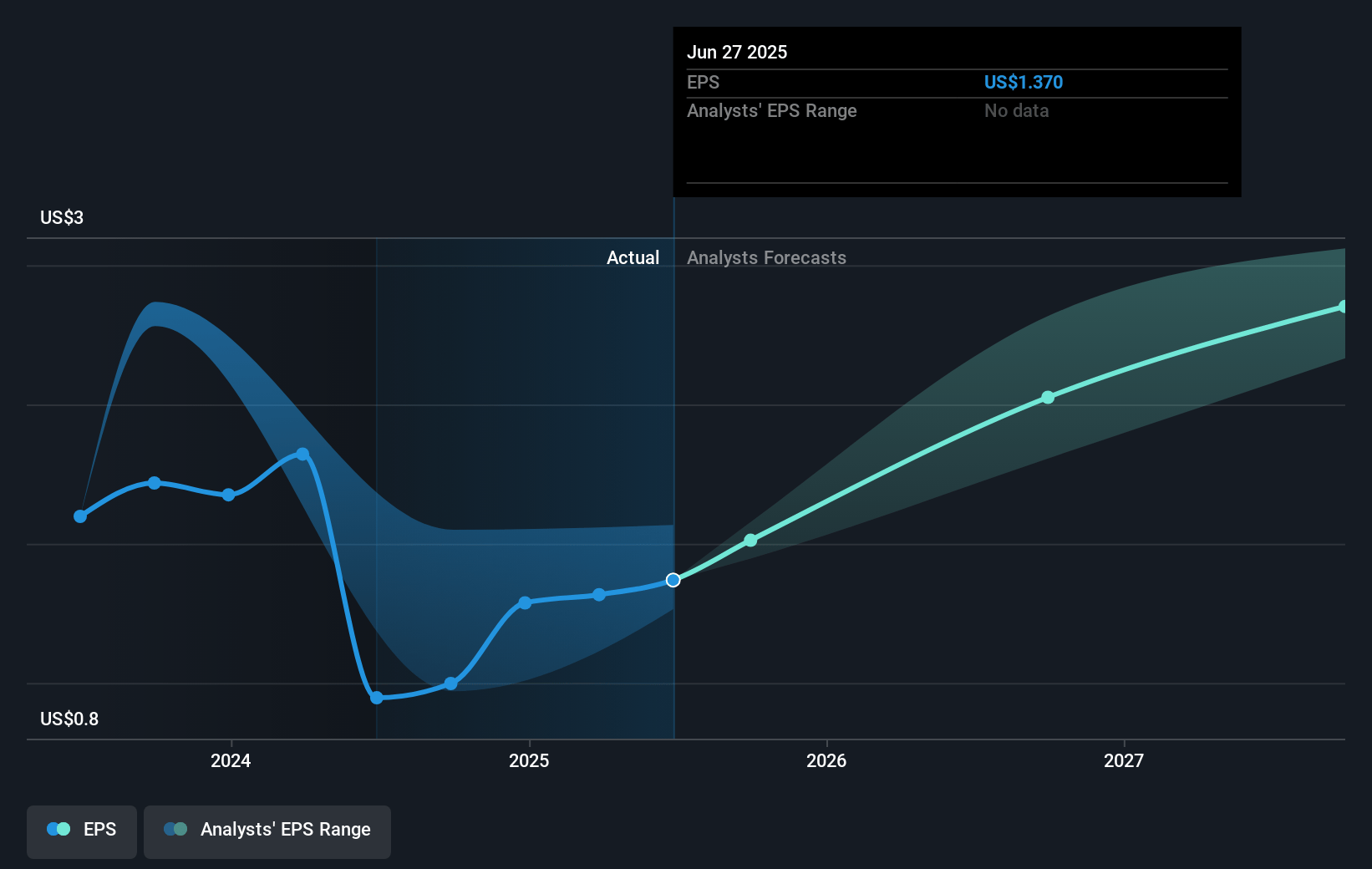

- Analysts expect earnings to reach $713.9 million (and earnings per share of $2.31) by about May 2028, up from $348.0 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 21.8x on those 2028 earnings, down from 28.7x today. This future PE is lower than the current PE for the US Hospitality industry at 21.9x.

- Analysts expect the number of shares outstanding to grow by 0.69% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.31%, as per the Simply Wall St company report.

Aramark Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Recent U.S. tariff activity has introduced uncertainty related to pricing levels and inflation expectations, which could impact Aramark's cost structure and consequently its net margins.

- Temporary factors such as weather-related client site closures in the U.S. Southeast impacted revenue growth, raising concerns about unpredictability in revenue generation.

- The exit of certain facilities accounts affected organic revenue growth, highlighting potential challenges in client retention or market share which could reduce future revenue streams.

- The impact of currency fluctuations, as noted in the discussion on foreign exchange, remains a factor that could unpredictably affect Aramark's international earnings and financial stability.

- Despite a strong new business pipeline, macroeconomic issues, such as potential education funding cuts or healthcare subsidy reductions, could affect client budgets and willingness to spend, potentially impacting revenue growth.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $44.179 for Aramark based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $49.0, and the most bearish reporting a price target of just $40.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $21.6 billion, earnings will come to $713.9 million, and it would be trading on a PE ratio of 21.8x, assuming you use a discount rate of 9.3%.

- Given the current share price of $37.64, the analyst price target of $44.18 is 14.8% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.