Narratives are currently in beta

Key Takeaways

- Strategic international expansion and local production efforts aim to boost revenue through increased global sales and presence.

- Investments in AI and autonomy are set to enhance efficiencies and net margins through operational improvements and advanced capabilities.

- Delays in F-35 revenue, uncertain defense budgets, classified program losses, and AI integration risks may impact Lockheed Martin's revenue, profits, and cash flow.

Catalysts

About Lockheed Martin- A security and aerospace company, engages in the research, design, development, manufacture, integration, and sustainment of technology systems, products, and services worldwide.

- Lockheed Martin's record backlog of over $165 billion and a robust book-to-bill ratio signify high future revenue potential, especially from significant orders for precision and air defense munitions. This supports expectations for sustained revenue growth.

- Investments in autonomy and AI, demonstrated through successful experimental deployments, position Lockheed Martin to enhance operational efficiencies and expand combat capabilities. This innovation is likely to improve net margins due to higher efficiency and advanced technologies.

- Expanding international collaborations and local production capabilities in countries like Australia, Germany, and India indicates a strategic push towards increasing sales abroad, which could significantly boost revenue.

- Full-scale flight testing of adaptive technology and investment in digital transformation aim to enhance platform capabilities, which may result in increased earnings by enabling cost optimization and improved operational performance.

- Active management of their supply chain and production capacity, especially the collaboration on solid rocket motors, could strengthen the defense supply chain resilience further and contribute to higher net margins by reducing operational disruptions.

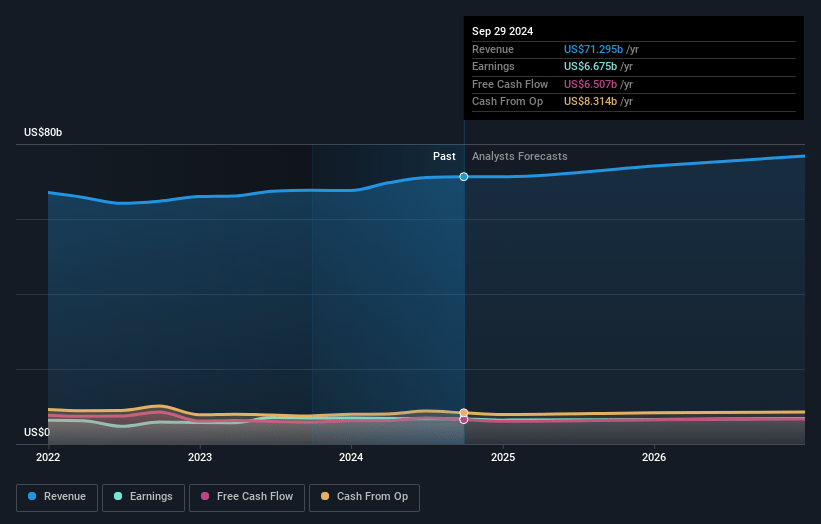

Lockheed Martin Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Lockheed Martin's revenue will grow by 3.3% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 9.4% today to 9.0% in 3 years time.

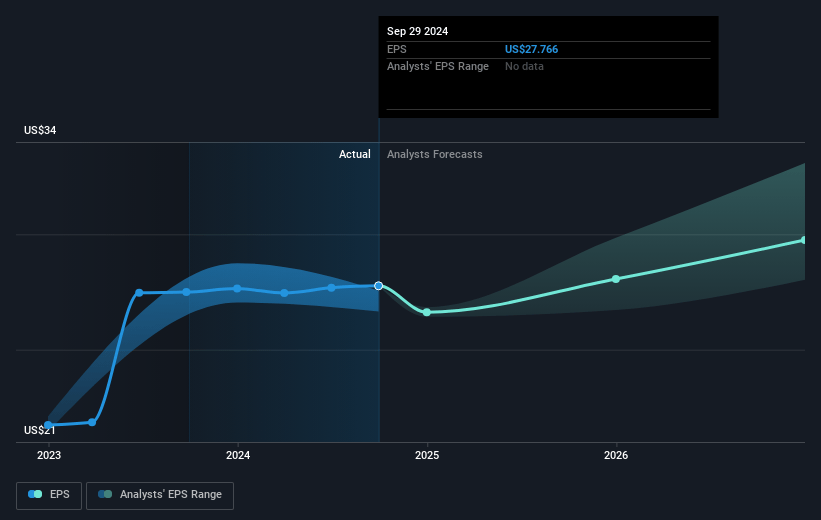

- Analysts expect earnings to reach $7.1 billion (and earnings per share of $31.29) by about January 2028, up from $6.7 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 22.4x on those 2028 earnings, up from 16.5x today. This future PE is lower than the current PE for the US Aerospace & Defense industry at 33.2x.

- Analysts expect the number of shares outstanding to decline by 1.64% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.44%, as per the Simply Wall St company report.

Lockheed Martin Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The F-35 program faces challenges such as delayed revenue recognition due to Lot 18-19 contract negotiations, which could lead to shifts in sales and cash flow into future periods, impacting short-term revenue and earnings.

- Despite increased orders and backlog, the defense budget is dependent on a continuing resolution through December 2024, creating uncertainty about long-term funding, which could affect revenue stability.

- There are concerns with the classified program losses and potential need for additional losses in the future, which may affect profit margins and net earnings.

- The integration of AI and autonomy into existing platforms and new concepts face execution risks, and if not managed well, could impact cost and timeline assumptions, influencing long-term earnings projections.

- Lockheed Martin's cash flow projections rely significantly on working capital management and supply chain improvements, with potential headwinds from pension contributions, which could affect net cash flow and dividend capabilities.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $583.17 for Lockheed Martin based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $704.0, and the most bearish reporting a price target of just $434.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $78.7 billion, earnings will come to $7.1 billion, and it would be trading on a PE ratio of 22.4x, assuming you use a discount rate of 6.4%.

- Given the current share price of $463.96, the analyst's price target of $583.17 is 20.4% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives