Narratives are currently in beta

Key Takeaways

- New model introductions and strategic spending aim to boost revenues and long-term growth prospects for Winnebago Industries.

- Operational improvements and strong Marine segment dynamics are expected to enhance margins and market share.

- Competitive pressures and economic uncertainties, along with increased expenses and lower revenues, could compress margins and negatively impact future earnings and revenue growth.

Catalysts

About Winnebago Industries- Manufactures and sells recreation vehicles and marine products primarily for use in leisure travel and outdoor recreation activities.

- Winnebago Industries is expecting an improved demand landscape in the second half of fiscal 2025 due to increasing consumer confidence and a stabilized retail environment, which should positively impact revenue growth.

- The introduction of new models such as the Grand Design Lineage Series F Super C and other upcoming products are expected to enhance the product lineup, potentially boosting future revenues.

- Strategic leadership changes and operational efficiency initiatives are underway to address inefficiencies in the Winnebago-branded Motorhome and Towables segments, which are anticipated to improve margins in the back half of calendar 2025.

- Strong market dynamics in the Marine segment, driven by Barletta and Chris-Craft brands, show potential for market share gains, contributing to revenue and margin growth.

- Planned capital spending and strategic investments in brand development are focused on driving long-term growth, which could enhance future earnings.

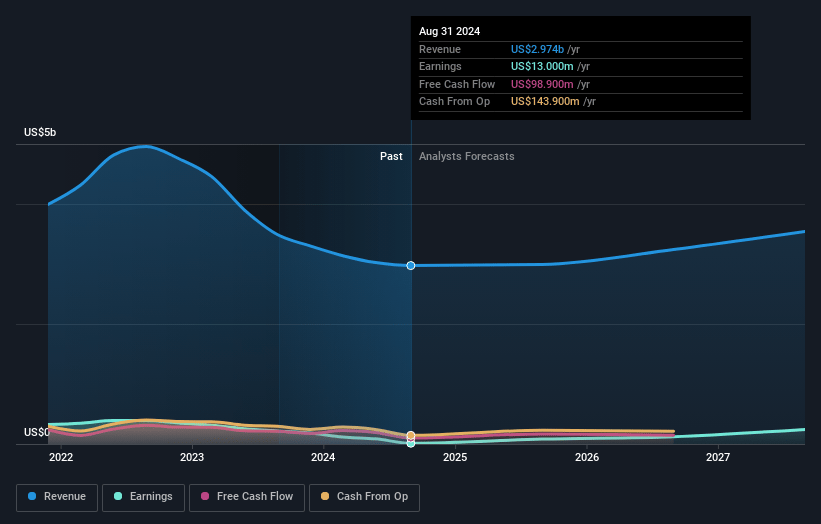

Winnebago Industries Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Winnebago Industries's revenue will grow by 8.6% annually over the next 3 years.

- Analysts assume that profit margins will increase from -0.6% today to 6.8% in 3 years time.

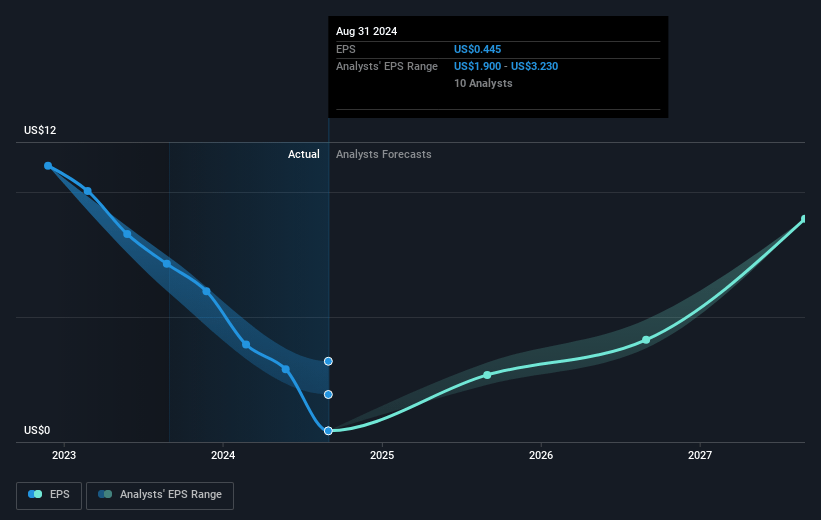

- Analysts expect earnings to reach $248.5 million (and earnings per share of $9.29) by about December 2027, up from $-18.0 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 9.3x on those 2027 earnings, up from -75.6x today. This future PE is lower than the current PE for the US Auto industry at 17.5x.

- Analysts expect the number of shares outstanding to decline by 1.97% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 10.86%, as per the Simply Wall St company report.

Winnebago Industries Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The challenging operating environment in the outdoor recreation space, marked by soft retail demand and a cautious dealer network, resulted in lower segment revenues and profitability in the Towable and Motorhome RV segments. This could negatively impact future revenue and net margins.

- Segment revenues were down 18% compared to the previous year, driven by lower unit volumes and a shift in product mix, coupled with higher warranty expenses, which reduced gross margins. This trend could continue to pressure earnings.

- The company experienced higher operating expenses related to Grand Design Motorhome, Barletta, and Lithionics businesses alongside investments in digital capabilities. This increase in expenses could further compress net margins.

- Winnebago's market share has declined by 50 basis points, potentially indicating competitive pressures and future revenue risks if the market continues to underperform.

- The macroeconomic factors, including high consumer interest rates and dealer network financial health, present uncertainties. If conditions remain unchanged, they could limit consumer financing capabilities and affect revenue and earnings negatively.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $64.9 for Winnebago Industries based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $80.0, and the most bearish reporting a price target of just $54.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2027, revenues will be $3.6 billion, earnings will come to $248.5 million, and it would be trading on a PE ratio of 9.3x, assuming you use a discount rate of 10.9%.

- Given the current share price of $47.89, the analyst's price target of $64.9 is 26.2% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives