Key Takeaways

- Improving housing demand, favorable tariffs, and a focus on premium products are boosting Mohawk’s pricing power and potential for higher profitability as conditions recover.

- Strategic investments in automation, cost reduction, and geographic expansion are diversifying revenue streams and supporting long-term earnings stability.

- Weak housing demand, volatile input costs, and overcapacity threaten profitability, while mitigation strategies depend on a strong rebound in consumer spending and top-line growth.

Catalysts

About Mohawk Industries- Designs, manufactures, sources, distributes, and markets flooring products for residential and commercial remodeling, and new construction channels in the United States, Europe, Latin America, and internationally.

- The rise in housing inventory, signs of consumers re-entering the real estate market after years of deferred purchases, and expectations of Fed/ECB rate cuts indicate that pent-up demand for remodeling and new housing could convert to stronger flooring volumes as macro conditions improve, supporting a growth rebound in revenue.

- Mohawk’s domestic manufacturing scale allows the company to benefit from recently implemented U.S. tariffs on Chinese imports, gaining share in key segments (like LVT) while offsetting cost increases with price actions—positioning for improved net margins and relative earnings as competitors are forced to raise prices.

- The company is actively investing in cost reduction, automation, and supply chain optimization—including more efficient manufacturing processes and restructuring actions—which are targeted to generate at least $100 million annual savings, potentially expanding operating margins and stabilizing long-term earnings.

- Mohawk's increased focus on premium products, innovation in premium laminate and luxury vinyl, and expansion into higher-value commercial channels are elevating product mix and pricing power, which should lift average selling prices, enhance gross margin, and drive higher profitability per unit as the market recovers.

- Ongoing investment in geographic expansion (especially in Europe and South America), new product launches tailored for local markets, and increased export activity are diversifying revenue streams and reducing risk, positioning Mohawk for revenue growth and earnings resilience as global housing demand trends upward over the long term.

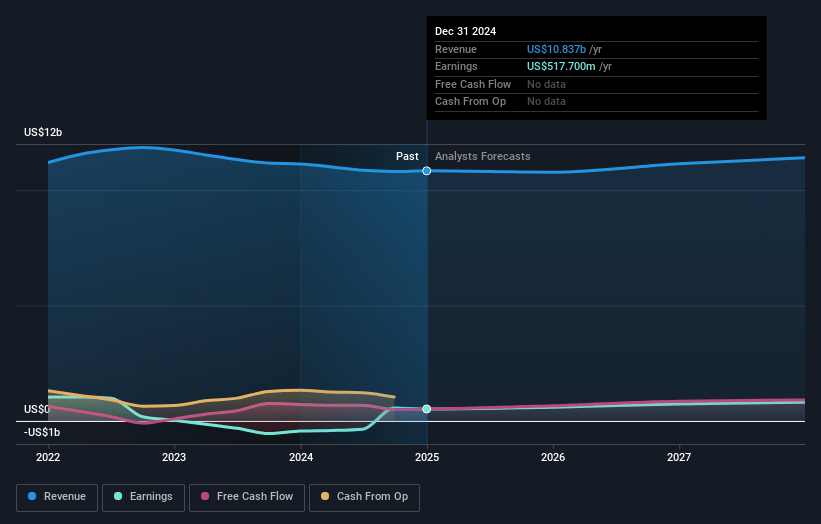

Mohawk Industries Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Mohawk Industries's revenue will grow by 2.3% annually over the next 3 years.

- Analysts assume that profit margins will increase from 4.5% today to 7.0% in 3 years time.

- Analysts expect earnings to reach $804.7 million (and earnings per share of $13.32) by about July 2028, up from $485.3 million today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as $713.6 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 12.2x on those 2028 earnings, down from 13.9x today. This future PE is greater than the current PE for the US Consumer Durables industry at 9.6x.

- Analysts expect the number of shares outstanding to decline by 0.94% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.58%, as per the Simply Wall St company report.

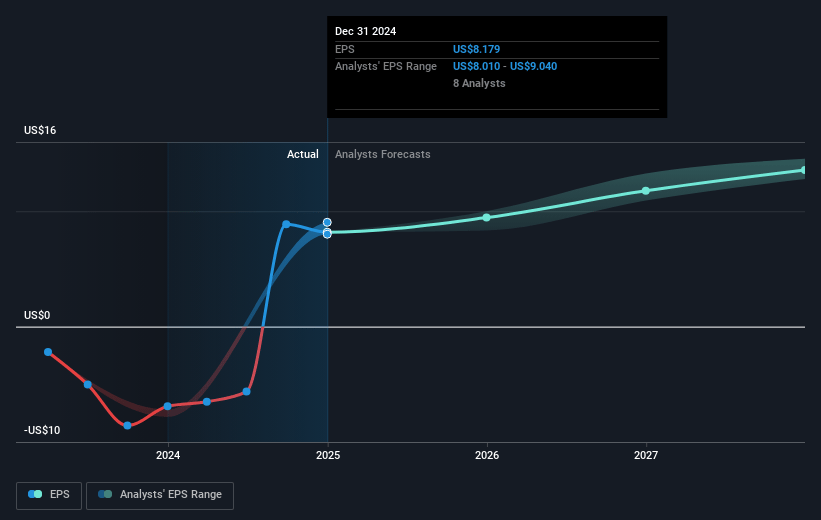

Mohawk Industries Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Prolonged weakness in residential remodeling and new housing activity, driven by low consumer confidence, high interest rates, and economic uncertainties in both the US and Europe, poses a risk to sustained revenue growth, especially if housing cycles do not rebound as expected.

- Ongoing pricing pressure and excess industry capacity, combined with promotional environments and subdued demand, could constrain Mohawk’s ability to pass on input cost increases—such as tariffs and energy inflation—thereby compressing net margins and earnings.

- Heightened exposure to volatile input costs (tariffs, energy, labor, and raw materials) creates a continued risk to gross margins, particularly if inflation persists or if supply chain adaptations prove costlier or slower than anticipated.

- Increased inventory levels, especially of imported goods in anticipation of tariff changes, elevate the risk of working capital burdens and potential write-downs should demand remain weak, negatively impacting free cash flow and profitability.

- While Mohawk is seeking to mitigate tariff exposure through domestic production and restructuring, its heavy capital expenditures and restructuring initiatives may only yield expected savings if top-line demand improves; otherwise, underutilized capacity and high fixed costs could pressure returns on assets and overall earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $127.842 for Mohawk Industries based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $150.0, and the most bearish reporting a price target of just $111.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $11.4 billion, earnings will come to $804.7 million, and it would be trading on a PE ratio of 12.2x, assuming you use a discount rate of 8.6%.

- Given the current share price of $107.81, the analyst price target of $127.84 is 15.7% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.