Key Takeaways

- Challenging macroeconomic conditions and high interest rates are reducing housing demand and impacting revenue growth.

- Increased sales incentives to address affordability concerns are expected to compress margins and net income.

- Lennar's asset-light model, strategic acquisitions, and strong cash flow focus enhance profitability, market reach, and shareholder value while ensuring stability amidst market fluctuations.

Catalysts

About Lennar- Operates as a homebuilder primarily under the Lennar brand in the United States.

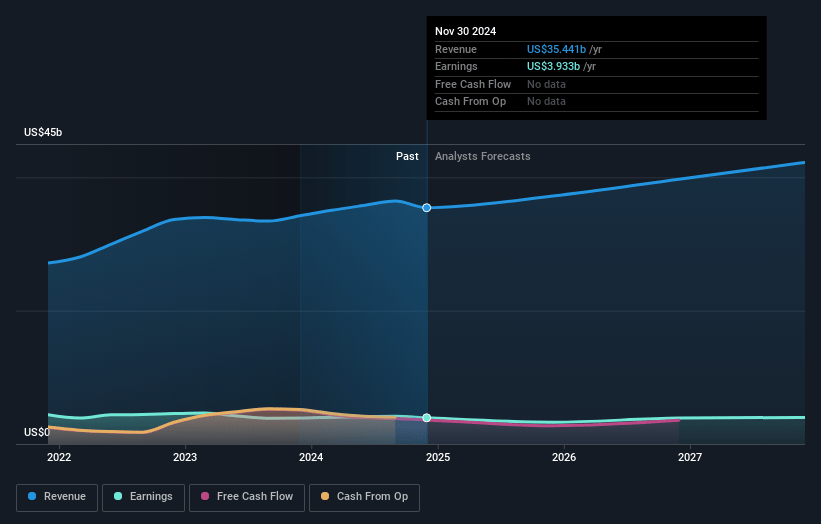

- Lennar is facing a challenging macroeconomic environment with persistently high mortgage interest rates, leading to a decline in actionable demand in the housing market. This is expected to impact revenue growth as affordability limits the potential for increased sales volumes.

- The company anticipates ongoing margin pressure due to increased sales incentives of approximately 13% to counteract affordability issues. This is significantly higher than the historical norm of 5% to 6%, which indicates potential compression of net margins in the near term.

- Lennar's transition to an asset-light, land-light model, while strategically beneficial, involves risks associated with the timing of land acquisition and development. Any misalignment could lead to inefficiencies, potentially affecting earnings if the current market conditions persist longer than expected.

- Consumer confidence has been wavering, restricting their ability and desire to purchase homes. With high personal debt levels further impeding mortgage access, near-term earnings might come under pressure as the urgency to transact remains low.

- Despite strategic shifts, Lennar's guidance projects an 18% gross margin for Q2 2025, indicating ongoing reduced profitability. If market conditions do not stabilize as anticipated, this could put further strain on net income and overall financial performance.

Lennar Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more pessimistic perspective on Lennar compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming Lennar's revenue will decrease by 0.0% annually over the next 3 years.

- The bearish analysts assume that profit margins will shrink from 10.3% today to 6.2% in 3 years time.

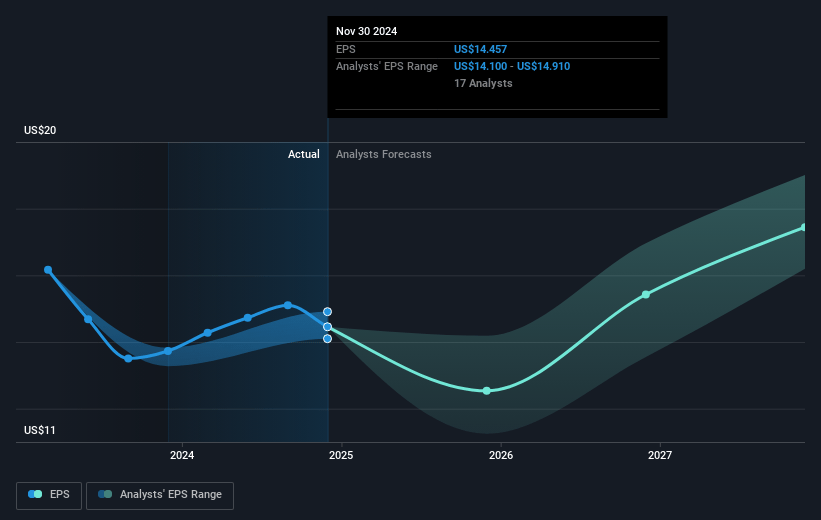

- The bearish analysts expect earnings to reach $2.2 billion (and earnings per share of $14.07) by about April 2028, down from $3.7 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 14.6x on those 2028 earnings, up from 7.3x today. This future PE is greater than the current PE for the US Consumer Durables industry at 8.0x.

- Analysts expect the number of shares outstanding to decline by 3.94% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.07%, as per the Simply Wall St company report.

Lennar Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Lennar has adopted an asset-light and land-light business model, which can lead to improved cash flows and a more efficient use of capital, potentially enhancing net margins and overall profitability.

- The company's strategic focus on delivering consistent volume and growth could stabilize Lennar’s revenue, even in challenging market conditions.

- Lennar's ability to maintain steady production and sales volume, even amidst market fluctuations, may lead to improved earnings and a more stable financial outlook.

- Lennar has strategically completed acquisitions, such as the Rausch Coleman acquisition, which could expand their market reach and increase overall revenue.

- The company's emphasis on maintaining a strong balance sheet with substantial cash flows allows for potential stock buybacks and dividends, which can enhance shareholder value and support earnings per share growth.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bearish price target for Lennar is $110.0, which represents the lowest price target estimate amongst analysts. This valuation is based on what can be assumed as the expectations of Lennar's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $200.0, and the most bearish reporting a price target of just $110.0.

- In order for you to agree with the bearish analysts, you'd need to believe that by 2028, revenues will be $35.7 billion, earnings will come to $2.2 billion, and it would be trading on a PE ratio of 14.6x, assuming you use a discount rate of 8.1%.

- Given the current share price of $102.76, the bearish analyst price target of $110.0 is 6.6% higher. The relatively low difference between the current share price and the analyst bearish price target indicates that the bearish analysts believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is an employee of Simply Wall St, but has written this narrative in their capacity as an individual investor. AnalystLowTarget holds no position in NYSE:LEN. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. This narrative is general in nature and explores scenarios and estimates created by the author. The narrative does not reflect the opinions of Simply Wall St, and the views expressed are the opinion of the author alone, acting on their own behalf. These scenarios are not indicative of the company's future performance and are exploratory in the ideas they cover. The fair value estimate's are estimations only, and does not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that the author's analysis may not factor in the latest price-sensitive company announcements or qualitative material.