Key Takeaways

- Strategic growth in high-value verticals and service acquisitions is enhancing Trane Technologies' revenue and margin expansion.

- Recovery and growth in Americas transport refrigeration markets are poised to drive earnings and revenue from 2025 onward.

- Economic and policy challenges in China, volatile transport refrigeration markets, and competition in fast-growing sectors could constrain Trane Technologies' revenue and profit margins.

Catalysts

About Trane Technologies- Designs, manufactures, sells, and services of solutions for heating, ventilation, air conditioning, and custom and transport refrigeration.

- Trane Technologies' relentless investment in innovation and high ROI projects is driving strong customer demand and market outperformance, particularly in Commercial HVAC, which is expected to significantly contribute to revenue and margin expansion.

- The company's strategic focus on high-growth verticals such as data centers and education, along with a robust pipeline, is anticipated to bolster organic revenue growth and improve net margins due to higher value-added services.

- The recovery forecasted in the Americas transport refrigeration markets by the second half of 2025, followed by strong growth in 2026 and 2027, presents a catalyst for revenue growth and improved earnings.

- Investments in service business offerings, including new acquisitions like BrainBox AI, are expected to enhance capabilities in predictive maintenance and digital solutions, further driving revenue growth and margin improvement due to higher service-related profits.

- The significant backlog of $6.75 billion entering 2025, with a strong focus on applied systems offering service opportunities with high margins, suggests robust revenue visibility and expected EPS growth through sustained service-related engagements.

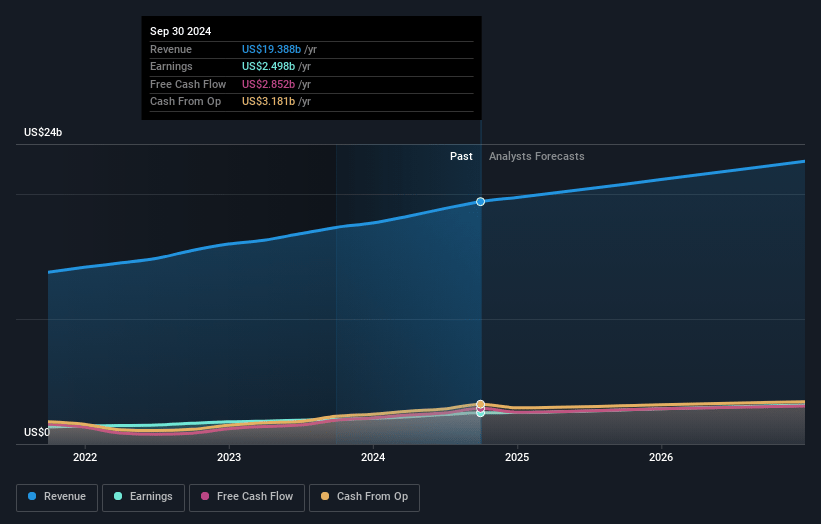

Trane Technologies Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Trane Technologies's revenue will grow by 6.9% annually over the next 3 years.

- Analysts assume that profit margins will increase from 13.1% today to 14.1% in 3 years time.

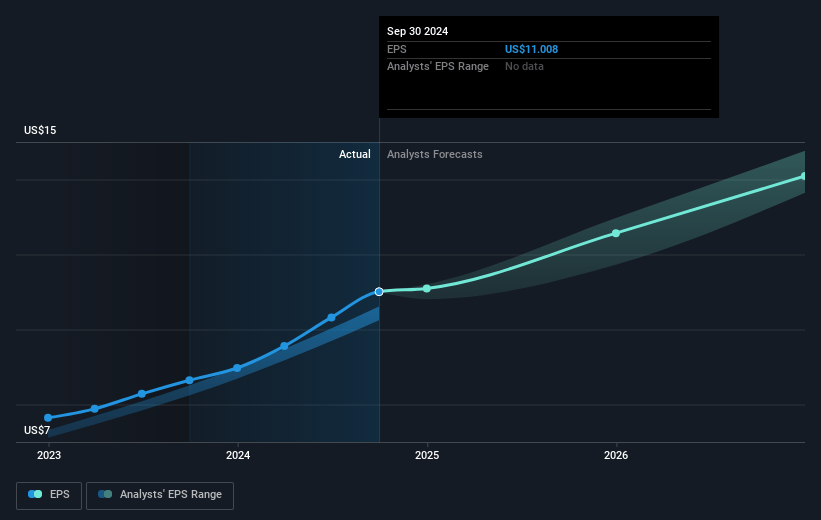

- Analysts expect earnings to reach $3.4 billion (and earnings per share of $15.43) by about March 2028, up from $2.6 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 33.0x on those 2028 earnings, up from 29.8x today. This future PE is greater than the current PE for the US Building industry at 19.2x.

- Analysts expect the number of shares outstanding to decline by 0.91% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.72%, as per the Simply Wall St company report.

Trane Technologies Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The company's performance is partly reliant on regions like China, where tightened credit policies have previously impacted results. Continued economic or policy challenges in China could negatively affect revenue and earnings.

- Despite strong past performance, the market for transport refrigeration in the Americas is volatile and expected to remain flat in 2025, which could constrain future revenue growth in this segment.

- There is uncertainty regarding market growth in residential HVAC, with only a mid-single-digit growth expectation following a prebuy event, which could impact revenue growth if the recovery is slower than anticipated.

- Currency fluctuations are projected to have a negative impact on earnings by approximately $0.20 for the year, which could adversely affect net margins and EPS.

- Elevated competition, especially in fast-growing sectors like data centers, could pressure pricing and market share, potentially affecting forecasted revenue growth and profit margins.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $403.558 for Trane Technologies based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $500.0, and the most bearish reporting a price target of just $237.34.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $24.3 billion, earnings will come to $3.4 billion, and it would be trading on a PE ratio of 33.0x, assuming you use a discount rate of 8.7%.

- Given the current share price of $344.76, the analyst price target of $403.56 is 14.6% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives