Last Update 04 Jun 26

Fair value Increased 2.59%LZ: AI Reset And Key Partnership Will Drive Future Upside Potential

Analysts have modestly raised their price target on LegalZoom.com to $8.50 from $8.29, reflecting updated views on fair value, discount rate, revenue growth, profit margins, and future P/E assumptions.

What's in the News

- LegalZoom reported Q1 revenue that was 12.9% higher year on year and 2.5% above analyst expectations, with CEO Jeff Stibel pointing to a companywide reset aimed at more sustainable growth and a focus on accelerating EBITDA expansion. [Source: LegalZoom Reports Mixed Q1 Results Amid Strategic Growth Reset]

- The company issued full year revenue guidance that was the weakest among its peer group and provided next quarter guidance that was slightly below expectations, while emphasizing multi year growth priorities and potential benefits from higher organic subscription revenue. [Source: LegalZoom Reports Mixed Q1 Results Amid Strategic Growth Reset]

- LegalZoom and GoDaddy agreed a partnership that makes LegalZoom the sole legal services provider within the GoDaddy ecosystem, integrating LLC formation and compliance support directly into GoDaddy’s small business tools. [Source: Strategic Alliances]

- LegalZoom expanded its product suite with Grant Finder, an AI powered tool designed to match small businesses and nonprofits with grant opportunities, and launched the LegalZoom app in ChatGPT to guide users from an initial business idea to a tailored formation plan. [Source: Product Related Announcements]

- The company reported that its Virtual Mail service has processed 17.8 million mail items and 1.7 million checks totaling US$9.5b in deposits, alongside new AI driven features such as automated mail categorization, summaries, and a Check Separation function for depositing multiple checks from a single mail item into different accounts. [Source: Product Related Announcements]

Valuation Changes

- Fair Value: Price target fair value has risen slightly to $8.50 from $8.29.

- Discount Rate: The discount rate has moved up marginally to 7.45% from 7.39%, signaling a minor adjustment in the risk or return assumptions used in the model.

- Revenue Growth: Forecast revenue growth has been raised slightly to 6.48% from 6.33%, indicating a small uplift in expected top line expansion in dollar terms.

- Net Profit Margin: Projected profit margin is effectively unchanged, moving to 9.71% from 9.75%.

- Future P/E: The assumed future P/E multiple has risen moderately to 17.07x from 16.28x, pointing to a somewhat higher valuation multiple being applied to expected earnings.

Key Takeaways

- AI partnerships and automation are expanding LegalZoom's market reach, boosting brand visibility, operating efficiency, and supporting scalable delivery of services.

- Growth in high-margin subscription products, bundled solutions, and successful acquisitions is increasing predictable revenues, customer retention, and driving strategic investment flexibility.

- Advances in AI, increased competition, cost pressures, declining retention, and regulatory risks collectively threaten LegalZoom's growth, margins, and long-term market position.

Catalysts

About LegalZoom.com- Operates an online platform that supports the legal, compliance, and business management needs of small businesses and consumers in the United States.

- Accelerating adoption of online legal and compliance services, supported by strong partnerships with AI leaders like OpenAI and Perplexity, is rapidly expanding LegalZoom's addressable market and improving brand visibility, which is set to increase future revenue growth.

- Strong momentum in high-margin, recurring subscription offerings-especially within compliance and concierge do-it-for-me products-signals continued growth in predictable revenues and improved customer retention, directly supporting higher net margins and earnings stability.

- Enhanced automation and AI deployment throughout the business is driving operating efficiency gains and enabling scalable delivery of higher-touch services, underpinning continued EBITDA margin expansion and reduced cost structure.

- Ongoing investment in upmarket and bundled solutions, coupled with successful integration and upsell cross-sell opportunities from acquisitions like Formation Nation, is broadening LegalZoom's product suite, targeting higher-LTV customers and increasing wallet share, which will benefit both revenue and gross margins.

- Robust free cash flow generation and a strengthened balance sheet provide LegalZoom with flexibility to strategically invest in growth initiatives and pursue further M&A, supporting long-term earnings growth.

LegalZoom.com Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

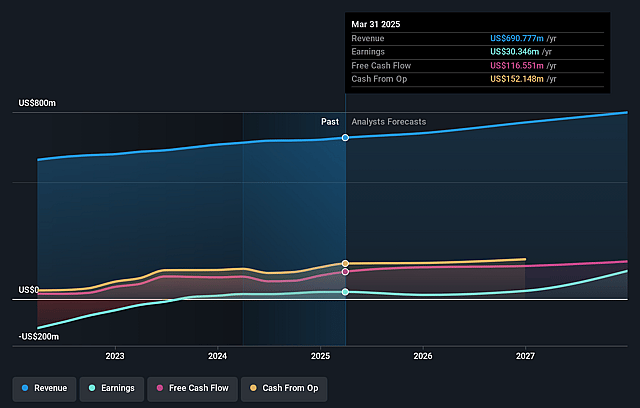

- Analysts are assuming LegalZoom.com's revenue will grow by 6.5% annually over the next 3 years.

- Analysts assume that profit margins will increase from 1.5% today to 9.7% in 3 years time.

- Analysts expect earnings to reach $91.4 million (and earnings per share of $0.37) by about June 2029, up from $11.4 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 17.1x on those 2029 earnings, down from 91.1x today. This future PE is lower than the current PE for the US Professional Services industry at 19.1x.

- Analysts expect the number of shares outstanding to decline by 4.77% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.45%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- The rapid advancement of generative AI and commoditization of legal documents could enable consumers and new competitors to easily replicate core formation and compliance services at lower costs, putting sustained downward pressure on LegalZoom's revenues and market share over the long term.

- Bundling lower-priced, lower-retention products (such as forms, eSignature, and bookkeeping) into its premium SKUs has led to a decrease in aggregate subscription retention rates (currently at 59%, down from 60%), elevating customer churn risk and threatening the predictability and growth of recurring revenues.

- Increased investment in hands-on "do-it-for-me" (DIFM) offerings and newly acquired sales teams introduces sizable cost pressures at scale, and until automation fully offsets these expenses, margin expansion and net earnings growth may be constrained.

- Intensifying price competition from both established law firms moving online and proliferating lower-cost or open-source alternatives may erode LegalZoom's brand differentiation, forcing continued sales and marketing spend, which could weigh on gross margins and profitability.

- Ongoing regulatory scrutiny and potential allegations around the unauthorized practice of law, especially as LegalZoom expands its service suite or geographic footprint, may result in costly legal defenses, regulatory restrictions, or settlements, impacting operating income and overall financial health.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $8.5 for LegalZoom.com based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $11.0, and the most bearish reporting a price target of just $6.5.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $941.2 million, earnings will come to $91.4 million, and it would be trading on a PE ratio of 17.1x, assuming you use a discount rate of 7.4%.

- Given the current share price of $6.05, the analyst price target of $8.5 is 28.8% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on LegalZoom.com?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.