Key Takeaways

- Strategic land ownership and self-development capability enable cost control and may improve future gross margins and earnings, with expansion in high-demand markets driving growth.

- Maintaining low cancellation rates and expanding affordable housing brands like Trophy Signature Homes could sustain strong revenue, supported by financial flexibility for strategic growth.

- Rising mortgage rates and higher development spending could strain affordability and profitability, with potential delays in revenue growth and cash flow challenges.

Catalysts

About Green Brick Partners- Operates as a homebuilding and land development company in the Southeast and Central United States.

- Green Brick Partners is set to benefit from its strategic land inventory, with an almost eightfold increase in lots since 2015. Owning 86% of its land and self-developing 95% of its lots allows the company to control costs and timelines, likely positively impacting future gross margins and earnings.

- The company’s expansion into high-demand markets like Dallas-Fort Worth and Atlanta, as well as newer markets like Houston, positions Green Brick to capitalize on robust demographic trends and housing demand, potentially driving future revenue growth.

- Despite higher mortgage rates, Green Brick continues to maintain low cancellation rates and high sales pace per active selling community. This resilience in demand, supported by attractive incentives and a focus on entry-level and first-time move-up buyers, may support continued strong revenue and earnings performance.

- The expansion of the Trophy Signature Homes brand is expected to enhance revenue growth due to its focus on more affordable housing options, catering to a large and growing segment of homebuyers, particularly as millennials and Gen Z enter their prime home-buying years.

- Green Brick’s strong balance sheet, with a low debt-to-total-capital ratio and a new share repurchase plan, provides financial flexibility that could lead to strategic growth initiatives and shareholder value enhancement, thereby potentially boosting EPS in the future.

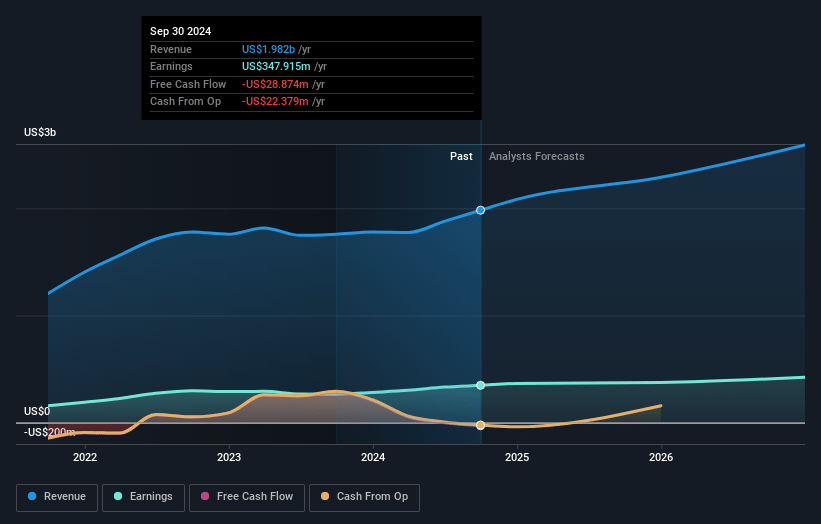

Green Brick Partners Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Green Brick Partners's revenue will grow by 4.2% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 18.0% today to 16.0% in 3 years time.

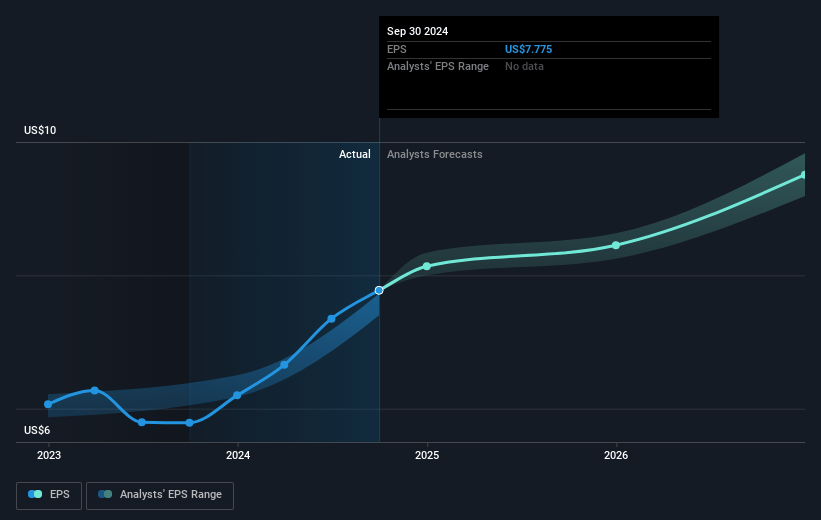

- Analysts expect earnings to reach $378.6 million (and earnings per share of $8.08) by about April 2028, down from $378.7 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 10.0x on those 2028 earnings, up from 6.8x today. This future PE is greater than the current PE for the US Consumer Durables industry at 8.9x.

- Analysts expect the number of shares outstanding to decline by 0.96% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.04%, as per the Simply Wall St company report.

Green Brick Partners Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Rising mortgage rates pose a significant risk to homebuyer affordability, particularly affecting entry-level and first-time homebuyers in more sensitive markets, potentially impacting sales volumes and revenues.

- An increase in development spending by 46% may not immediately translate to earnings growth due to the typical three-year lag from land acquisition to revenue generation, potentially affecting near-term financial performance.

- Elevated incentive levels, particularly in less desirable locations, may erode gross margins if mortgage rates remain high, impacting overall profitability.

- Reduced backlog revenue by 10.7% year-over-year could signal a potential slowdown in future sales growth and revenue recognition.

- Land acquisition costs remaining sticky in a competitive market could lead to increased capital spending with uncertain immediate returns, affecting cash flow and net margins.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $70.0 for Green Brick Partners based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $2.4 billion, earnings will come to $378.6 million, and it would be trading on a PE ratio of 10.0x, assuming you use a discount rate of 8.0%.

- Given the current share price of $58.22, the analyst price target of $70.0 is 16.8% higher. Despite analysts expecting the underlying buisness to decline, they seem to believe it's more valuable than what the market thinks.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.