Key Takeaways

- Strategic partnerships and collaborations in energy and hydrogen sectors are boosting revenue growth and market expansion globally, particularly in Asia and the Americas.

- Cost-cutting and restructuring efforts aim to enhance profitability and improve financial performance through reduced operating expenses.

- FuelCell Energy faces profitability challenges due to significant losses, strategic growth risks, reliance on tech commercialization, and cost reduction dependencies amidst uncertain incentives.

Catalysts

About FuelCell Energy- Manufactures and sells stationary fuel cell and electrolysis platforms that decarbonize power and produce hydrogen.

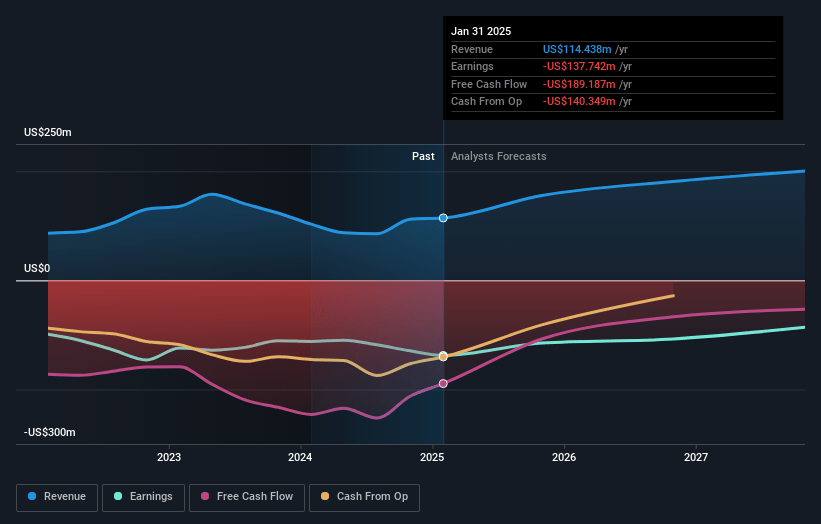

- FuelCell Energy’s cost reduction initiatives and global restructuring are expected to reduce operating expenses by 15% in fiscal year 2025, which will improve net margins and accelerate progress toward profitability.

- The partnership with Diversified Energy to deliver up to 360 megawatts to data centers in Virginia, West Virginia, and Kentucky is anticipated to drive significant revenue growth as it positions FuelCell Energy at the forefront of powering AI and high-performance computing sectors.

- The joint development agreement with Malaysia Marine and Heavy Engineering to co-develop large-scale hydrogen production systems is expected to enhance revenue by expanding FuelCell Energy's market presence in Asia, New Zealand, and Australia, tapping into growing demand for hydrogen.

- The company’s ongoing collaboration with ExxonMobil on carbon capture technology and its solid oxide electrolyzer systems could open new revenue streams and improve margins as these technologies are commercialized and integrated into existing infrastructure.

- The contracted delivery of 30 fuel cell modules to Gyeonggi Green Energy in South Korea in fiscal year 2025 is set to significantly increase product revenues, contributing to FuelCell Energy’s improved financial performance.

FuelCell Energy Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming FuelCell Energy's revenue will grow by 25.9% annually over the next 3 years.

- Analysts are not forecasting that FuelCell Energy will become profitable in next 3 years. To represent the Analyst Price Target as a Future PE Valuation we will estimate FuelCell Energy's profit margin will increase from -120.4% to the average US Electrical industry of 10.5% in 3 years.

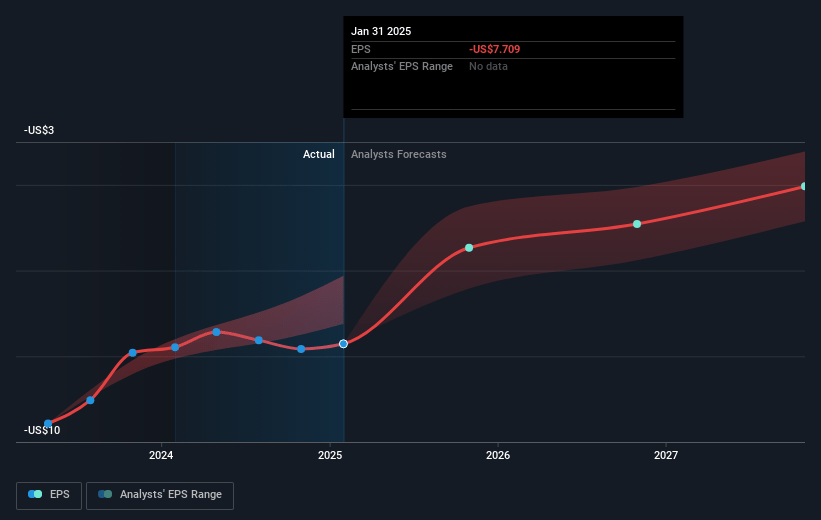

- If FuelCell Energy's profit margin were to converge on the industry average, you could expect earnings to reach $23.9 million (and earnings per share of $0.96) by about May 2028, up from $-137.7 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 12.5x on those 2028 earnings, up from -0.6x today. This future PE is lower than the current PE for the US Electrical industry at 22.8x.

- Analysts expect the number of shares outstanding to grow by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 11.41%, as per the Simply Wall St company report.

FuelCell Energy Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- FuelCell Energy has experienced historically significant losses, with a reported net loss of $29.1 million for the first quarter of fiscal 2025, which raises concerns about continued ability to achieve profitability and affects earnings.

- The reliance on new partnerships for strategic growth, such as the joint development agreement with Diversified Energy and TESIAC, could introduce operational and execution risks that might impact anticipated revenue streams and margins.

- There is a potential vulnerability due to uncertainties regarding tax credits and incentives for clean energy projects under the U.S. administration, which may affect project viability and revenue generation.

- The high dependency on successful commercialization and scaling of new technologies like solid oxide electrolyzer and carbon capture solutions poses a risk if these technologies do not achieve market acceptance or expected cost efficiencies, impacting revenues and profitability.

- The financial outlook is contingent on successfully reducing operating costs by 15% in fiscal 2025, which if not achieved could result in continued high operating losses and negative impact on the company’s margins.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $8.667 for FuelCell Energy based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $12.0, and the most bearish reporting a price target of just $4.5.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $228.4 million, earnings will come to $23.9 million, and it would be trading on a PE ratio of 12.5x, assuming you use a discount rate of 11.4%.

- Given the current share price of $4.09, the analyst price target of $8.67 is 52.8% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.