Key Takeaways

- Strategic portfolio management and international expansion are set to enhance JAKKS Pacific's revenue through diverse offerings and increased market share.

- Strong financial management and exclusive retailer partnerships aim to boost earnings and support growth through efficient turnover and strategic initiatives.

- Challenges in international markets and retailer credit issues, alongside dependency on unpredictable content-led products, threaten revenue growth and earnings stability.

Catalysts

About JAKKS Pacific- Designs, produces, markets, sells, and distributes toys and related products, electronic products, and other consumer products worldwide.

- JAKKS Pacific is prioritizing strategic portfolio management across more than 30 businesses, focusing on both property-driven and category-driven product lines, helping to sustain and potentially increase revenue through diverse market offerings.

- The company’s expansion in Latin America, coupled with improvements in product listings and supply chain logistics in Europe, is expected to drive revenue growth internationally, benefiting from increasing market share in regions with previously lower presence.

- The robust execution of new retail programs and consumer marketing strategies aims to enhance sell-through rates, particularly during the holiday season, which should positively impact revenue and margins through higher product turnover and consumer engagement.

- By maintaining a strong balance sheet with zero debt and disciplined inventory management, JAKKS can preserve cash and leverage financial strength to pursue new business opportunities and strategic initiatives, potentially increasing earnings and net margins.

- Focused investments in exclusive retailer partnerships and increased shelf space globally provide consistent selling opportunities and support top-line growth, helping to drive revenue by leveraging retailer-specific promotions and placements.

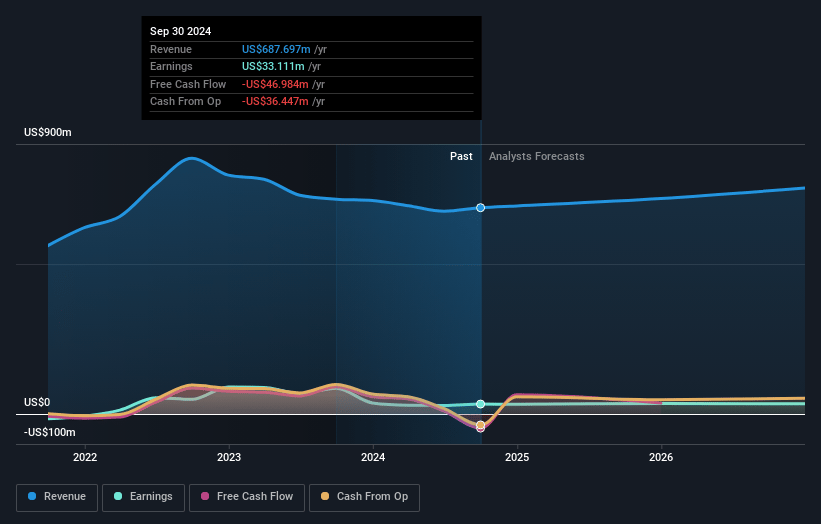

JAKKS Pacific Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming JAKKS Pacific's revenue will grow by 4.0% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 4.8% today to 4.6% in 3 years time.

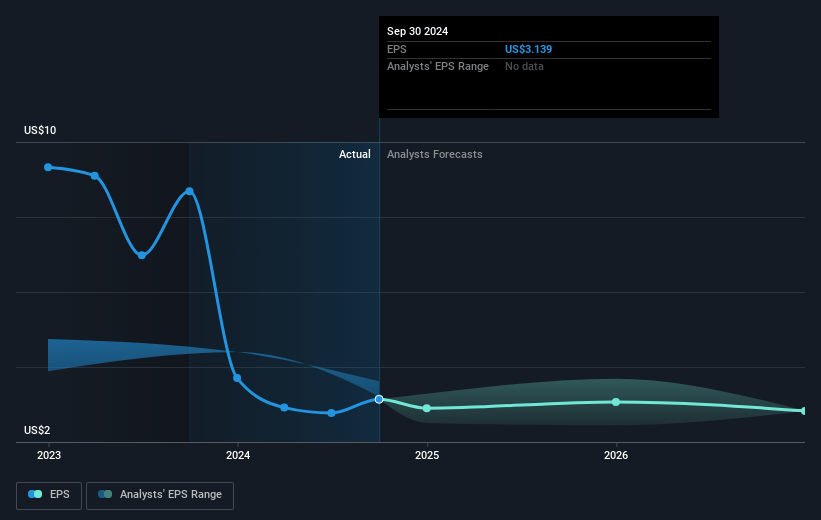

- Analysts expect earnings to reach $35.5 million (and earnings per share of $2.83) by about January 2028, up from $33.1 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 17.4x on those 2028 earnings, up from 9.8x today. This future PE is greater than the current PE for the US Leisure industry at 16.6x.

- Analysts expect the number of shares outstanding to grow by 4.53% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.8%, as per the Simply Wall St company report.

JAKKS Pacific Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The company faces challenges in international markets, particularly with declines in Europe and Asia Pacific, which could lead to reduced revenue growth in these regions.

- Retailers are actively destocking, indicating potential weakness in demand or inventory management issues, which may impact overall sales and net margins.

- There is a deteriorating creditworthiness of some retailers, with potential bankruptcies posing a risk to accounts receivables and future earnings.

- Issues with timing and trade dynamics in regions like Canada could affect shipment schedules and revenue consistency.

- The company heavily relies on content-led products, whose performance is unpredictable and dependent on the success of associated films and media, posing a risk to stable earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $42.33 for JAKKS Pacific based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $773.1 million, earnings will come to $35.5 million, and it would be trading on a PE ratio of 17.4x, assuming you use a discount rate of 6.8%.

- Given the current share price of $29.43, the analyst's price target of $42.33 is 30.5% higher. Despite analysts expecting the underlying buisness to decline, they seem to believe it's more valuable than what the market thinks.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives