Narratives are currently in beta

Key Takeaways

- Strategic investments and acquisitions are set to enhance Curtiss-Wright's position in key markets, driving long-term revenue and net margin growth.

- Growing backlog and share repurchases, aligning with industry trends, indicate strong future revenue and earnings per share growth.

- Investment plans aimed at competitive improvement may pressure margins, while government budget delays and industrial market sales challenges threaten revenue and earnings growth.

Catalysts

About Curtiss-Wright- Provides engineered products, solutions, and services mainly to aerospace and defense, commercial power, process, and industrial markets worldwide.

- Curtiss-Wright anticipates closing its acquisition of Ultra Energy in the fourth quarter, which is expected to enhance its position in naval defense and power generation markets and expand its customer base globally, likely boosting revenue growth.

- The strategic investments in technology, systems, and infrastructure position Curtiss-Wright well for long-term profitable growth, with a focus on commercial nuclear and defense segments, which can improve net margins.

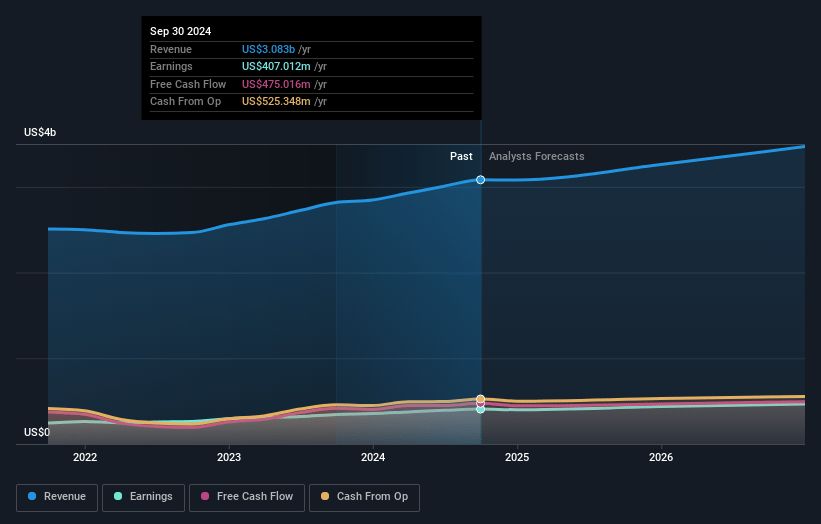

- The company's growing backlog, which has increased 16% to a new record of $3.3 billion, provides a strong basis for future revenue growth, supporting higher earnings.

- Curtiss-Wright is aligned with industry trends, such as increased power demands for data centers and rising global defense spending, which are expected to drive sales growth and enhance operating income.

- The Board's authorization for an increased share repurchase program reflects confidence in Curtiss-Wright’s strong free cash flow position and is expected to positively impact earnings per share (EPS).

Curtiss-Wright Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Curtiss-Wright's revenue will grow by 6.2% annually over the next 3 years.

- Analysts assume that profit margins will increase from 13.2% today to 14.2% in 3 years time.

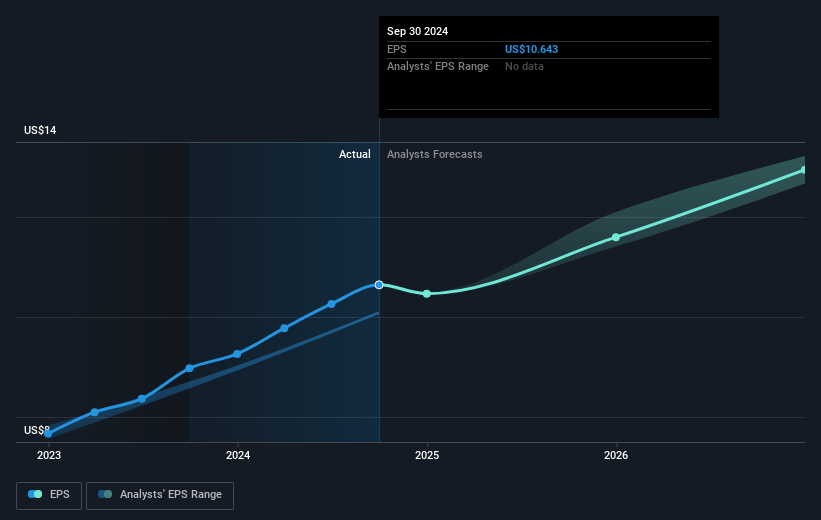

- Analysts expect earnings to reach $523.4 million (and earnings per share of $13.74) by about January 2028, up from $407.0 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 34.9x on those 2028 earnings, down from 35.7x today. This future PE is lower than the current PE for the US Aerospace & Defense industry at 35.6x.

- Analysts expect the number of shares outstanding to grow by 0.13% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.3%, as per the Simply Wall St company report.

Curtiss-Wright Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The company's results are subject to risks and uncertainties associated with forward-looking statements, which could impact future revenue growth and profitability if expectations are not met.

- Curtiss-Wright has planned significant investments across its businesses to improve competitive positioning, which could pressure operating margins if not effectively managed.

- Potential sequential declines in revenue within the Defense Electronics and Naval & Power segments may affect quarter-over-quarter earnings and operating margins due to timing of production revenues and material receipts.

- Lower expected sales in general industrial markets, driven by off-highway vehicle sales challenges, may impact overall commercial market growth and reduce total revenue projections.

- Any prolonged continuing resolutions (CRs) impacting U.S. government budget appropriations could delay new program starts in the Defense Electronics segment, hence tempering revenue and earnings growth if the current situation extends beyond typical durations.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $400.07 for Curtiss-Wright based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $452.0, and the most bearish reporting a price target of just $304.55.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $3.7 billion, earnings will come to $523.4 million, and it would be trading on a PE ratio of 34.9x, assuming you use a discount rate of 6.3%.

- Given the current share price of $382.55, the analyst's price target of $400.07 is 4.4% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives