Last Update 02 Apr 26

Fair value Increased 793%LNZA: Future Capital Needs And Project Execution Will Shape Balanced Outlook

Analysts have raised their price target for LanzaTech Global from $1.68 to $15.00, citing updated assumptions regarding discount rates, revenue growth, profit margins, and future P/E multiples, while also noting the company’s need to raise capital to remain viable.

Analyst Commentary

Bullish Takeaways

- Bullish analysts see the higher price target as an attempt to align with updated assumptions on revenue growth and profit margins, which, if achieved, could support a higher long term earnings profile.

- The jump in target price is described as reflecting potential upside in future P/E multiples, assuming the company can execute on its business plan and move closer to sustainable profitability.

- Some bullish views suggest that revisiting discount rates in the valuation model provides more room for upside if funding needs are addressed and project pipelines progress as planned.

- The new target also signals confidence that, with adequate capital, LanzaTech Global could better scale its platform, which would matter for both growth expectations and long term valuation.

Bearish Takeaways

- Bearish analysts stress that the company still needs to raise capital to remain viable, which introduces dilution risk and execution pressure that could weigh on the current share price.

- There is concern that the valuation case relies heavily on assumptions about future P/E multiples and margin expansion, with limited visibility on the timing or certainty of those outcomes.

- Some cautious views focus on funding risk, warning that less favorable capital market conditions or higher financing costs could constrain growth plans and challenge the raised target.

- Analysts with a more conservative stance highlight that, without clear proof of improved cash generation, the higher price target may be harder to justify on fundamentals alone.

What's in the News

- LanzaTech Global selected Saltend Chemicals Park in Humberside as the intended site for its DRAGON II project, a planned £600 million facility targeting large scale production of sustainable aviation fuel and renewable diesel. Construction is expected to start in the second half of 2027, with operations targeted for 2030 (Key Developments).

- The DRAGON projects, supported by a £6.4 million UK Department for Transport Advanced Fuels Fund grant awarded in July 2025, are planned to use LanzaJet Alcohol to Jet technology and LanzaTech gas fermentation to convert waste CO2 and green hydrogen into ethanol for Power to Liquid SAF, subject to rule changes affecting green hydrogen use (Key Developments).

- LanzaTech Global entered into subscription agreements for a private placement of 4,000,000 common shares at US$5.00 per share, for total gross proceeds of US$20,000,000, plus 510,968 bonus shares. One large investor will receive board observer rights while it maintains at least 50% of its subscribed shares (Key Developments).

- The company was awarded a contract by Spray Engineering Devices Ltd. to build an ethanol facility in Uttar Pradesh, India. The facility is expected to process up to 300 tons per day of sugarcane bagasse as part of the SED Smart Village concept and to supply sustainable fuels and chemicals, including under India’s PM JI-VAN Yojana program (Key Developments).

- LanzaTech reported successful operational results at a municipal solid waste to ethanol pilot plant in Kuji City, Japan. The 1/10th commercial scale facility, funded by a Sekisui Chemical and INCJ joint venture and Japanese government support, met guaranteed performance targets while processing mixed non recyclable waste streams (Key Developments).

Valuation Changes

- Fair Value: Target fair value has moved from $1.68 to $15.00, a very large step up that reshapes how the upside is framed.

- Discount Rate: The discount rate has fallen significantly from 10.14% to 7.12%, which generally increases the present value placed on future cash flows.

- Revenue Growth: The revenue growth assumption has shifted from 57.93% to 27.23%, indicating a more moderate long-term growth profile being used in the model.

- Net Profit Margin: The net profit margin assumption has edged up from 6.13% to 6.84%, reflecting a slightly stronger profitability outlook once the business matures.

- Future P/E: The future P/E multiple assumption has come down sharply from 44.17x to 6.57x, meaning the higher fair value is no longer relying on a very high earnings multiple.

Key Takeaways

- Transition from licensing to owning and financing projects allows LanzaTech to capture more value, driving revenues and profitability through technological advancements.

- Strong partnerships and unique agreements like those with Brookfield and ArcelorMittal bolster project execution, stability, and access to new market opportunities.

- Dependence on sublicense agreements and large-scale projects introduces revenue timing, geopolitical risks, and potential liquidity strains, affecting overall financial stability.

Catalysts

About LanzaTech Global- Operates as a nature-based carbon refining company in the United States and internationally.

- LanzaTech's shift from a licensing-only model to developing and financing its own projects aims to capture more value and control over timing, which could drive higher revenues and profitability as they gain more from the upside of their technology.

- The partnership with Brookfield Asset Management, which has committed $500 million for LanzaTech projects, reflects a strong capital backing to develop new projects, potentially boosting future earnings through increased project execution and ownership.

- The exclusivity and financing agreement for Project Drake and similar initiatives are expected to provide significant income, supporting a meaningful uplift in 2025 financial performance, positively impacting earnings and cash flow.

- The first long-term ethanol offtake agreement with ArcelorMittal enhances access to products, potentially leading to greater revenue stability and growth through CarbonSmart, and improves profit margins by enabling more substantial customer commitments.

- LanzaTech's capability to produce LanzaTech Nutritional Protein taps into the rapidly growing alternative protein market, which is expected to significantly boost revenue streams as it targets an estimated $1 trillion market opportunity.

LanzaTech Global Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming LanzaTech Global's revenue will grow by 27.2% annually over the next 3 years.

- Analysts are not forecasting that LanzaTech Global will become profitable in next 3 years. To represent the Analyst Price Target as a Future PE Valuation we will estimate LanzaTech Global's profit margin will increase from -190.2% to the average US Commercial Services industry of 6.8% in 3 years.

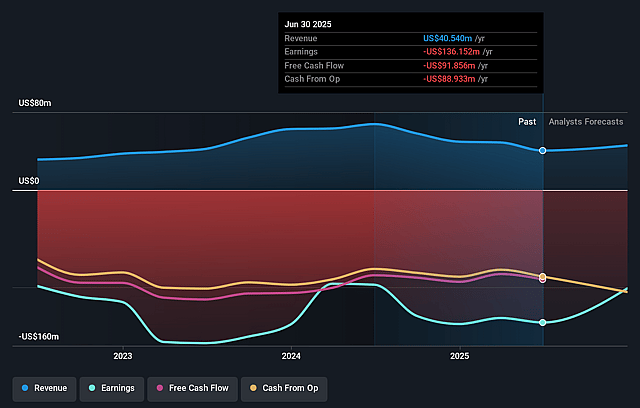

- If LanzaTech Global's profit margin were to converge on the industry average, you could expect earnings to reach $5.6 million (and earnings per share of $2.42) by about April 2029, up from -$75.9 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 7.6x on those 2029 earnings, up from -1.9x today. This future PE is lower than the current PE for the US Commercial Services industry at 22.0x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.12%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- The company's reliance on sublicensing agreements with LanzaJet creates uncertainty in revenue timing, affecting potential revenue recognition and cash flow stability.

- Low ethanol prices, particularly in the Chinese market, have reduced CarbonSmart's revenue potential, impacting overall margin and earnings.

- A shift towards developing capital-intensive projects in-house necessitates significant up-front investment which could strain liquidity and impact net margins if returns do not materialize as expected.

- Achieving financial targets is dependent on multiple large-scale infrastructure projects reaching final investment decisions on schedule, posing execution risks to projected revenues and operating income.

- The company's strategy to grow through joint venture and project developments in various global regions involves geopolitical and operational risks that could affect project delivery and financial outcomes.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $15.0 for LanzaTech Global based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $82.1 million, earnings will come to $5.6 million, and it would be trading on a PE ratio of 7.6x, assuming you use a discount rate of 7.1%.

- Given the current share price of $14.64, the analyst price target of $15.0 is 2.4% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on LanzaTech Global?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.