Key Takeaways

- Expansion in Asia and direct-to-consumer focus are boosting growth, geographic diversification, margins, and operating leverage.

- Digital innovation, product elevation, and sustainability efforts are enhancing brand loyalty, pricing power, and long-term profitability.

- Heavy reliance on traditional wholesale channels, underinvestment in digital, and limited sustainability initiatives threaten future relevance, margins, and growth amid evolving consumer and regulatory pressures.

Catalysts

About Ralph Lauren- Designs, markets, and distributes lifestyle products in North America, Europe, Asia, and internationally.

- Ralph Lauren's continued expansion and strong sales growth in Asia, especially China and broader Southeast Asia, positions the brand to benefit from a rising middle class seeking aspirational and premium brands, which will drive sustained revenue growth and increase geographic diversification.

- The company's accelerated shift toward direct-to-consumer channels, both physical and digital, with double-digit comps and new store openings across key global cities, is resulting in higher gross margins and improved operating leverage, boosting both top-line growth and net margin expansion.

- Strategic investment in digital capabilities—including AI-powered predictive buying, enhanced digital customer journeys, and omnichannel experiences—enables more efficient inventory management, higher full-price sell-throughs, and more personalized marketing, which is likely to expand gross margins and profitability over time.

- Ralph Lauren’s ongoing focus on product elevation, including brand premiumization, expansion in high-growth categories like women’s apparel and handbags, and high-impact cultural and celebrity marketing activations, supports stronger pricing power, higher average selling prices, and market share gains, driving both revenue and net earnings upward.

- Demonstrated commitment to sustainability, brand purpose, and community engagement resonates with younger, more socially conscious consumer cohorts, strengthening long-term brand loyalty and positioning the company to capture incremental market share as consumer preferences shift, ultimately improving both revenue growth and customer lifetime value.

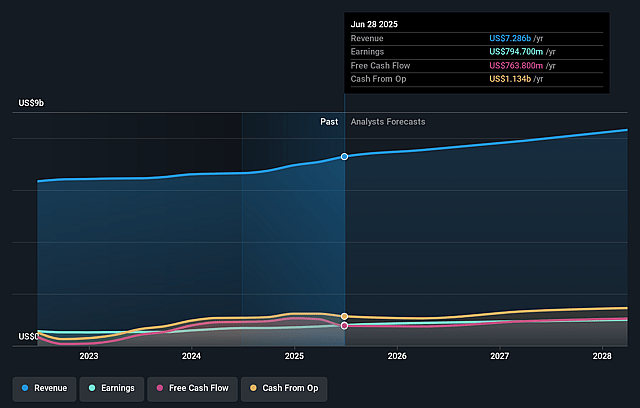

Ralph Lauren Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more optimistic perspective on Ralph Lauren compared to the consensus, based on a Fair Value that aligns with the bullish cohort of analysts.

- The bullish analysts are assuming Ralph Lauren's revenue will grow by 6.3% annually over the next 3 years.

- The bullish analysts assume that profit margins will increase from 10.5% today to 12.3% in 3 years time.

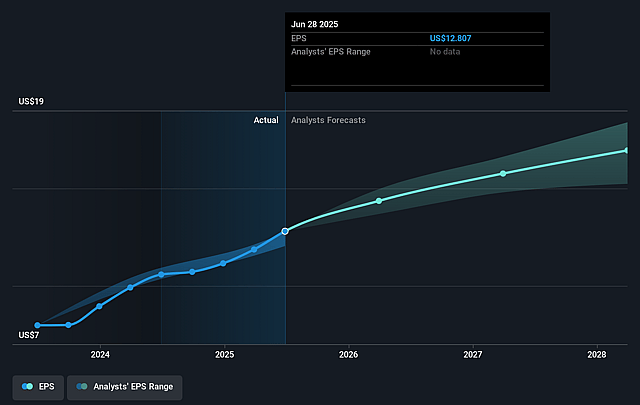

- The bullish analysts expect earnings to reach $1.0 billion (and earnings per share of $18.33) by about July 2028, up from $742.9 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bullish analyst cohort, the company would need to trade at a PE ratio of 25.6x on those 2028 earnings, up from 23.5x today. This future PE is greater than the current PE for the US Luxury industry at 16.3x.

- Analysts expect the number of shares outstanding to decline by 2.61% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.24%, as per the Simply Wall St company report.

Ralph Lauren Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Ralph Lauren’s core business relies heavily on premium and accessible luxury apparel, which faces long-term pressure from secular shifts toward experiential spending among younger demographics, potentially resulting in slower revenue growth and declining relevance with strategic consumer cohorts.

- The company continues to rely meaningfully on wholesale distribution and traditional department store partnerships, a channel under structural threat from declining foot traffic and growing market share of direct-to-consumer and digital-native brands, creating risks to future revenues and operating margins as the wholesale channel contracts.

- While leadership touts progress in digital and AI investments, there remains the risk that Ralph Lauren is underinvesting relative to more agile fast fashion and luxury competitors, which could result in ongoing share loss, margin compression, and an inability to capture e-commerce growth over the long term.

- The text reflects a strong focus on product, marketing, and city-based expansion, but there is little evidence of robust action on sustainability or ethical sourcing initiatives; increasing consumer and regulatory scrutiny in this area could drive higher compliance and supply chain costs, erode brand equity, and negatively impact net margins.

- Persistent global economic inequality and the shrinking aspirational middle-class threaten the long-term growth of Ralph Lauren’s accessible luxury positioning; this dynamic could shrink the potential customer base, making it harder to grow revenues and achieve earnings expansion in a fragmenting socioeconomic environment.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bullish price target for Ralph Lauren is $384.0, which is the highest price target estimate amongst analysts. This valuation is based on what can be assumed as the expectations of Ralph Lauren's future earnings growth, profit margins and other risk factors from analysts on the bullish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $384.0, and the most bearish reporting a price target of just $175.0.

- In order for you to agree with the bullish analysts, you'd need to believe that by 2028, revenues will be $8.5 billion, earnings will come to $1.0 billion, and it would be trading on a PE ratio of 25.6x, assuming you use a discount rate of 8.2%.

- Given the current share price of $288.31, the bullish analyst price target of $384.0 is 24.9% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystHighTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystHighTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystHighTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.