Narratives are currently in beta

Key Takeaways

- Strategic investments in relationship managers and specialized lending are driving deposit growth and improving net margins through diversified revenue streams.

- Focus on market disruptions and client acquisition is enhancing franchise value and positioning the company for steady balance sheet growth.

- Reliance on consistent interest rates and Southwestern market growth could risk revenue and margin stability amid potential economic fluctuations and credit quality issues.

Catalysts

About Enterprise Financial Services- Operates as the holding company for Enterprise Bank & Trust that offers banking and wealth management services to individuals and corporate customers primarily in Arizona, California, Florida, Kansas, Missouri, Nevada, and New Mexico.

- The company has invested in hiring relationship managers with expertise in C&I banking and deposit generation, which has already started to produce significant growth in client deposits. This strategic focus is expected to enhance revenue and potentially improve net interest income.

- Enterprise Financial Services is positioned for mid

- to high-single-digit balance sheet growth in 2025, supported by strong loan and deposit pipelines. This growth expectation indicates potential for increased revenue and net interest income.

- The company anticipates a slight elevation in loan demand due to changes in client sentiment post-election, which could drive revenue growth as loan portfolio diversification is pursued.

- Strategic growth in specialized lending areas such as life insurance premium finance and SBA lending, with solid risk-adjusted returns, suggests potential for improved net margins and enhanced earnings through diversified revenue streams.

- The focus on leveraging disruptions in the market to recruit talent and acquire new client relationships is likely to expand franchise value and profitability, supporting earnings growth.

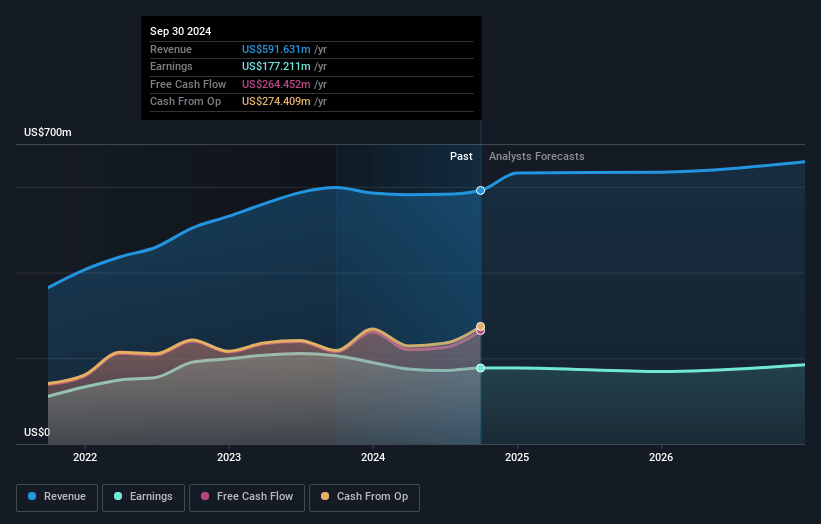

Enterprise Financial Services Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Enterprise Financial Services's revenue will grow by 4.2% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 29.9% today to 26.4% in 3 years time.

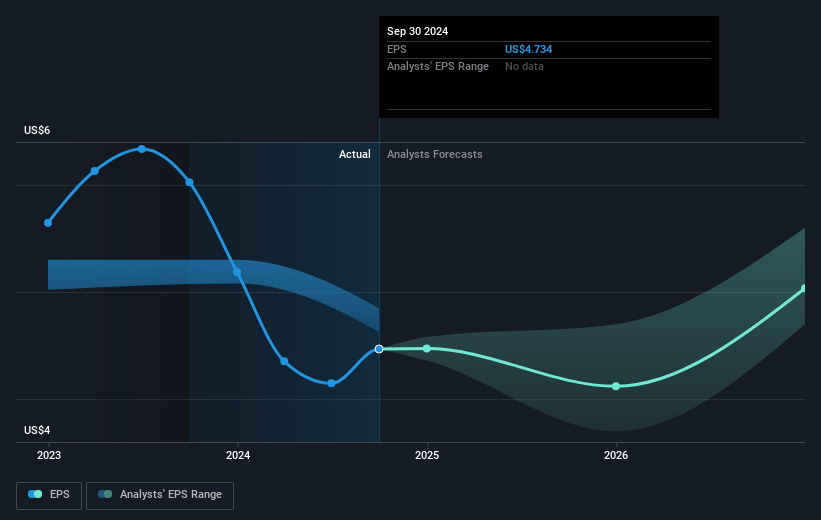

- Analysts expect earnings to reach $181.3 million (and earnings per share of $5.0) by about January 2028, down from $181.5 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 15.7x on those 2028 earnings, up from 12.3x today. This future PE is greater than the current PE for the US Banks industry at 12.3x.

- Analysts expect the number of shares outstanding to decline by 0.75% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 5.92%, as per the Simply Wall St company report.

Enterprise Financial Services Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The muted growth within the generalized C&I categories, due to businesses using lines of credit sparingly and opting to use cash reserves, could pose a risk to loan growth projections, impacting revenue and future earnings.

- Increase in nonperforming assets, although described as modest, and a slight rise in net charge-offs could signal potential credit quality issues, which may affect net margins.

- The reliance on a positive interest rate environment to maintain net interest margin could present a risk, particularly if rate cuts occur, potentially impacting net interest income and earnings.

- The potential remixing of deposit balances and the pressure on deposit costs management may lead to challenges in maintaining a favorable margin, impacting net interest revenue.

- The geographic market concentrations, such as strong reliance on Southwestern markets for growth, might expose the company to regional economic variances affecting revenue predictions.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $66.5 for Enterprise Financial Services based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $687.3 million, earnings will come to $181.3 million, and it would be trading on a PE ratio of 15.7x, assuming you use a discount rate of 5.9%.

- Given the current share price of $60.04, the analyst's price target of $66.5 is 9.7% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives