Key Takeaways

- AeroVironment's new contracts, product introductions, and acquisitions suggest long-term growth, increased revenues, and improved profit margins.

- Enhanced manufacturing capacity and favorable payment terms aim to boost operational efficiency, cash flow, and strategic reinvestment opportunities.

- AeroVironment's reliance on defense contracts and Ukraine revenue, coupled with acquisition and expense challenges, poses risks to future growth and revenue stability.

Catalysts

About AeroVironment- Designs, develops, produces, delivers, and supports a portfolio of robotic systems and related services for government agencies and businesses in the United States and internationally.

- AeroVironment has secured significant funding and contract awards, including large Switchblade IDIQ awards with a $1.7 billion ceiling, indicating long-term growth potential and visibility, likely boosting future revenues.

- The introduction of new products like the P550 UAS, with strong international and domestic interest, positions AeroVironment for revenue expansion and improved product margins as these platforms are integrated into military programs.

- The acquisition of BlueHalo will diversify AeroVironment's portfolio and enhance its competitive position in defense technology, which should contribute to increased revenues and potentially improve net margins through synergies and innovation.

- Increasing manufacturing capacity to support over $500 million in annual Switchblade product revenue indicates scaling production capabilities that could enhance operational efficiencies and increase earnings over time.

- New favorable payment terms for contracts are expected to improve cash flow and working capital, potentially positively impacting net margins by reducing financial strain and allowing for more strategic reinvestments.

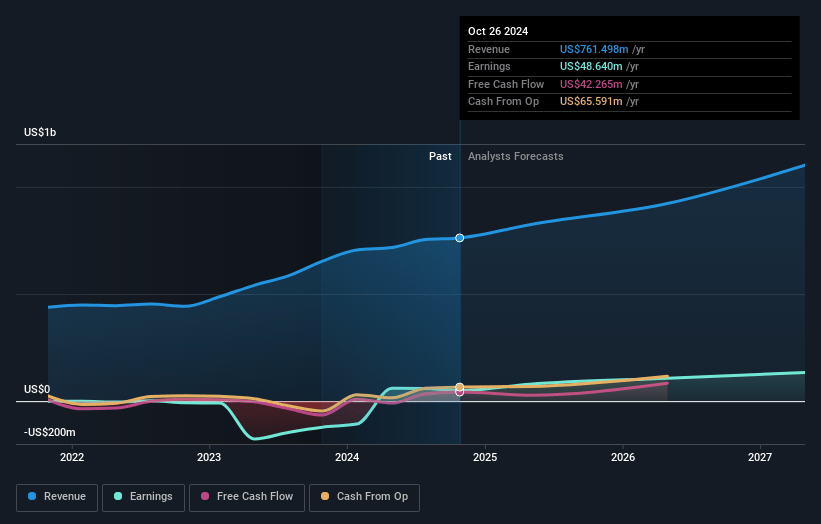

AeroVironment Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming AeroVironment's revenue will grow by 16.1% annually over the next 3 years.

- Analysts assume that profit margins will increase from 6.4% today to 15.1% in 3 years time.

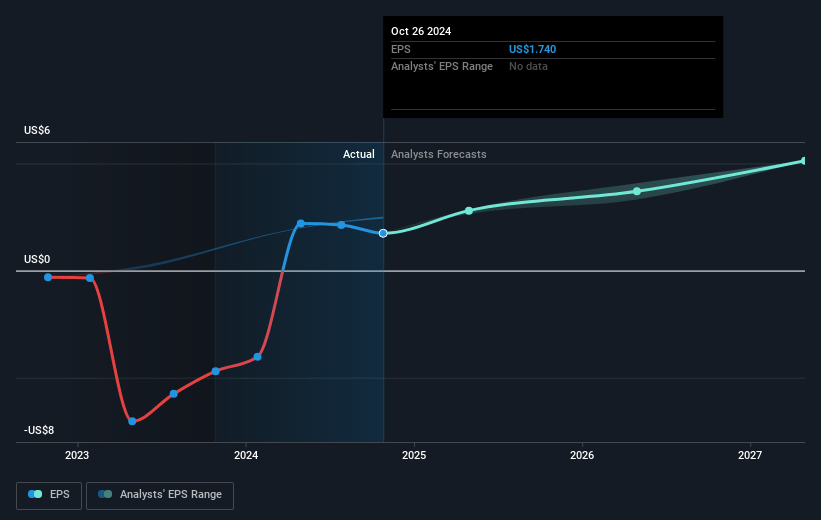

- Analysts expect earnings to reach $180.2 million (and earnings per share of $5.12) by about January 2028, up from $48.6 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 53.6x on those 2028 earnings, down from 100.8x today. This future PE is greater than the current PE for the US Aerospace & Defense industry at 34.0x.

- Analysts expect the number of shares outstanding to grow by 7.95% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.17%, as per the Simply Wall St company report.

AeroVironment Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- AeroVironment's past strong revenue from Ukraine may not be sustainable as the company transitions away from this surge, which could impact future revenue stability.

- The company's dependence on defense contracts, which are subject to political shifts such as changes in administrations and regulatory conditions, poses a risk to revenue and order timing.

- Delays or complications in completing the BlueHalo acquisition, pending regulatory and shareholder approvals, could impact the projected revenue growth and diversification plans.

- Increased SG&A and R&D expenses have already led to lower net margins, and continued high expenses could further pressure earnings if growth targets are not met.

- The market entry into specific niche areas like Group 2 UAS could face execution risks, impacting revenue growth if demand does not materialize as expected or competitive challenges arise.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $230.74 for AeroVironment based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $1.2 billion, earnings will come to $180.2 million, and it would be trading on a PE ratio of 53.6x, assuming you use a discount rate of 6.2%.

- Given the current share price of $175.04, the analyst's price target of $230.74 is 24.1% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives