Narratives are currently in beta

Key Takeaways

- Improved balance sheet management and deposit trends are set to enhance liquidity and support future revenue and earnings growth.

- Strategic expansion into new markets and mortgage growth should drive client and revenue expansion, bolstering profitability.

- Asset quality concerns and increased expenses may pressure profitability, while changes in net interest margin and income could challenge future earnings.

Catalysts

About First Western Financial- A financial holding company, provides wealth advisory, private baking, personal trust, investment management, mortgage lending, and institutional asset management services.

- Prudent balance sheet management resulting in an improved loan-to-deposit ratio and increased liquidity positions the company for higher loan growth in 2025, likely positively impacting revenue and earnings.

- Strengthening deposit trends, particularly a 19% increase in non-interest bearing deposits, are expected to lower the company's cost of funds, which should support net interest margins going forward.

- Successful resolution of non-performing loans and sale of repossessed properties will improve asset quality and provide additional cash for redeployment into interest-earning assets, positively influencing profitability.

- Expansion of the mortgage loan officer (MLO) team, with anticipated growth in mortgage production even in a slow market, should lead to increased revenue and fee income from mortgage business activities.

- Entry into new markets and investment in talent, alongside marketing efforts, suggest potential client growth and revenue expansion, supported by operational leverage with a historical capability to handle higher revenues.

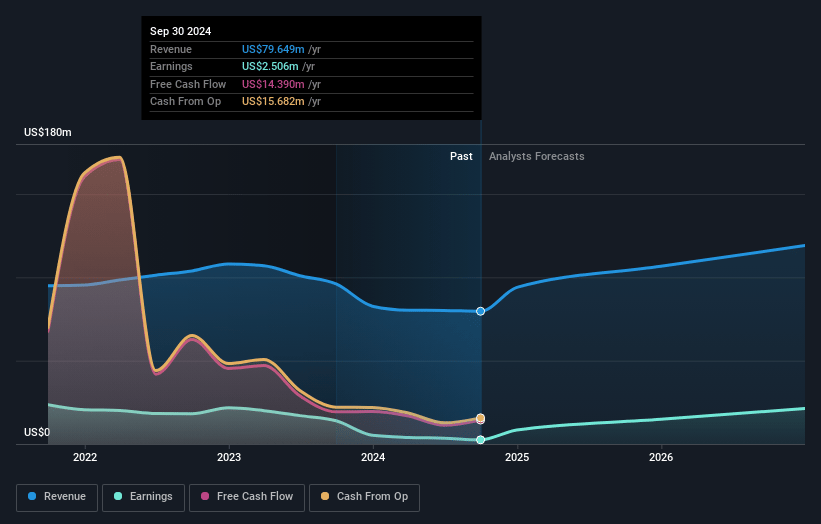

First Western Financial Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming First Western Financial's revenue will grow by 18.9% annually over the next 3 years.

- Analysts assume that profit margins will increase from 3.1% today to 24.5% in 3 years time.

- Analysts expect earnings to reach $32.8 million (and earnings per share of $3.2) by about December 2027, up from $2.5 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 8.8x on those 2027 earnings, down from 74.8x today. This future PE is lower than the current PE for the US Banks industry at 12.5x.

- Analysts expect the number of shares outstanding to grow by 1.89% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.32%, as per the Simply Wall St company report.

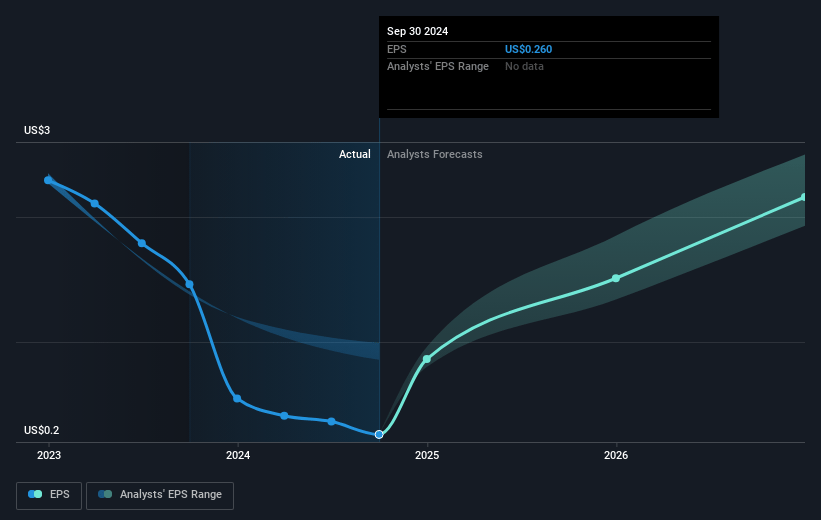

First Western Financial Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The migration of a problematic credit to non-accrual status negatively impacted net interest income and net interest margin, directly affecting future earnings and profitability.

- The reduction in net interest margin due to increased deposit costs and an unfavorable mix shift could compress earnings and squeeze net margins.

- Asset quality issues, including non-performing assets increasing to $52.1 million, could lead to higher provisions for credit losses, thereby impacting net margins and earnings.

- The low level of mortgage production in previous months, despite an increase in September, suggests potential revenue instability in periods of lower market activity.

- Elevated non-interest expenses related to recent front office hires and operational growth might not immediately offset revenue increases, impacting net margins and profitability if revenue targets are not met.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $24.0 for First Western Financial based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2027, revenues will be $133.9 million, earnings will come to $32.8 million, and it would be trading on a PE ratio of 8.8x, assuming you use a discount rate of 6.3%.

- Given the current share price of $19.39, the analyst's price target of $24.0 is 19.2% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives