Key Takeaways

- Champion Homes' digital direct-to-consumer strategy and successful Regional Homes integration enhance customer engagement and operational efficiencies.

- Anticipated demand in hurricane-hit areas and Champion Financing's new options drive sales growth and future earnings potential.

- Economic and environmental challenges, combined with acquisition-related costs and input price rises, threaten Champion Homes' revenue and margins in the near term.

Catalysts

About Champion Homes- Engages in the production and sale of factory-built housing in North America.

- Champion Homes is enhancing its digital direct-to-consumer strategy, which is expected to drive future revenue growth by expanding their market reach and improving customer engagement.

- The successful integration of the Regional Homes acquisition has led to the upper limit of synergy targets being achieved earlier than expected, likely improving net margins due to enhanced operational efficiencies.

- Champion Financing has gained significant momentum through new financing options, which could improve future earnings by attracting more customers to purchase homes, thereby increasing sales volume.

- Anticipated increased demand in regions affected by hurricanes may boost revenue as the company plays a crucial role in rebuilding efforts, leveraging the destruction of homes to drive sales.

- Strong cash position and share repurchase initiatives imply confidence in continued cash flow generation, potentially boosting EPS through reduced share count in the future.

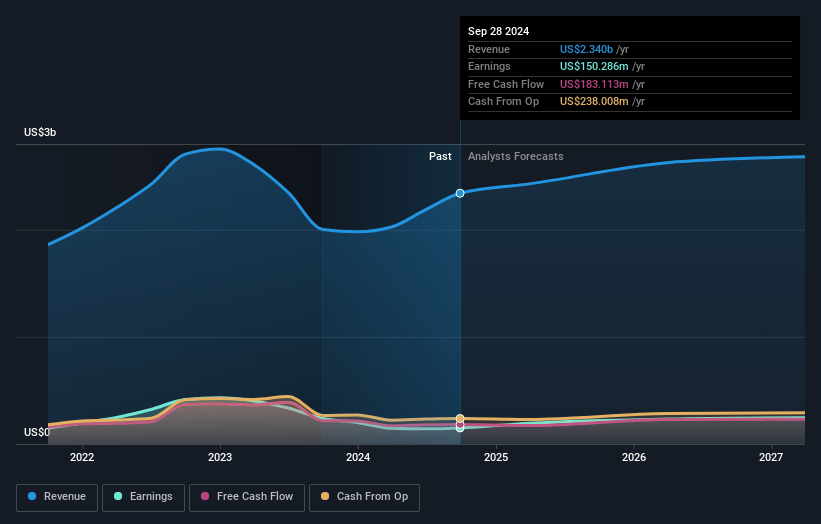

Champion Homes Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Champion Homes's revenue will grow by 7.0% annually over the next 3 years.

- Analysts assume that profit margins will increase from 6.4% today to 10.0% in 3 years time.

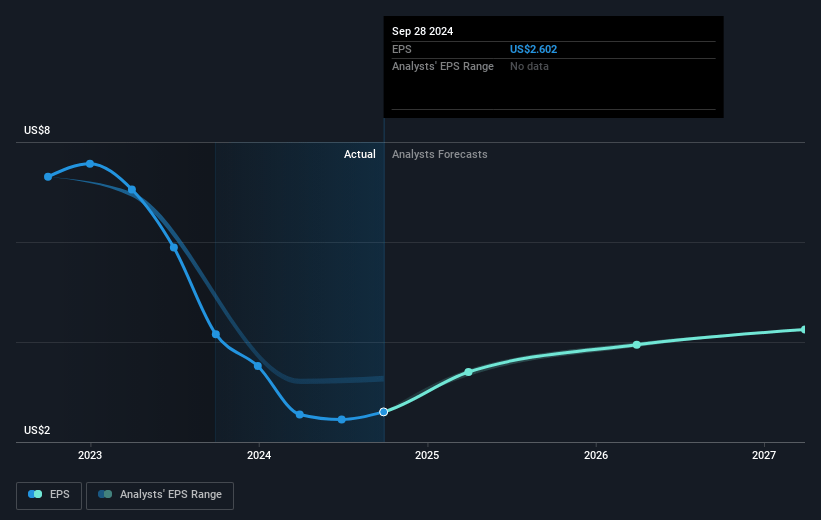

- Analysts expect earnings to reach $287.5 million (and earnings per share of $4.25) by about January 2028, up from $150.3 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 27.5x on those 2028 earnings, down from 34.5x today. This future PE is greater than the current PE for the US Consumer Durables industry at 11.3x.

- Analysts expect the number of shares outstanding to grow by 5.65% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.8%, as per the Simply Wall St company report.

Champion Homes Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The impact of hurricanes on Champion Homes’ operations, specifically due to power outages and production delays, is expected to cause timing delays in order fulfillment, potentially reducing revenue in the near term.

- The softening in order rates due to consumer hesitation ahead of the presidential election and slower winter selling season may lead to decreased revenue and backlog.

- The company faces economic uncertainty and higher interest rates in key Canadian markets, leading to reduced sales and affecting overall revenue and net margins.

- There is a risk of increased SG&A due to the recent acquisition, which could pressure net margins if costs exceed revenue growth.

- Champion Homes anticipates some margin pressures due to potential increases in input costs, which could impact gross profit margins if cost management strategies do not offset these rises.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $94.17 for Champion Homes based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $2.9 billion, earnings will come to $287.5 million, and it would be trading on a PE ratio of 27.5x, assuming you use a discount rate of 7.8%.

- Given the current share price of $90.43, the analyst's price target of $94.17 is 4.0% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives