Key Takeaways

- Stellar Bancorp's expansion of low-cost core funding and loan offerings is expected to enhance revenue and net interest margins.

- Strategic growth in populous markets and potential for mergers could boost revenue and improve net margins.

- Stabilization of interest rates and intense competition may pressure Stellar Bancorp's margins, potentially limiting growth and impacting net earnings.

Catalysts

About Stellar Bancorp- Operates as the bank holding company that provides a range of commercial banking services primarily to small and medium-sized businesses, professionals, and individual customers.

- Stellar Bancorp plans to expand its relationship-generated low-cost core funding base and broaden its loan offerings, which should positively impact future revenue growth and net interest margins.

- The focus on organic growth, supported by a strong capital base and potential partnerships, suggests that future earnings may see an increase, particularly with the flexibility for share repurchases or increased dividends.

- The robust capital foundation and a strong balance sheet position Stellar Bancorp to support strategic mergers and acquisitions, which could accelerate revenue growth and improve net margins with increased scale.

- Stellar Bancorp's strategic focus on operating in vibrant markets with positive job growth and population increases is expected to drive revenue growth as they capitalize on these favorable economic conditions.

- The company aims to achieve positive operating leverage in 2025 by managing expenses effectively while driving higher revenue growth, suggesting improved earnings potential.

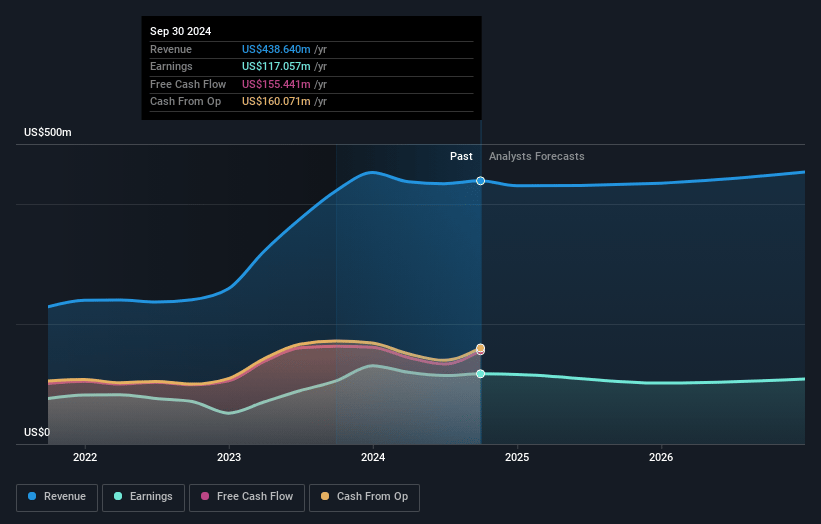

Stellar Bancorp Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Stellar Bancorp's revenue will grow by 2.3% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 26.5% today to 21.8% in 3 years time.

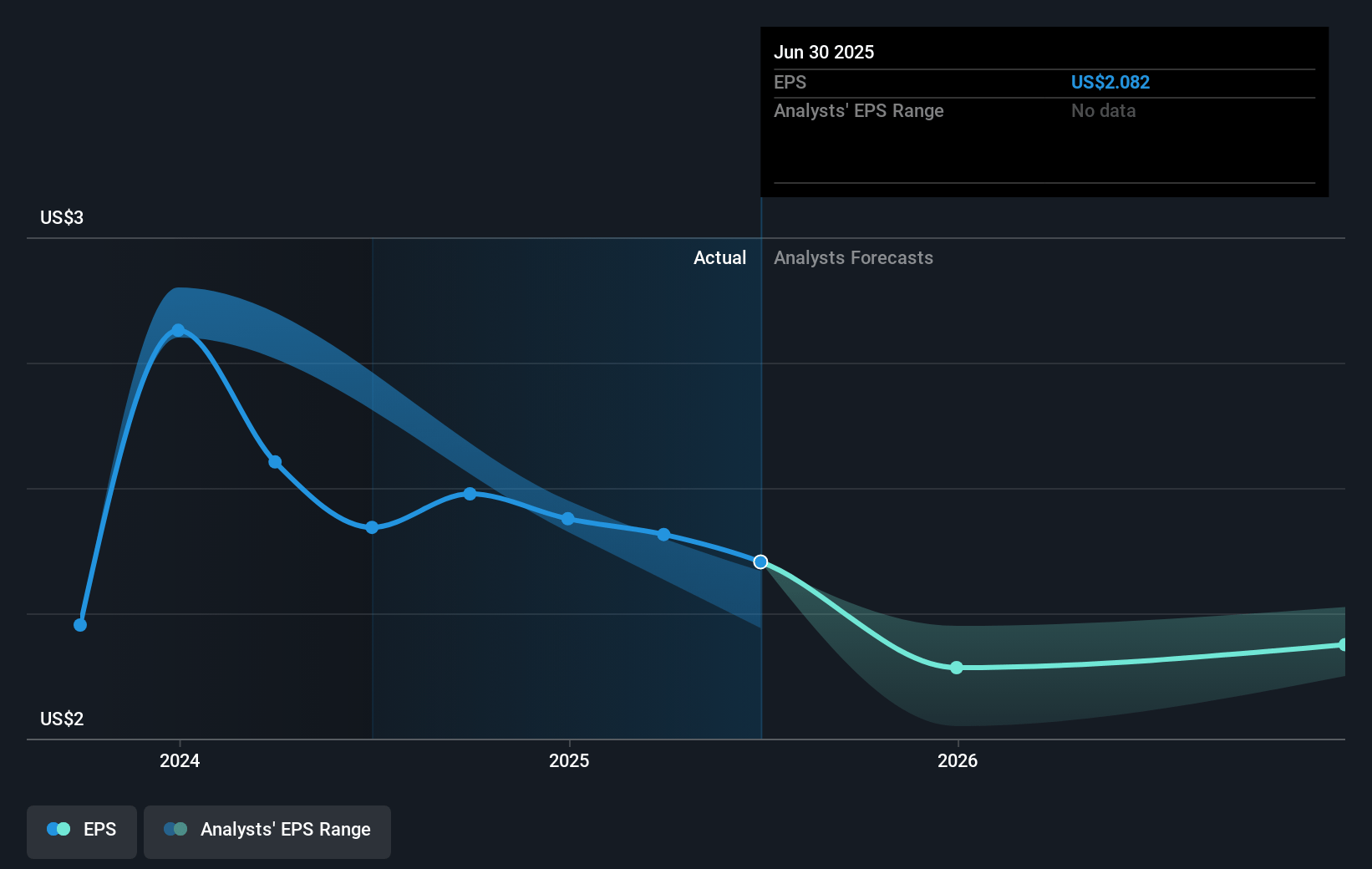

- Analysts expect earnings to reach $101.3 million (and earnings per share of $1.9) by about March 2028, down from $115.0 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 18.5x on those 2028 earnings, up from 12.6x today. This future PE is greater than the current PE for the US Banks industry at 11.2x.

- Analysts expect the number of shares outstanding to decline by 1.13% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.21%, as per the Simply Wall St company report.

Stellar Bancorp Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The stabilization rather than reduction of interest rates could limit growth opportunities and pressure margins, potentially impacting net interest margin and net income.

- There is the potential for normalization in credit which could increase provisions for credit losses, negatively affecting net earnings.

- As expenses are expected to grow modestly in line with inflation, there is a risk of operating leverage not materializing positively if revenue growth does not outpace this rise, impacting net margins.

- The presence of intense competition in the Houston market, particularly from large institutions like JPMorgan, could hinder market share gains and depress revenue growth.

- The liquidity from seasonal government deposits is transitory, which may temporarily inflate the balance sheet, not providing a lasting impact on balance sheet strength or earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $30.6 for Stellar Bancorp based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $465.1 million, earnings will come to $101.3 million, and it would be trading on a PE ratio of 18.5x, assuming you use a discount rate of 6.2%.

- Given the current share price of $27.43, the analyst price target of $30.6 is 10.4% higher. Despite analysts expecting the underlying buisness to decline, they seem to believe it's more valuable than what the market thinks.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.