Narratives are currently in beta

Key Takeaways

- The merger with First Security may not yield expected synergies or growth, potentially affecting earnings projections and resource allocation.

- Competitive deposit pricing and focus on core deposits could compress net interest margins, impacting overall earnings and revenue growth.

- Merger with First Security Bancorp presents lucrative financial prospects, including EPS accretion, excess capital returns, and expanded market share.

Catalysts

About Byline Bancorp- Operates as the bank holding company for Byline Bank that provides various banking products and services for small and medium sized businesses, commercial real estate and financial sponsors, and consumers in the United States.

- The announced merger with First Security is anticipated to add significant assets and deposits, but it might not deliver the expected synergies or growth, potentially impacting earnings growth projections.

- Byline's plan to actively pursue further M&A opportunities could strain resources if not executed effectively, impacting net margins due to integration costs and potential inefficiencies.

- Continued competitive pressure in deposit pricing, as noted by expectations of stable yet potentially lower interest income, could cause net interest margin compression, impacting overall earnings.

- By opting to reduce brokered deposits and focus on core customer deposits, future net interest income might face challenges if interest rates decline and deposit costs do not adjust quickly, affecting revenue growth.

- Anticipated mid-single-digit loan growth may not offset the potential for increased credit costs, especially if small business and commercial real estate loans experience higher stress, impacting net margins.

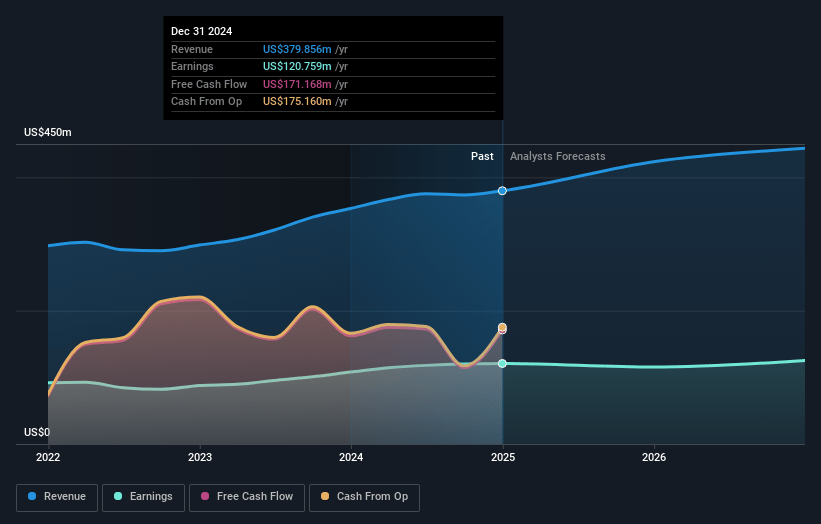

Byline Bancorp Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Byline Bancorp's revenue will grow by 7.1% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 32.1% today to 26.5% in 3 years time.

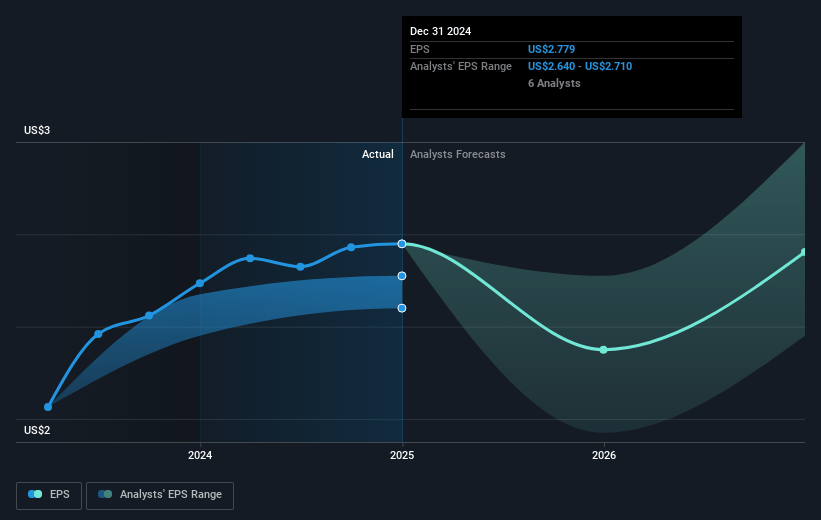

- Analysts expect earnings to reach $121.7 million (and earnings per share of $2.65) by about December 2027, up from $120.0 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 14.9x on those 2027 earnings, up from 11.7x today. This future PE is greater than the current PE for the US Banks industry at 13.1x.

- Analysts expect the number of shares outstanding to grow by 1.12% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.09%, as per the Simply Wall St company report.

Byline Bancorp Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Byline Bancorp's strong profitability metrics, including top quartile rankings among peers, could lead to continued revenue growth and stockholder rewards if the market grants the company a premium valuation.

- The merger with First Security Bancorp is expected to be financially attractive, indicating potential earnings per share (EPS) accretion, return in excess of capital, expanded market share, and other financial benefits.

- Recognized workplace awards suggest a positive company culture and investment in employee development, which could support stable operational performance and thus steady net margins.

- Continued strong loan demand, with expectations for mid-single-digit growth in the coming quarters, indicates potential revenue increases and financial growth.

- Byline Bancorp maintains strong capital levels, allowing for future organic growth and strategic investments, crucial for sustaining earnings and shareholder value over time.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $33.8 for Byline Bancorp based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2027, revenues will be $459.3 million, earnings will come to $121.7 million, and it would be trading on a PE ratio of 14.9x, assuming you use a discount rate of 6.1%.

- Given the current share price of $31.76, the analyst's price target of $33.8 is 6.0% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives