Narratives are currently in beta

Key Takeaways

- Expansion into new markets and diverse channels is poised to drive revenue growth and strengthen global presence.

- Innovative game releases and strategic geographic diversification are expected to boost future earnings and market share.

- Legal issues with the Dragon Train product and international market uncertainties pose significant risks to Light & Wonder's revenue, margins, and long-term growth stability.

Catalysts

About Light & Wonder- Operates as a cross-platform games company in the United States and internationally.

- Light & Wonder's robust content roadmap, featuring over 80 unique game titles, and its new studio in Reno are expected to drive sustained growth, impacting future revenue positively.

- The company's strategic participation in new markets, such as the Manitoba VLT market, aligns with its plan to expand across land-based, social, and iGaming channels, likely enhancing revenue growth.

- Continuous game releases and innovative product introductions, like Huff N' Puff extensions and new cabinets, are expected to maintain and increase the North American installed base, positively impacting future earnings.

- Strong performance and growth in the iGaming sector, backed by successful new game launches and adaptations of popular franchises, are anticipated to contribute to future revenue and market share growth.

- Light & Wonder's focus on diversification of its gaming operations across geographies and product lines, including new markets like the UAE and ongoing regulatory updates, is expected to increase its global scale, boosting future revenue potential.

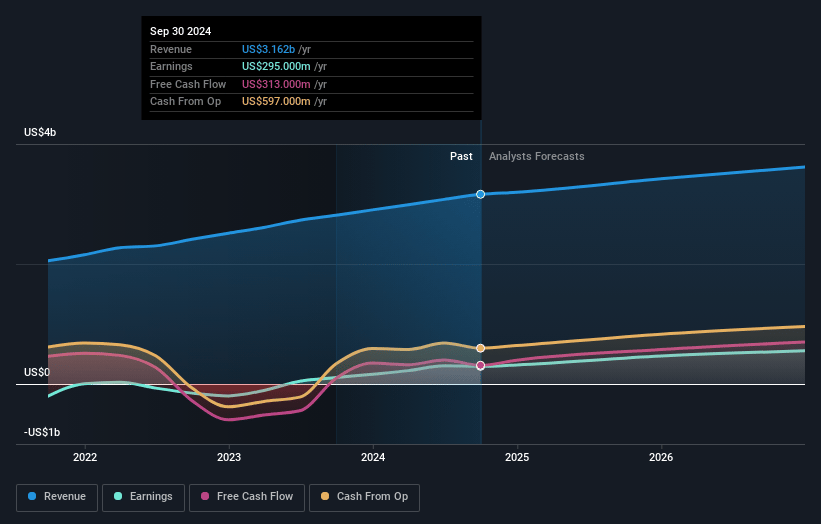

Light & Wonder Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Light & Wonder's revenue will grow by 5.1% annually over the next 3 years.

- Analysts assume that profit margins will increase from 9.3% today to 15.9% in 3 years time.

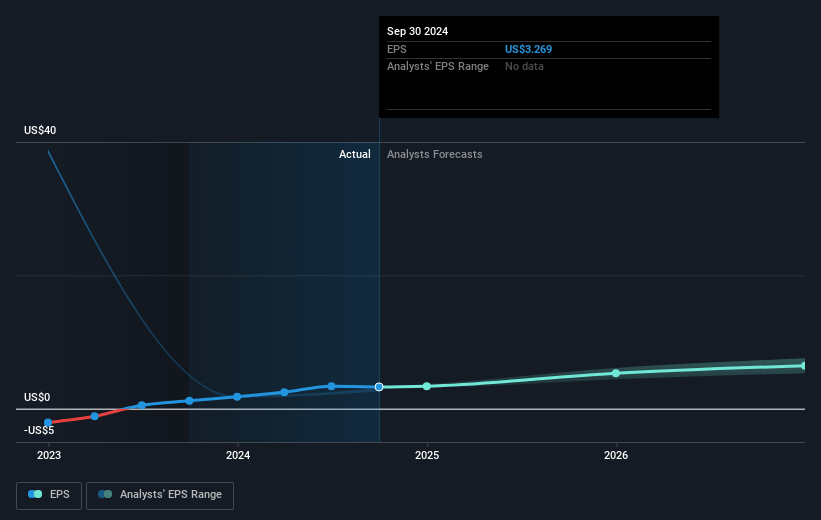

- Analysts expect earnings to reach $584.6 million (and earnings per share of $6.38) by about January 2028, up from $295.0 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $658.6 million in earnings, and the most bearish expecting $435.8 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 21.7x on those 2028 earnings, down from 25.3x today. This future PE is lower than the current PE for the US Hospitality industry at 22.4x.

- Analysts expect the number of shares outstanding to grow by 1.65% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.62%, as per the Simply Wall St company report.

Light & Wonder Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The company is facing a preliminary injunction related to its Dragon Train product, leading to potential revenue and margin impacts due to legal and conversion costs. This uncertainty surrounding legal matters may affect earnings.

- The North American market's installed base growth could be impacted by game conversions following the Dragon Train injunction, potentially affecting revenue per day and overall financial performance.

- Despite confidence in mitigating current disruptions, there's potential for further risks or slowdowns in international markets, such as Australia, which could impact future game sales and revenue growth.

- The company's gaming operations margins are vulnerable to shifts in product sales mix, which may lead to fluctuating net margins and impact overall profitability.

- A dependence on international regulatory developments and market expansion opportunities in regions such as the UAE, Macau, and the Philippines introduces uncertainties that could affect the company's long-term revenue projections and earnings stability.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $108.83 for Light & Wonder based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $144.0, and the most bearish reporting a price target of just $76.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $3.7 billion, earnings will come to $584.6 million, and it would be trading on a PE ratio of 21.7x, assuming you use a discount rate of 8.6%.

- Given the current share price of $85.63, the analyst's price target of $108.83 is 21.3% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives